|

市场调查报告书

商品编码

1928973

自主移动机器人市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Autonomous Mobile Robots (AMR) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

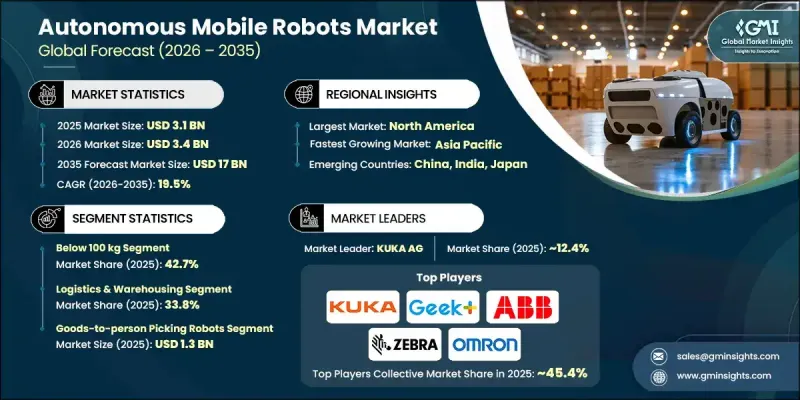

全球自主移动机器人(AMR)市场预计到 2025 年将达到 31 亿美元,到 2035 年将达到 170 亿美元,年复合成长率为 19.5%。

这一市场成长反映了物流、製造、医疗保健和服务型产业对自动化日益增长的需求。各组织正在扩大自主移动机器人的应用范围,以提高职场安全、提升营运效率并减少对人力的依赖。随着自动化倡议的扩展和运营的日益复杂,对智慧机器人解决方案的需求持续增长。物料搬运能力的进步使机器人能够处理更大的负载容量,从而缩短工作週期并提高整个设施的工作流程效率。人工智慧 (AI) 和机器学习如今已成为自主系统的核心组成部分,实现了自适应导航、即时决策和高阶资料处理。这些能力使机器人能够在动态环境中高效运行,同时提高精度和可靠性。随着全球数位转型的加速,自主移动机器人正成为多个产业现代营运策略的重要组成部分。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 31亿美元 |

| 预测金额 | 170亿美元 |

| 复合年增长率 | 19.5% |

到2025年,有效载荷低于100公斤的机器人将占据42.7%的市场。该细分市场的机器人专为轻型任务而设计,并针对能源效率、精确导航和紧凑外形规格进行了最佳化。製造商优先考虑电池续航时间长、运动控制精准、有效载荷处理安全以及经济高效的扩充性,以满足该有效载荷范围内的各种操作需求。

预计2026年至2035年,电子和半导体产业将以20.8%的复合年增长率成长。这一成长主要受自动化需求增加、对更高製造精度、更快生产週期和更严格品质标准的需求所推动。持续的技术创新、灵活的生产能力以及对研发的持续投入,对于进入该领域的製造商仍然至关重要。

预计2025年,北美自主移动机器人(AMR)市占率将达到33.5%。该地区的成长主要得益于先进製造技术的应用、对自动化物流解决方案日益增长的需求、人事费用的上升以及对机器人创新领域的大力投资。智慧製造技术与弹性自动化系统的融合将持续巩固该地区的市场领先地位。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 生态系分析

- 产业影响因素

- 司机

- 电子商务和仓储自动化的发展

- 自主移动机器人在医疗和製药领域的扩展

- 自主移动机器人(AMR)在农业和食品加工的应用

- 提高工业和物流营运的安全性和效率

- 自主移动机器人(AMR)在饭店业的应用不断扩展

- 挑战与困难

- 自主移动机器人高成本

- 自主移动机器人技术(AMR)整合与部署面临的挑战

- 市场机会

- 拓展最后一公里配送业务

- 智慧工厂集成

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 永续性措施

- 消费者心理分析

- 专利和智慧财产权分析

- 地缘政治和贸易趋势

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 地理分布比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年主要发展动态

- 併购

- 合作伙伴关係和合资企业

- 技术进步

- 扩张与投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/Start-Ups竞赛的趋势

第五章 按组件分類的市场估算与预测,2022-2035年

- 硬体

- 软体和服务

第六章 按类型分類的市场估算与预测,2022-2035年

- 产品运输拣选机器人

- 自动堆高机

- 自主库存控制机器人

- 无人机

7. 依负载容量分類的市场估计与预测,2022-2035 年

- 体重低于100公斤

- 100kg~500kg

- 超过500公斤

8. 2022-2035年导航技术市场估算与预测

- 雷射/光达

- 视觉引导

- 其他的

第九章 依电池类型分類的市场估计与预测,2022-2035年

- 铅酸电池

- 锂离子电池

- 镍基电池

- 其他的

第十章 依应用领域分類的市场估计与预测,2022-2035年

- 选拔

- 运输

- 组装

- 库存管理

- 其他的

第十一章 依最终用途产业分類的市场估计与预测,2022-2035年

- 物流/仓储业

- 零售

- 车

- 电子装置和半导体

- 製药和医疗保健

- 食品/饮料

- 航太/国防

- 饭店业

- 其他的

第十二章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十三章:公司简介

- 主要企业

- ABB Ltd.

- KUKA AG

- Omron Corporation

- Zebra Technologies Corp.

- 按地区分類的主要企业

- 北美洲

- Aethon, Inc.

- Vecna Robotics

- ForwardX Robotics

- Mobile Industrial Robots

- 亚太地区

- Geekplus Technology Co., Ltd.

- YUJIN ROBOT Co., Ltd.

- Honda Motor Co., Ltd.

- 欧洲

- Fanuc

- GreyOrange

- Locus Robotics

- Murata Machinery, Ltd.

- 北美洲

- 小众玩家/颠覆者

- Balyo

- Boston Dynamics

- Onward Robotics

- Seegrid

- Teradyne Inc.

- JBT

The Global Autonomous Mobile Robots (AMR) Market was valued at USD 3.1 billion in 2025 and is estimated to grow at a CAGR of 19.5% to reach USD 17 billion by 2035.

Market growth reflects the rising need for automation across logistics, manufacturing, healthcare, and service-oriented environments. Organizations are increasingly deploying autonomous mobile robots to improve workplace safety, enhance operational efficiency, and reduce dependency on manual labor. Expanding automation initiatives, combined with rising operational complexity, continue to strengthen demand for intelligent robotic solutions. Advances in load-handling capabilities allow robots to manage larger payloads, reducing task cycles and improving workflow efficiency across facilities. Artificial intelligence and machine learning are now core components of autonomous systems, enabling adaptive navigation, real-time decision-making, and advanced data processing. These capabilities allow robots to function effectively in dynamic settings while improving precision and reliability. As digital transformation accelerates globally, autonomous mobile robots are becoming an essential part of modern operational strategies across multiple industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.1 Billion |

| Forecast Value | $17 Billion |

| CAGR | 19.5% |

The below 100 kg payload category accounted for 42.7% share in 2025. Robots in this segment are designed for lightweight operations and are optimized for energy efficiency, precise navigation, and compact form factors. Manufacturers emphasize extended battery life, accurate movement control, secure payload handling, and cost-effective scalability to meet diverse operational requirements within this payload range.

The electronics and semiconductor segment is expected to grow at a CAGR of 20.8% during 2026-2035. Growth is supported by increasing automation requirements, demand for higher manufacturing precision, faster production cycles, and strict quality standards. Continuous innovation, flexible production capabilities, and sustained investment in research and development remain critical for manufacturers serving this segment.

North America Autonomous Mobile Robots (AMR) Market held a 33.5% share in 2025. Regional growth is driven by advanced manufacturing adoption, rising demand for automated logistics solutions, increasing labor costs, and strong investment in robotics innovation. The integration of smart manufacturing technologies and flexible automation systems continues to reinforce market leadership in the region.

Key companies operating in the Global Autonomous Mobile Robots (AMR) Market include ABB Ltd., Boston Dynamics, KUKA AG, Fanuc, Omron Corporation, Locus Robotics, Geekplus Technology Co., Ltd., GreyOrange, Mobile Industrial Robots, Zebra Technologies Corp., Teradyne Inc., Honda Motor Co., Ltd., Murata Machinery Ltd., ForwardX Robotics, Seegrid, Vecna Robotics, Aethon, Inc., JBT, Balyo, Onward Robotics, and YUJIN ROBOT Co., Ltd. Companies in the Global Autonomous Mobile Robots (AMR) Market strengthen their market position through continuous technological advancement, product diversification, and strategic partnerships. Investment in artificial intelligence, navigation software, and sensor integration enhances robot autonomy and adaptability. Manufacturers focus on modular and scalable platforms to address varied operational needs across industries. Geographic expansion and collaboration with logistics, manufacturing, and technology providers support broader market penetration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Component trends

- 2.2.2 Type trends

- 2.2.3 Payload capacity trends

- 2.2.4 Navigation technology trends

- 2.2.5 Battery type trends

- 2.2.6 Application trends

- 2.2.7 End use industry trends

- 2.2.8 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry ecosystem analysis

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growth of e-commerce and warehouse automation

- 3.3.1.2 Expansion of AMRs in healthcare and pharmaceuticals

- 3.3.1.3 Adoption of AMRs in agriculture and food processing

- 3.3.1.4 Enhanced safety and efficiency in industrial and logistics operations

- 3.3.1.5 Increasing application of AMRs in the hospitality industry

- 3.3.2 Pitfalls and challenges

- 3.3.2.1 High cost associated with autonomous mobile robots

- 3.3.2.2 Challenges in integration and deployment of AMR technologies

- 3.3.3 Market opportunities

- 3.3.3.1 Expansion in last-mile delivery

- 3.3.3.2 Integration with smart factories

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter';s analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Emerging Business Models

- 3.10 Compliance Requirements

- 3.11 Sustainability Measures

- 3.12 Consumer Sentiment Analysis

- 3.13 Patent and IP analysis

- 3.14 Geopolitical and trade dynamics

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software & services

Chapter 6 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Goods-to-person picking robots

- 6.3 Self-driving forklifts

- 6.4 Autonomous inventory robots

- 6.5 Unmanned aerial vehicles

Chapter 7 Market Estimates and Forecast, By Payload Capacity, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Below 100 kg

- 7.3 100 kg - 500 kg

- 7.4 More than 500 kg

Chapter 8 Market Estimates and Forecast, By Navigation Technology, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Laser/lidar

- 8.3 Vision guidance

- 8.4 Others

Chapter 9 Market Estimates and Forecast, By Battery Type, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 Lead battery

- 9.3 Lithium-ion battery

- 9.4 Nickel-based battery

- 9.5 Others

Chapter 10 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 10.1 Key trends

- 10.2 Sorting

- 10.3 Transportation

- 10.4 Assembly

- 10.5 Inventory management

- 10.6 Others

Chapter 11 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Million & Units)

- 11.1 Key trends

- 11.2 Logistics & warehousing

- 11.3 Retail

- 11.4 Automotive

- 11.5 Electronics & semiconductor

- 11.6 Pharmaceuticals & healthcare

- 11.7 Food & beverage

- 11.8 Aerospace & defense

- 11.9 Hospitality

- 11.10 Others

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global Key Players

- 13.1.1 ABB Ltd.

- 13.1.2 KUKA AG

- 13.1.3 Omron Corporation

- 13.1.4 Zebra Technologies Corp.

- 13.2 Regional key players

- 13.2.1 North America

- 13.2.1.1 Aethon, Inc.

- 13.2.1.2 Vecna Robotics

- 13.2.1.3 ForwardX Robotics

- 13.2.1.4 Mobile Industrial Robots

- 13.2.2 Asia Pacific

- 13.2.2.1 Geekplus Technology Co., Ltd.

- 13.2.2.2 YUJIN ROBOT Co., Ltd.

- 13.2.2.3 Honda Motor Co., Ltd.

- 13.2.3 Europe

- 13.2.3.1 Fanuc

- 13.2.3.2 GreyOrange

- 13.2.3.3 Locus Robotics

- 13.2.3.4 Murata Machinery, Ltd.

- 13.2.1 North America

- 13.3 Niche Players/Disruptors

- 13.3.1 Balyo

- 13.3.2 Boston Dynamics

- 13.3.3 Onward Robotics

- 13.3.4 Seegrid

- 13.3.5 Teradyne Inc.

- 13.3.6 JBT

全球自主移动机器人 (AMR) 市场(至 2032 年)按导航方式(雷射/雷射雷达、视觉引导、SLAM、RFID 标籤、磁感测器、惯性感测器)、类型(货物搬运 AMR、托盘搬运 AMR)和负载容量(100 公斤以下、100-500 公斤、500 公斤以上)划分

全球自主移动机器人 (AMR) 市场(至 2032 年)按导航方式(雷射/雷射雷达、视觉引导、SLAM、RFID 标籤、磁感测器、惯性感测器)、类型(货物搬运 AMR、托盘搬运 AMR)和负载容量(100 公斤以下、100-500 公斤、500 公斤以上)划分 2026年全球自主移动机器人市场报告

2026年全球自主移动机器人市场报告 自主移动机器人 (AMR) 市场规模、占有率及预测:依感测器类型(雷射雷达、视觉、雷达、超音波)、感测器融合演算法、SLAM 技术及应用(仓库、工厂、户外)划分 - 全球预测至 2036 年2026年全球室内机器人导航雷射雷达市场报告

自主移动机器人 (AMR) 市场规模、占有率及预测:依感测器类型(雷射雷达、视觉、雷达、超音波)、感测器融合演算法、SLAM 技术及应用(仓库、工厂、户外)划分 - 全球预测至 2036 年2026年全球室内机器人导航雷射雷达市场报告 全球自主移动机器人市场,2026-2030年

全球自主移动机器人市场,2026-2030年 AI配送机器人市场按运作模式、技术、组件、应用、最终用户和分销管道划分,全球预测(2026-2032年)

AI配送机器人市场按运作模式、技术、组件、应用、最终用户和分销管道划分,全球预测(2026-2032年) 自主移动机器人市场规模、份额和趋势分析报告:按组件、类型、电池类型、应用、负载容量、导航技术、最终用途、地区和细分市场预测(2026-2033 年)

自主移动机器人市场规模、份额和趋势分析报告:按组件、类型、电池类型、应用、负载容量、导航技术、最终用途、地区和细分市场预测(2026-2033 年) 全球自主移动机器人市场-按类型、组件、最终用途产业、地区和竞争格局分類的产业规模、份额、趋势、机会和预测(2021-2031年预测)

全球自主移动机器人市场-按类型、组件、最终用途产业、地区和竞争格局分類的产业规模、份额、趋势、机会和预测(2021-2031年预测) 自主移动机器人市场预测至2032年:按组件、类型、导航技术、负载容量、应用、最终用户和地区分類的全球分析

自主移动机器人市场预测至2032年:按组件、类型、导航技术、负载容量、应用、最终用户和地区分類的全球分析 用于货物运输的自主移动机器人(AMR)-全球市场份额和排名、总收入和需求预测(2025-2031年)

用于货物运输的自主移动机器人(AMR)-全球市场份额和排名、总收入和需求预测(2025-2031年)