|

市场调查报告书

商品编码

1928920

水洗水槽市场机会、成长要素、产业趋势分析及2026年至2035年预测Water Sink Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球水族馆市场预计到 2025 年将价值 104 亿美元,到 2035 年将达到 184 亿美元,年复合成长率为 6%。

全球各地酒店食品服务基础设施的快速发展推动了市场扩张。新型住宿设施和餐饮设施的不断涌现,带动了对能够承受日常高强度使用并保持高效运作的水槽的需求。高客流量的商业环境越来越重视耐用材料和能够满足频繁清洁需求的设计。旅行活动的增加以及消费者饮食习惯的改变,促使新的服务场所不断涌现,进一步支撑了市场需求。同时,人们对智慧免接触式水槽解决方案的兴趣日益浓厚,正在改变住宅和商业环境中的购买偏好。这些系统在高使用率环境中极具吸引力,因为自动化操作有助于提高卫生标准并节约用水。日益增长的永续性意识和不断上涨的水价也在影响购买决策,促使人们更加关注节水设计。製造商正在积极回应,推出兼顾节水、耐用和现代外观的产品,而环境认证也正成为计划核准的关键因素。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 104亿美元 |

| 预测金额 | 184亿美元 |

| 复合年增长率 | 6% |

预计2025年,固定式水族箱市场规模将达85亿美元,2026年至2035年期间的复合年增长率将达到6%。该细分市场凭藉其结构强度高、性能可靠和应用广泛等优势,持续引领市场。固定式水族箱安装稳固,使用寿命长,因此非常适合需要持续可靠性和抗损性的严苛环境。

预计到2025年,嵌入式水槽将占据56%的市场份额,并在2035年之前以6.1%的复合年增长率成长。其强劲的市场地位归功于安装简单、兼容多种檯面类型以及易于维护。这种形式便于快速更换并减少人力成本,因此对住宅和商业用户都极具吸引力。

预计2025年,中国水族箱市场规模将达到11亿美元,2026年至2035年期间的复合年增长率(CAGR)将达到6.5%。中国市场成长的主要驱动力是持续的城市发展以及住宅和商业领域建设活动的增加。消费者对符合现代设计偏好、卫生标准和材料耐用性的水族箱的需求持续成长。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 产业影响因素

- 司机

- 住宅和住宅维修活动增加

- 消费者越来越偏好高端、现代的厨房美学

- 扩展全球酒店和食品服务基础设施

- 挑战与困难

- 大众住宅市场对价格高度敏感

- 低成本材料频繁磨损和表面损伤

- 机会

- 推出一款采用回收材料製成的环保水槽

- 增加模组化户外厨房和实用水槽的安装量

- 司机

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 监管环境

- 标准和合规要求

- 区域法规结构

- 认证标准

- 贸易统计(HS编码-6910)

- 主要进口国

- 主要出口国

- 波特分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 按类型分類的市场估算与预测,2022-2035年

- 固定水箱

- 可携式洗涤池

6. 按安装类型分類的市场估算与预测,2022-2035 年

- 无需预约

- 下装式

- 工作站水槽

- 其他(吧台水槽等)

第七章 按材料分類的市场估算与预测,2022-2035年

- 不銹钢

- 花岗岩/石英

- 陶瓷水槽

- 耐火黏土水槽

- 其他(铜水槽等)

第八章 依产品类型分類的市场估算与预测,2022-2035年

- 单槽水槽

- 双槽水槽

第九章 按应用领域分類的市场估算与预测,2022-2035年

- 住宅

- 商业的

第十章 按分销管道分類的市场估算与预测,2022-2035年

- 直销

- 间接销售

第十一章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

第十二章:公司简介

- Alveus

- American Standard

- Blanco

- Duravit

- Elkay

- Franke

- JOMOO

- Kohler

- Moen

- Pyramis

- Reginox

- Roca

- Schock

- Teka Group

- TOTO

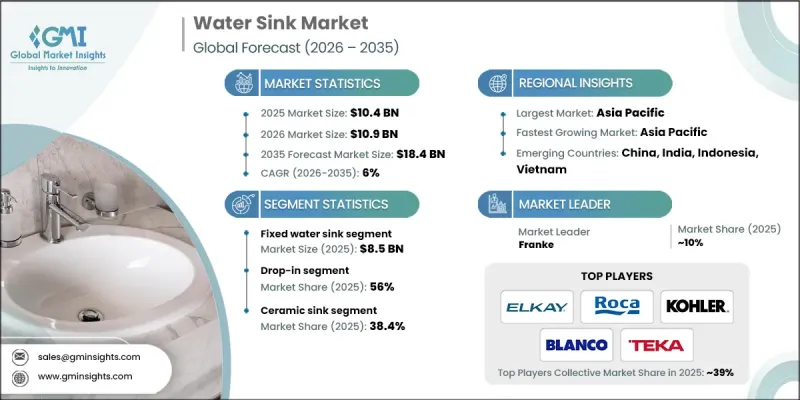

The Global Water Sink Market was valued at USD 10.4 billion in 2025 and is estimated to grow at a CAGR of 6% to reach USD 18.4 billion by 2035.

Market expansion is supported by the rapid development of hospitality and food service infrastructure across global regions. As new accommodation and food preparation facilities continue to emerge, demand is rising for sinks that can support intensive daily usage while maintaining operational efficiency. High-capacity commercial environments are increasingly prioritizing durable materials and designs that support frequent sanitation requirements. Growth in travel activity and changing consumer dining habits are contributing to the steady establishment of new service outlets, which further sustains demand. At the same time, growing interest in smart and hands-free sink solutions is reshaping purchasing preferences across residential and commercial settings. Automated operation improves hygiene standards and supports water conservation efforts, making these systems attractive in high-usage environments. Increasing focus on sustainability and rising water costs are also influencing buying decisions, with water-saving designs gaining traction. Manufacturers are responding by introducing products that balance reduced consumption, long-term durability, and modern visual appeal, while environmental certifications are becoming an important factor in project approvals.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.4 Billion |

| Forecast Value | $18.4 Billion |

| CAGR | 6% |

The fixed water sink segment generated USD 8.5 billion in 2025 and is expected to grow at a CAGR of 6% from 2026 to 2035. This segment continues to lead the market due to its structural strength, dependable performance, and broad applicability. Fixed sinks offer secure installation and long service life, making them suitable for demanding environments that require consistent reliability and resistance to damage.

The drop-in sinks segment accounted for 56% share in 2025 and is projected to grow at a CAGR of 6.1% during 2035. Their strong position is attributed to simplified installation, compatibility with multiple surface types, and ease of maintenance. This format allows faster replacement and reduced labor requirements, which appeals to both residential and commercial buyers.

China Water Sink Market reached USD 1.1 billion in 2025 and is forecast to grow at a CAGR of 6.5% from 2026 to 2035. Market growth in the country is being driven by ongoing urban development and rising construction activity across residential and commercial sectors. Demand continues to increase for sinks that align with modern design preferences, hygiene standards, and material durability expectations.

Key companies operating in the Global Water Sink Market include Kohler, Franke, TOTO, Blanco, Elkay, Roca, Moen, Duravit, Teka Group, American Standard, JOMOO, Reginox, Pyramis, Schock, and Alveus. Companies active in the Global Water Sink Market are reinforcing their competitive positions through product innovation, brand expansion, and strategic partnerships. Many manufacturers are focusing on developing water-efficient and smart-enabled sink solutions to align with sustainability goals and evolving consumer expectations. Investments in material technology and surface finishes are helping improve durability and design differentiation. Firms are also expanding distribution networks and strengthening relationships with commercial developers and contractors. Customization options, certifications, and region-specific product offerings are being used to enhance market penetration and build long-term customer loyalty across residential and commercial segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Installation

- 2.2.4 Material

- 2.2.5 Configuration

- 2.2.6 Application

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in residential construction and home renovation activities

- 3.2.1.2 Increasing consumer preference for premium and modern kitchen aesthetics

- 3.2.1.3 Expansion of hospitality and foodservice infrastructure globally

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High price sensitivity in mass-market residential segments

- 3.2.2.2 Frequent wear and surface damage in low-cost materials

- 3.2.3 Opportunities

- 3.2.3.1 Adoption of eco-friendly and recycled material sink options

- 3.2.3.2 Growth of modular outdoor kitchen and utility sink installations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS Code - 6910)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter';s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Fixed water sink

- 5.3 Portable water sink

Chapter 6 Market Estimates & Forecast, By Installation Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Drop-in

- 6.3 Under mount

- 6.4 Workstation sinks

- 6.5 Others (bar sinks etc.)

Chapter 7 Market Estimates & Forecast, By Material, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Stainless Steel

- 7.3 Granite/quartz

- 7.4 Ceramic sink

- 7.5 Fireclay sink

- 7.6 Others (copper sinks etc.)

Chapter 8 Market Estimates & Forecast, By Configuration, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Single bowl sink

- 8.3 Double bowl sink

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Alveus

- 12.2 American Standard

- 12.3 Blanco

- 12.4 Duravit

- 12.5 Elkay

- 12.6 Franke

- 12.7 JOMOO

- 12.8 Kohler

- 12.9 Moen

- 12.10 Pyramis

- 12.11 Reginox

- 12.12 Roca

- 12.13 Schock

- 12.14 Teka Group

- 12.15 TOTO

按槽数、安装方式、材质、分销管道和应用分類的全球分槽式水槽市场预测(2026-2032年)

按槽数、安装方式、材质、分销管道和应用分類的全球分槽式水槽市场预测(2026-2032年) 全球石英水槽市场规模、份额、趋势和成长分析报告(2026-2034年)

全球石英水槽市场规模、份额、趋势和成长分析报告(2026-2034年) 水处理设备市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、分销管道、地区和竞争格局划分,2021-2031年)石英水槽市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、分销管道、地区和竞争格局划分,2021-2031年)厨房水槽市场 - 全球产业规模、份额、趋势、机会和预测,按材质(金属、花岗岩、其他)、水槽数量(单槽、多槽)、最终用户(住宅、商业)、地区和竞争格局划分,2021-2031年预测

水处理设备市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、分销管道、地区和竞争格局划分,2021-2031年)石英水槽市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、分销管道、地区和竞争格局划分,2021-2031年)厨房水槽市场 - 全球产业规模、份额、趋势、机会和预测,按材质(金属、花岗岩、其他)、水槽数量(单槽、多槽)、最终用户(住宅、商业)、地区和竞争格局划分,2021-2031年预测 石英水槽市场规模、份额及成长分析(按类型、应用、通路和地区划分)-2026-2033年产业预测

石英水槽市场规模、份额及成长分析(按类型、应用、通路和地区划分)-2026-2033年产业预测 家用厨房水槽市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)厨房水槽市场依材质、安装方式、水槽形状、应用和通路划分-2025-2032年全球预测

家用厨房水槽市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)厨房水槽市场依材质、安装方式、水槽形状、应用和通路划分-2025-2032年全球预测 全球厨房水槽市场全球多功能厨房水槽市场

全球厨房水槽市场全球多功能厨房水槽市场