|

市场调查报告书

商品编码

1928954

化学废热回收系统市场机会、成长要素、产业趋势分析及2026年至2035年预测Chemical Waste Heat Recovery Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

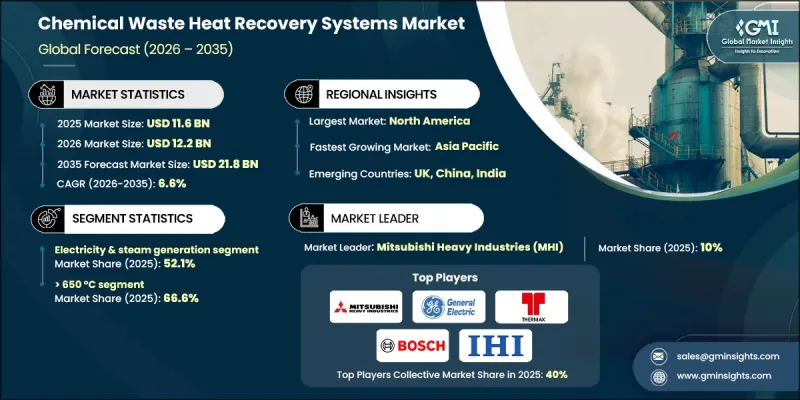

全球化学废热回收系统市场预计到 2025 年将达到 116 亿美元,到 2035 年将达到 218 亿美元,年复合成长率为 6.6%。

成长的驱动力来自大型化学企业设定的更严格的脱碳目标,这些企业日益重视减少燃料蒸气的产生和製程热的消耗。废热回收正被广泛采用,成为提高能源效率并减少排放的直接且经济有效的解决方案。随着企业将排放目标与营运绩效指标挂钩,这些系统正日益被视为策略性投资,而非可有可无的升级。这种转变有助于在能源成本波动的情况下稳定营运利润率。随着客户对低碳化工产品的需求日益增长,内部碳计量和产品级排放追踪的普及进一步加速了这项需求。法规结构也透过要求在核准新产能之前进行详细的能源评估和剩余热能回收,加强了以效率为先的规划。财政奖励和支持性政策结构使得这些系统的实施更加便捷,也更容易纳入长期资本规划。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 116亿美元 |

| 预测金额 | 218亿美元 |

| 复合年增长率 | 6.6% |

预计到 2025 年,电力和蒸气发电领域将占 52.1% 的市场份额,到 2035 年将以 7.5% 的复合年增长率成长。化学製造商正越来越多地将回收的热量转化为可用能源,以满足现场电力和蒸气需求,同时降低排放强度。

预计到 2025 年,运作温度高于 650°C 的系统将占市场份额的 66.6%,到 2035 年将以 6% 的复合年增长率增长。高温製程会产生大量可回收的热量,而回收这种能量正成为能源密集型化学製程中下一代热效率策略的核心。

2025年,美国化工废热回收系统市场价值47亿美元,占全球市场份额的82%。区域成长得益于有利的政策机制,这些机制支持效率投资,并加速化学和石化设施采用先进的废热回收解决方案。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 监管环境

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 成长潜力分析

- 波特分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- PESTEL 分析

- 新的机会与趋势

- 数位化和物联网集成

- 拓展新兴市场

第四章 竞争情势

- 介绍

- 公司市占率分析

- 策略倡议

- 竞争标竿分析

- 战略仪錶板

- 创新与科技趋势

第五章 依应用领域分類的市场规模及预测(2022-2035年)

- 预热

- 电力和蒸气发电

- 蒸气朗肯迴圈

- 有机朗肯迴圈

- 卡琳娜循环

- 其他的

第六章 依温度分類的市场规模及预测(2022-2035年)

- 低于 230°C

- 230°C~650°C

- 超过650℃

第七章 2022-2035年各地区市场规模及预测

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 法国

- 德国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 拉丁美洲

- 巴西

- 阿根廷

第八章 公司简介

- Aura

- BIHL

- Bosch

- Climeon

- Cochran

- Durr Group

- Echogen

- Exergy International

- Forbes Marshall

- General Electric

- IHI Power Systems

- John Wood Group

- Mitsubishi Heavy Industries

- Ormat

- Promec Engineering

- Rentech Boilers

- Siemens Energy

- Sofinter

- Thermax

- Viessmann

The Global Chemical Waste Heat Recovery Systems Market was valued at USD 11.6 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 21.8 billion by 2035.

Growth is supported by stricter decarbonization targets set by large chemical producers, with increasing focus on reducing fuel-based steam generation and process heat consumption. Waste heat recovery is being adopted as a direct and cost-effective solution to lower emissions while improving energy efficiency. As companies align emissions targets with operational performance metrics, these systems are increasingly viewed as strategic investments rather than optional upgrades. This shift helps stabilize operating margins amid fluctuating energy costs. Broader adoption of internal carbon accounting and product-level emissions tracking is further accelerating demand, as customers increasingly expect lower-carbon chemical outputs. Regulatory frameworks are also reinforcing efficiency-first planning by requiring detailed energy assessments and recovery of excess thermal energy before approving new capacity. Financial incentives and supportive policy structures are making these systems easier to justify and integrate into long-term capital programs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.6 Billion |

| Forecast Value | $21.8 Billion |

| CAGR | 6.6% |

The electricity and steam generation segment accounted for 52.1% share in 2025 and is projected to grow at a CAGR of 7.5% through 2035. Chemical producers are increasingly converting recovered heat into usable energy to support on-site power and steam needs while reducing emissions intensity.

The systems operating above 650°C represented 66.6% share in 2025 and are expected to grow at a CAGR of 6% by 2035. High-temperature processes generate substantial recoverable heat, and capturing this energy is becoming central to next-generation thermal efficiency strategies across energy-intensive chemical operations.

U.S. Chemical Waste Heat Recovery Systems Market held 82% share in 2025 and generated USD 4.7 billion. Regional growth is being driven by favorable policy mechanisms that support efficiency investments and accelerate the adoption of advanced heat recovery solutions across chemical and petrochemical facilities.

Key companies active in the Global Chemical Waste Heat Recovery Systems Market include Siemens Energy, Mitsubishi Heavy Industries, General Electric, Bosch, Thermax, Viessmann, John Wood Group, Ormat, Exergy International, Sofinter, Durr Group, IHI Power Systems, Rentech Boilers, Climeon, Forbes Marshall, Aura, BIHL, Cochran, Promec Engineering, and Echogen. Companies operating in the Chemical Waste Heat Recovery Systems Market are strengthening their positions through technology advancement, project integration capabilities, and strategic collaborations. Manufacturers are focusing on developing scalable, high-efficiency solutions that can be deployed across multiple plant configurations. Many players are expanding service offerings to include system design, optimization, and long-term maintenance to improve customer value. Geographic expansion into regions with strong regulatory support is also a key priority.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Application trends

- 2.1.3 Temperature trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter';s analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Application, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Pre-heating

- 5.3 Electricity & steam generation

- 5.3.1 Steam rankine cycle

- 5.3.2 Organic rankine cycle

- 5.3.3 Kalina cycle

- 5.4 Other

Chapter 6 Market Size and Forecast, By Temperature, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 < 230°C

- 6.3 230°C - 650 °C

- 6.4 > 650 °C

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.3.5 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 South Africa

- 7.5.3 UAE

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Aura

- 8.2 BIHL

- 8.3 Bosch

- 8.4 Climeon

- 8.5 Cochran

- 8.6 Durr Group

- 8.7 Echogen

- 8.8 Exergy International

- 8.9 Forbes Marshall

- 8.10 General Electric

- 8.11 IHI Power Systems

- 8.12 John Wood Group

- 8.13 Mitsubishi Heavy Industries

- 8.14 Ormat

- 8.15 Promec Engineering

- 8.16 Rentech Boilers

- 8.17 Siemens Energy

- 8.18 Sofinter

- 8.19 Thermax

- 8.20 Viessmann

2026年全球余热回收市场报告

2026年全球余热回收市场报告 废热回收系统市场:按类型、组件、安装配置、容量和最终用户划分-2026-2032年全球市场预测

废热回收系统市场:按类型、组件、安装配置、容量和最终用户划分-2026-2032年全球市场预测 水泥废热回收系统市场规模、份额和成长分析:按循环技术、热源位置、系统元件、产量和地区划分 - 产业预测,2026-2033年

水泥废热回收系统市场规模、份额和成长分析:按循环技术、热源位置、系统元件、产量和地区划分 - 产业预测,2026-2033年 余热回收锅炉市场规模、份额、趋势和预测:按类型、余热温度、余热来源、方向、最终用途行业和地区划分,2026-2034年基于工质、功率范围、系统配置、应用和终端用户产业的ORC低温废热发电系统市场全球预测(2026-2032年)日本绿色水泥市场规模、份额、趋势及预测(按类型、原料、应用、最终用户及地区划分),2026-2034年

余热回收锅炉市场规模、份额、趋势和预测:按类型、余热温度、余热来源、方向、最终用途行业和地区划分,2026-2034年基于工质、功率范围、系统配置、应用和终端用户产业的ORC低温废热发电系统市场全球预测(2026-2032年)日本绿色水泥市场规模、份额、趋势及预测(按类型、原料、应用、最终用户及地区划分),2026-2034年 废热回收系统市场 - 全球产业规模、份额、趋势、机会及预测(按应用、温度、最终用途、地区和竞争格局划分,2021-2031年)锅炉余热回收系统市场按技术、结构材料、热源温度、最终用途产业和安装类型划分-2026-2032年全球预测

废热回收系统市场 - 全球产业规模、份额、趋势、机会及预测(按应用、温度、最终用途、地区和竞争格局划分,2021-2031年)锅炉余热回收系统市场按技术、结构材料、热源温度、最终用途产业和安装类型划分-2026-2032年全球预测 废热回收系统市场规模、份额及成长分析(按应用、终端用户产业、组件、温度及地区划分)-2026-2033年产业预测

废热回收系统市场规模、份额及成长分析(按应用、终端用户产业、组件、温度及地区划分)-2026-2033年产业预测 金属製造余热回收系统市场机会、成长动力、产业趋势分析及2025-2034年预测

金属製造余热回收系统市场机会、成长动力、产业趋势分析及2025-2034年预测