|

市场调查报告书

商品编码

1928926

合成及生物乳化聚合物市场:机会、成长要素、产业趋势分析及2026年至2035年预测Synthetic and Bio Emulsion Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

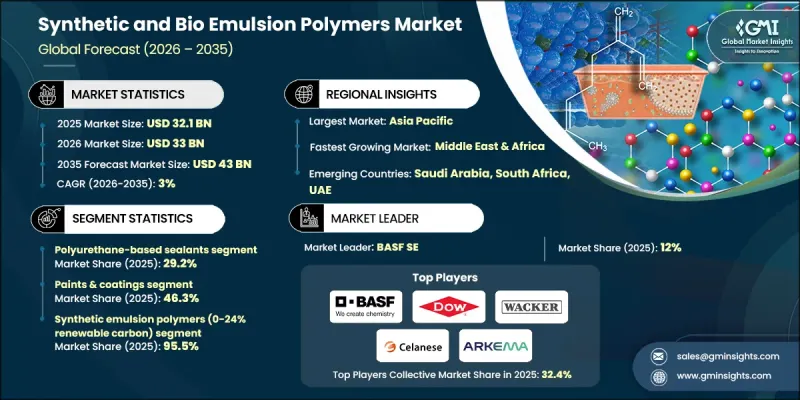

全球合成和生物乳化聚合物市场预计到 2025 年将达到 321 亿美元,预计到 2035 年将达到 430 亿美元,复合年增长率为 3%。

多年来,合成和生物基乳化聚合物已从利基产品发展成为支撑现代海事作业和工业应用的关键材料。它们的作用不仅限于基本的密封,还能提升船舶的结构完整性、耐腐蚀性和长期性能。随着永续性趋势重塑产业优先事项,这些聚合物正处于高性能、环保解决方案的前沿,有助于减少船舶建造、维护和维修对环境的影响。为因应严格的环境法规和全球脱碳目标,混合配方、低VOC系统和可再生原料聚合物在工业领域日益受到关注。市场成长主要受区域生产优先事项的驱动,其中亚太地区凭藉强劲的造船活动和不断扩大的商船队主导成长。这催生了对可靠的高性能乳化聚合物解决方案的巨大需求。技术进步不断提升耐久性、耐化学性和适应性,可望推动市场长期稳定成长。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 321亿美元 |

| 预测金额 | 430亿美元 |

| 复合年增长率 | 3% |

预计到2025年,涂料和油漆领域将占据46.3%的市场份额,并在2035年之前以3.2%的复合年增长率成长。在该领域,聚合物发挥着至关重要的作用,它们赋予涂料良好的成膜性、耐久性和抗环境应力能力,从而提供保护性和装饰性涂层。尤其是丙烯酸和聚氨酯分散体的强黏合性能,在工业和结构性黏着剂备受重视。

预计到 2025 年,可再生碳含量为 0-24% 的合成乳化聚合物将占据市场主导地位,市占率达到 95.5%,到 2035 年将以 2.4% 的复合年增长率成长。这些配方因其机械强度高、耐化学腐蚀且在恶劣环境下具有长期稳定性,而被广泛应用于涂料、黏合剂和建筑业,使其在许多工业领域比生物基替代品更值得信赖。

预计到2025年,北美合成和生物乳化聚合物市占率将达到21.9%。该地区先进的製造能力、有利的法规环境以及对永续实践日益增长的接受度,使其成为合成和生物乳化聚合物的领先中心。该地区的各行业需要高性能配方,以满足严格的环境和创新主导标准,从而支持涂料、黏合剂和建筑等领域的应用。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 对环保和永续产品的需求日益增长

- 在油漆、涂料和黏合剂行业中不断扩展的应用

- 聚合技术的进步

- 产业潜在风险与挑战

- 原物料价格波动

- 严格的环境法规

- 市场机会

- 新兴市场的扩张

- 生物基乳化聚合物的开发

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按聚合物类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 依聚合物类型分類的市场估算与预测,2022-2035年

- 丙烯酸纤维

- 醋酸乙烯酯聚合物

- 苯乙烯-丁二烯乳胶(SBR)

- 苯乙烯-丙烯酸共聚物

- 乙烯基丙烯酸共聚物

- 聚氨酯分散体(PUD)

- 生物基乳化聚合物

- 生物性丙烯酸酯(可再生单体)

- 生物基苯乙烯丁二烯

- 天然乳胶(源自橡胶树)

- 其他的

第六章 按应用领域分類的市场估算与预测,2022-2035年

- 油漆和涂料

- 建筑涂料(室内/室外)

- 工业涂料

- 保护涂层

- 黏合剂

- 压敏黏着剂(PSA)

- 层压黏合剂

- 组装黏合剂

- 其他的

- 纸和纸板涂层

- 纸张涂层(光面、雾面、丝光)

- 纸板涂装(折迭纸盒、瓦楞纸板)

- 其他的

- 建筑和水泥改性

- 水泥添加剂和改质剂

- 防水膜

- 磁砖黏合剂和填缝剂

- 外墙保温装饰系统(EIFS)

- 其他的

- 纤维和不织布

- 纺织加工和涂层

- 地毯背衬

- 其他的

- 沥青改性

- 道路建设/维护用途

- 屋顶产品

- 其他的

- 密封剂

- 其他(印刷油墨、地板清洁剂、皮革整理加工剂)

7. 依可再生碳含量分類的市场估算与预测,2022-2035年

- 合成乳化聚合物(可再生碳含量0-24%)

- 生物基乳化聚合物(超过25%的可再生碳)

- 生物含量低(25-49%可再生碳)

- 中等生物含量(50-74%可再生碳)

- 高生物含量(75%或以上可再生碳)

第八章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- BASF SE

- The Dow Chemical Company

- Wacker Chemie AG

- Celanese Corporation

- Arkema SA

- Trinseo PLC

- Covestro AG

- Synthomer PLC

- Dairen Chemical Corporation

- Asahi Kasei Corporation

- Mallard Creek Polymers

- Encres Dubuit

- Organik Kimya

- Shenzhen Jitian Chemical

- Indulor Chemie GmbH

The Global Synthetic and Bio Emulsion Polymers Market was valued at USD 32.1 billion in 2025 and is estimated to grow at a CAGR of 3% to reach USD 43 billion by 2035.

Over the years, synthetic and bio emulsion polymers have evolved from niche product offerings into vital materials supporting modern maritime operations and industrial applications. Their role now extends beyond basic sealing to enhancing structural integrity, corrosion resistance, and long-term performance of marine vessels. Sustainability trends are reshaping industry priorities, and these polymers are at the forefront of eco-friendly, high-performance solutions that reduce environmental impact in shipbuilding, maintenance, and retrofitting. Hybrid formulations, low-volatile organic compound systems, and renewable content polymers are gaining traction as industries respond to strict environmental regulations and global decarbonization goals. Market growth is strongly influenced by regional production priorities, with Asia Pacific leading due to high shipbuilding activity and expanding commercial fleets, creating substantial demand for reliable, high-performance emulsion polymer solutions. Technological advancements continue to enhance durability, chemical resistance, and adaptability, positioning the market for steady long-term growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $32.1 Billion |

| Forecast Value | $43 Billion |

| CAGR | 3% |

The paints and coatings segment accounted held 46.3% share in 2025 and is expected to grow at a CAGR of 3.2% through 2035. In this segment, polymers provide film-forming capabilities, durability, and resistance to environmental stress, making them essential for protective and decorative finishes. Strong bonding properties, particularly from acrylic and polyurethane dispersions, are highly valued in adhesives for industrial and structural applications.

The synthetic emulsion polymers, containing 0-24% renewable carbon, dominated the market in 2025 with a 95.5% share and are projected to grow at a CAGR of 2.4% through 2035. These formulations are widely preferred in coatings, adhesives, and construction for their mechanical strength, chemical resistance, and long-term stability in demanding environments, making them more relied upon than bio-based alternatives in many industrial sectors.

North America Synthetic and Bio Emulsion Polymers Market accounted for 21.9% share in 2025. The region's advanced manufacturing capabilities, supportive regulatory environment, and increasing adoption of sustainable practices have positioned it as a key center for synthetic and bio emulsion polymers. Industries in the region demand high-performance formulations that meet stringent environmental and innovation-driven standards, supporting applications in coatings, adhesives, and construction.

Key players operating in the Global Synthetic and Bio Emulsion Polymers Market include Wacker Chemie AG, Covestro AG, BASF SE, Trinseo PLC, Arkema S.A., Celanese Corporation, Synthomer PLC, The Dow Chemical Company, Dairen Chemical Corporation, Asahi Kasei Corporation, Mallard Creek Polymers, Encres Dubuit, Shenzhen Jitian Chemical, Organik Kimya, and Indulor Chemie GmbH. Companies in the Synthetic and Bio Emulsion Polymers Market strengthen their market presence by investing in research and development to create innovative, high-performance, and sustainable formulations. They focus on expanding production capabilities, diversifying product portfolios with hybrid and low-VOC polymers, and forming strategic partnerships with industrial end-users. Emphasizing regulatory compliance, sustainability certifications, and quality assurance helps build trust with clients, while targeting emerging regions and expanding distribution networks ensures long-term market growth and enhanced competitive positioning.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Polymer Type

- 2.2.3 Application

- 2.2.4 End Use

- 2.2.5 Renewable Content

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for eco-friendly and sustainable products

- 3.2.1.2 Rising applications in paints, coatings, and adhesives industries

- 3.2.1.3 Advancements in polymerization technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fluctuating raw material prices

- 3.2.2.2 Stringent environmental regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Development of bio-based emulsion polymers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By polymer type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Polymer Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Acrylics

- 5.3 Vinyl acetate polymers

- 5.4 Styrene-butadiene latex (SBR)

- 5.5 Styrene-acrylic copolymers

- 5.6 Vinyl-acrylic copolymers

- 5.7 Polyurethane dispersions (puds)

- 5.8 Bio-based emulsion polymers

- 5.8.1 Bio-based acrylics (renewable monomers)

- 5.8.2 Bio-based styrene-butadiene

- 5.8.3 Natural latex (rubber tree derived)

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Paints & coatings

- 6.2.1 Architectural coatings (interior & exterior)

- 6.2.2 Industrial coatings

- 6.2.3 Protective coatings

- 6.3 Adhesives

- 6.3.1 Pressure-sensitive adhesives (psa)

- 6.3.2 Laminating adhesives

- 6.3.3 Assembly adhesives

- 6.3.4 Others

- 6.4 Paper & paperboard coatings

- 6.4.1 Paper coating (gloss, matte, silk)

- 6.4.2 Paperboard coating (folding carton, corrugated)

- 6.4.3 Others

- 6.5 Construction & cement modification

- 6.5.1 Cement additives & modifiers

- 6.5.2 Waterproofing membranes

- 6.5.3 Tile adhesives & grouts

- 6.5.4 Exterior insulation finishing systems (eifs)

- 6.5.5 Others

- 6.6 Textiles & nonwovens

- 6.6.1 Textile finishing & coating

- 6.6.2 Carpet backing

- 6.6.3 Others

- 6.7 Asphalt modification

- 6.7.1 Road construction & maintenance applications

- 6.7.2 Roofing applications

- 6.7.3 Others

- 6.8 Sealants

- 6.9 Others (printing inks, floor care, leather finishing)

Chapter 7 Market Estimates and Forecast, By Renewable Content, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Synthetic emulsion polymers (0-24% renewable carbon)

- 7.3 Bio-based emulsion polymers (≥25% renewable carbon)

- 7.3.1 Low bio-content (25-49% renewable carbon)

- 7.3.2 Medium bio-content (50-74% renewable carbon)

- 7.3.3 High bio-content (≥75% renewable carbon)

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 The Dow Chemical Company

- 9.3 Wacker Chemie AG

- 9.4 Celanese Corporation

- 9.5 Arkema S.A.

- 9.6 Trinseo PLC

- 9.7 Covestro AG

- 9.8 Synthomer PLC

- 9.9 Dairen Chemical Corporation

- 9.10 Asahi Kasei Corporation

- 9.11 Mallard Creek Polymers

- 9.12 Encres Dubuit

- 9.13 Organik Kimya

- 9.14 Shenzhen Jitian Chemical

- 9.15 Indulor Chemie GmbH