|

市场调查报告书

商品编码

1928925

铝颜料市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Aluminum Pigments Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

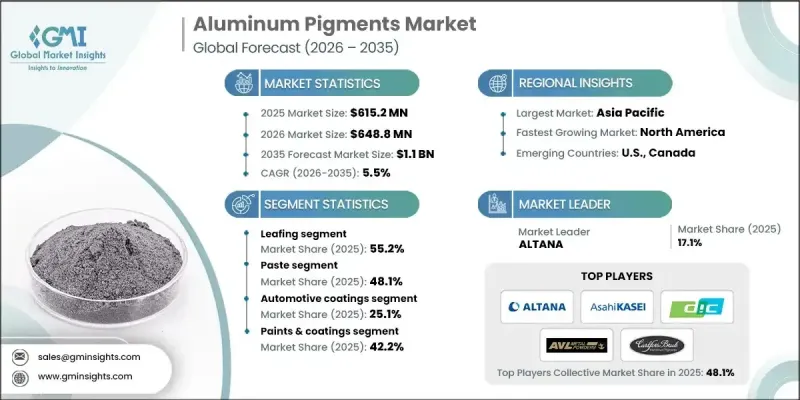

全球铝颜料市场预计到 2025 年将达到 6.152 亿美元,到 2035 年将达到 11 亿美元,年复合成长率为 5.5%。

由于汽车、包装、化妆品、涂料等行业的需求不断增长,铝颜料市场正在扩张。铝颜料因其金属光泽和反射特性而备受青睐,不仅能提升视觉吸引力,还能改善最终产品的功能性能。它们能实现镜面效果,增强耐久性、耐腐蚀性和热稳定性。这些颜料具有高遮盖力、高亮度和金属光泽,是装饰性和功能性涂料的理想选择。其反射性能也有助于降低热吸收,进而提高能源效率。其化学稳定性和耐环境性进一步延长了成品的使用寿命。汽车涂料和高端个人保健产品中铝颜料的日益普及,以及各行业对高品质涂料的需求,持续推动铝颜料的市场成长。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 6.152亿美元 |

| 预测金额 | 11亿美元 |

| 复合年增长率 | 5.5% |

预计到2025年,片状铝颜料将占据55.2%的市场份额,并在2035年之前以5.6%的复合年增长率增长。该细分市场之所以迅速发展,是因为其能够形成超薄反射层,并产生高金属光泽的表面。这些特性使得片状颜料成为汽车和装饰应用领域高端涂料的首选。

依产品形态划分,预计2025年,膏状铝颜料市占率将达到48.1%,并在2026年至2035年间以5.6%的复合年增长率成长。膏状颜料因其优异的分散性、均匀性和易混性,被广泛应用于工业涂料、汽车涂料和装饰涂料领域。这些特性确保了涂料表面光滑且具有高反射性,从而帮助製造商提升产品的视觉效果和耐久性。

预计北美铝颜料市场将持续保持强劲成长势头,到2025年将占据26.1%的市场份额。该地区的需求主要由汽车、涂料和包装行业的应用所驱动。随着永续性和环保措施对生产产生影响,製造商正致力于研发低VOC和水性配方。汽车产业仍然是关键领域,消费者和製造商都在寻求高光泽、反光效果的涂料,以提升产品美观。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 按类型分類的市场估算与预测,2022-2035年

- 叶子

- 不落叶

第六章 按类型分類的市场估算与预测,2022-2035年

- 贴上

- 粉末

- 颗粒

- 其他(片状物等)

第七章 按应用领域分類的市场估算与预测,2022-2035年

- 汽车涂料

- 工业涂料

- 建筑和装饰涂料

- 凹版印刷油墨

- 柔版印刷油墨

- 工业塑料

- 美甲产品

- 脸部美妆

- 护髮产品

- 其他的

第八章 依最终用途产业分類的市场估算与预测,2022-2035年

- 油漆和涂料

- 印刷油墨

- 塑胶

- 个人护理及化妆品

- 其他(建筑、电子等)

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十章:公司简介

- ALTANA

- Asahi Kasei

- AVL METAL POWDERS nv

- Carlfors Bruk

- DIC CORPORATION

- Kolortek Co., Ltd.

- Metaflake Ltd

- SCHLENK SE

- Shan Dong Jie Han Metal Material Co., Ltd

- TOYO ALUMINIUM KK

- Zhangqiu metallic pigment co.,ltd.

- ZuXing New Materials Co., Ltd.

The Global Aluminum Pigments Market was valued at USD 615.2 million in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 1.1 billion by 2035.

The market is expanding due to rising demand across sectors such as automotive, packaging, cosmetics, and paints & coatings. Aluminum pigments are prized for their metallic sheen and reflective properties, which not only enhance visual appeal but also improve functional performance in end-use products. They deliver a mirror-like finish, increase durability, boost corrosion resistance, and enhance thermal stability. These pigments offer high opacity, brightness, and metallic effects, making them ideal for decorative and functional coatings. Their reflective capabilities also contribute to energy efficiency by reducing heat absorption. Chemical stability and environmental resilience further add to the longevity of finished products. Increasing use in automotive coatings and luxury personal care items continues to drive adoption, supported by demand for high-quality finishes in various industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $615.2 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 5.5% |

The leafing aluminum pigments segment held 55.2% share in 2025 and is projected to grow at a CAGR of 5.6% through 2035. This segment is gaining traction due to its ability to form ultra-thin reflective layers, producing highly metallic and glossy surfaces. Such properties make leafing pigments a preferred choice for premium coatings in automotive and decorative applications.

In terms of product form, the paste aluminum pigments segment held 48.1% share in 2025 and is expected to grow at a CAGR of 5.6% between 2026 and 2035. Paste pigments are widely used in industrial coatings, automotive finishes, and decorative paints because they provide excellent dispersibility, uniform distribution, and easy blending. These features ensure smooth, reflective surfaces and enable manufacturers to enhance both the visual appeal and durability of their products.

North America Aluminum Pigments Market accounted for 26.1% share in 2025 and continues to exhibit strong growth. The region's demand is driven by applications in automotive, coatings, and packaging sectors. Sustainability and eco-friendly practices are increasingly influencing production, leading manufacturers to focus on low-VOC and water-based formulations. Automotive remains a key sector, with consumers and manufacturers seeking high-gloss and reflective finishes to elevate product aesthetics.

Key players in the Global Aluminum Pigments Market include Metaflake Ltd, DIC CORPORATION, ALTANA, Asahi Kasei, SCHLENK SE, Carlfors Bruk, TOYO ALUMINIUM K.K., Zhangqiu Metallic Pigment Co., Ltd., ZuXing New Materials Co., Ltd., Kolortek Co., Ltd., and AVL METAL POWDERS n.v. Market participants are adopting several strategies to strengthen their presence and expand market share. Companies are investing in advanced manufacturing technologies and eco-friendly processes to meet sustainability requirements. They are increasing production capacities, enhancing R&D for high-performance pigments, and diversifying product portfolios. Strategic collaborations, partnerships, and regional expansions allow firms to access new markets and serve emerging applications. Focus on product innovation, quality improvement, and operational efficiency further solidifies the market position and ensures long-term competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Form

- 2.2.4 Application

- 2.2.5 End use industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Leafing

- 5.3 Non-leafing

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Paste

- 6.3 Powder

- 6.4 Pellets

- 6.5 Others (flakes, etc)

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive coatings

- 7.3 Industrial coatings

- 7.4 Architectural/decorative coatings

- 7.5 Gravure inks

- 7.6 Flexographic inks

- 7.7 Industrial plastic

- 7.8 Nail products

- 7.9 Face makeup

- 7.10 Hair care products

- 7.11 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Paints & coatings

- 8.3 Printing inks

- 8.4 Plastics

- 8.5 Personal care & cosmetics

- 8.6 Others (construction, electronics, etc)

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 ALTANA

- 10.2 Asahi Kasei

- 10.3 AVL METAL POWDERS n.v.

- 10.4 Carlfors Bruk

- 10.5 DIC CORPORATION

- 10.6 Kolortek Co., Ltd.

- 10.7 Metaflake Ltd

- 10.8 SCHLENK SE

- 10.9 Shan Dong Jie Han Metal Material Co., Ltd

- 10.10 TOYO ALUMINIUM K.K.

- 10.11 Zhangqiu metallic pigment co.,ltd.

- 10.12 ZuXing New Materials Co., Ltd.