|

市场调查报告书

商品编码

1928976

干涉合成孔径雷达市场机会、成长要素、产业趋势分析及2026年至2035年预测Interferometric Synthetic Aperture Radar (InSAR) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球干涉合成孔径雷达(InSAR)市场预计到 2025 年将达到 5.692 亿美元,到 2035 年将达到 15 亿美元,年复合成长率为 10%。

这一增长轨蹟的驱动力源于对高精度地表监测日益增长的需求、雷达数据与人工智慧、机器学习和云端分析技术的融合,以及其在能源、自然资源和公共部门航太专案中的广泛应用。具备频繁重访能力的卫星星系的日益普及,持续提升了资料的可用性和监测精度。该技术能够提供不受天气或光照条件影响的一致、广域测量数据,这使其在长期规划、风险缓解和资产管理中的重要性日益凸显。随着分析平台的日趋成熟,各组织机构越来越依赖干涉合成孔径雷达的洞察数据来支援预测建模和营运决策。政府支持的观测项目和商业性应用增强了市场的扩充性,而处理技术和平台整合的持续创新则扩大了其在各行业的应用范围。这些因素共同促成了干涉合成孔径雷达成为支援基础设施韧性、环境监测和全球战略规划的关键地理空间情报工具。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 5.692亿美元 |

| 预测金额 | 15亿美元 |

| 复合年增长率 | 10% |

由于干涉雷达能够探测地表随时间推移发生的细微变化,因此持续维护和监测应用正加速普及。持续观测有助于制定预防性维护计划,降低结构故障的可能性,减少长期维修成本,并增强灾害应对策略。在能源和资源领域,该技术发挥日益重要的作用,它能够精确测量作业区域周围的地面运动,从而帮助实现安全目标,最大限度地减少环境影响,并提高合规性。大规模监测增强了预测性维护和运作风险评估,同时减少了对人工巡检的依赖。

截至2025年,双影像合成孔径雷达市场规模达3.317亿美元。该技术因其实施成本低、处理简单以及在形变和稳定性评估方面具有可靠的精度而广泛应用。对于许多用户而言,它在解析度品质和高效工作流程之间取得了良好的平衡,无需采用更复杂的多影像技术。

机载和天载平台是主要的应用类别,到 2025 年市场规模将达到 3.225 亿美元。这些平台提供广泛的地理覆盖范围和一致的观测週期,使其成为需要频繁数据更新和广域可视性的大规模监视和国家观测倡议必不可少的工具。

预计到2025年,北美干涉合成孔径雷达(InSAR)市场份额将达到33.5%,并透过对先进分析、太空技术和监视解决方案的持续投资,保持主导地位。公共和商业领域的广泛应用,正在提升对高解析度雷达资料集和分析服务的需求,进一步巩固了该地区市场的优势。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 基础设施监控和维护

- 与人工智慧、机器学习和云端分析的集成

- 石油、天然气和采矿应用

- 国防和政府航太计划

- 卫星星系和频繁重访

- 挑战与困难

- 安装和系统成本高昂

- 技术复杂性和技能要求

- 机会:

- 基础设施韧性与智慧城市计划

- 环境监测与灾害管理

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 永续发展倡议

- 供应链韧性

- 地缘政治分析

- 数位转型

- 併购和策略联盟

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 按地区分類的企业发展比较

- 全球企业发展分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 产品系列比较

- 2022-2025 年主要发展动态

- 併购

- 合作伙伴关係和合资企业

- 技术进步

- 扩张与投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/Start-Ups竞赛的趋势

第五章 按类型分類的市场估算与预测,2022-2035年

- 两幅合成孔径雷达(SAR)影像

- 多幅合成孔径雷达(SAR)影像

第六章 2022-2035年各平台市场估算与预测

- 机载和星载

- 地面类型

- 其他的

7. 2022-2035年按组件分類的市场估算与预测

- 硬体

- 软体

- 服务

第八章 按应用领域分類的市场估算与预测,2022-2035年

- 导航

- 影响评估

- 洪水和干旱

- 地震灾害

- 露天矿

- 其他的

- 监测

- 地层下陷和地壳运动

- 基础设施稳定性

- 冰川和冰盖

- 火山活动

- 其他的

- 地图绘製与规划

- 其他的

9. 依最终用途分類的市场估计与预测,2022-2035 年

- 航太/国防

- 农业

- 土木工程/建筑

- 环境监测

- 矿业

- 石油和天然气

- 其他的

第十章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第十一章:公司简介

- 主要企业

- Airbus Defence and Space

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Raytheon Technologies

- Thales Group

- BAE Systems

- Leonardo SpA

- L3 Harris Technologies

- 按地区分類的主要企业

- 北美洲

- Capella Space

- MDA Ltd.

- Orbital Insight

- SkyGeo

- 欧洲

- GAMMA Remote Sensing AG

- CGG

- Tre Altamira

- Tele-Rilevamento Europa

- sarmap SA

- 亚太地区

- ICEYE

- Synspective

- 北美洲

- 小众/颠覆性公司

- 3vGeomatics

- GroundProbe

- PCI Geomatics

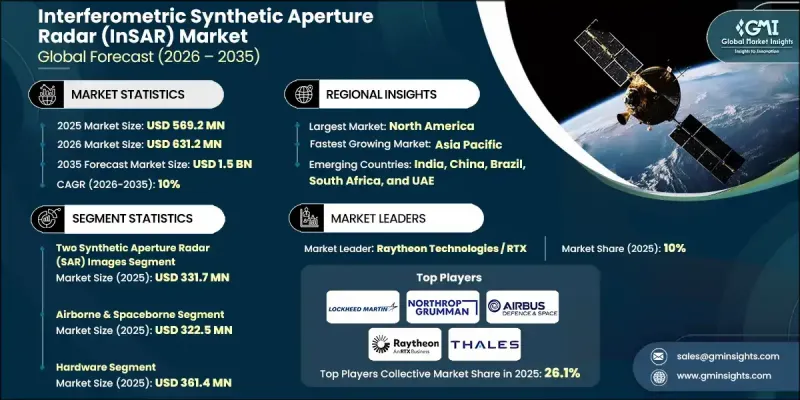

The Global Interferometric Synthetic Aperture Radar (InSAR) Market was valued at USD 569.2 million in 2025 and is estimated to grow at a CAGR of 10% to reach USD 1.5 billion by 2035.

The growth trajectory is driven by rising demand for high-precision surface monitoring, the convergence of radar data with artificial intelligence, machine learning, and cloud-based analytics, and expanding use across energy, natural resource, and public-sector space initiatives. The increasing deployment of satellite constellations with frequent revisit capabilities continues to enhance data availability and improve monitoring accuracy. Technology's ability to deliver consistent, large-area measurements regardless of weather or lighting conditions has elevated its importance for long-term planning, risk mitigation, and asset management. As analytical platforms mature, organizations increasingly rely on interferometric radar insights to support predictive modeling and operational decision-making. Government-backed observation programs and commercial adoption are reinforcing market scalability, while continuous innovation in processing techniques and platform integration is expanding accessibility across industries. These combined factors position interferometric synthetic aperture radar as a critical geospatial intelligence tool supporting infrastructure resilience, environmental oversight, and strategic planning worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $569.2 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 10% |

Ongoing maintenance and monitoring applications are accelerating adoption due to the capability of interferometric radar to detect minute surface changes over time. Continuous observation supports proactive maintenance planning, lowers the probability of structural failures, reduces long-term repair costs, and strengthens disaster readiness strategies. In the energy and resource sectors, technology plays a growing role by enabling precise measurement of land movement around operational zones, supporting safety objectives, minimizing environmental exposure, and improving regulatory compliance. Large-scale monitoring reduces dependence on manual inspections while enhancing predictive maintenance and operational risk assessment.

The two-image synthetic aperture radar segment reached USD 331.7 million in 2025. This method remains widely adopted due to its lower implementation costs, reduced processing complexity, and reliable accuracy for deformation and stability assessments. For many users, the balance between resolution quality and streamlined workflows eliminates the need for more complex multi-image techniques.

The airborne and spaceborne platforms formed the leading deployment category, generating USD 322.5 million in 2025. These platforms support extensive geographic coverage and consistent observation cycles, making them essential for large-scale monitoring and national observation initiatives that require frequent data updates and broad visibility.

North America Interferometric Synthetic Aperture Radar (InSAR) Market accounted for 33.5% share in 2025, maintaining leadership through sustained investment in advanced analytics, space technologies, and monitoring solutions. Strong adoption across public agencies and commercial sectors has increased demand for high-resolution radar datasets and analytical services, reinforcing regional market strength.

Key companies active in the Global Interferometric Synthetic Aperture Radar (InSAR) Market include Airbus Defence and Space, ICEYE, Capella Space, Lockheed Martin Corporation, Northrop Grumman Corporation, Leonardo S.p.A., Thales Group, Raytheon Technologies, L3Harris Technologies, BAE Systems, MDA Ltd., Synspective, GAMMA Remote Sensing AG, CGG, GroundProbe, Orbital Insight, PCI Geomatics, SkyGeo, sarmap SA, Tre Altamira, Tele-Rilevamento Europa, and 3vGeomatics. Companies in the Global Interferometric Synthetic Aperture Radar (InSAR) Market strengthen their competitive position through continuous technology innovation, expansion of satellite and airborne capabilities, and integration of advanced analytics. Strategic investments in AI-driven data processing and cloud-based delivery platforms improve scalability and customer accessibility. Partnerships with government agencies, infrastructure operators, and energy companies help secure long-term contracts and recurring revenue streams.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Platform trends

- 2.2.3 Component trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Infrastructure monitoring & maintenance

- 3.2.1.2 Integration with AI, ML, and cloud analytics

- 3.2.1.3 Oil, gas & mining applications

- 3.2.1.4 Defense & government space programs

- 3.2.1.5 Satellite constellations & high-frequency revisit

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High deployment & system costs

- 3.2.2.2 Technical complexity & skill requirements

- 3.2.3 Opportunities:

- 3.2.3.1 Infrastructure Resilience & Smart City Projects

- 3.2.3.2 Environmental Monitoring & Disaster Management

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Initiatives

- 3.11 Supply Chain Resilience

- 3.12 Geopolitical Analysis

- 3.13 Digital Transformation

- 3.14 Mergers, Acquisitions, and Strategic Partnerships Landscape

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Two Synthetic Aperture Radar (SAR) Images

- 5.3 Multiple Synthetic Aperture Radar (SAR) Images

Chapter 6 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Airborne & spaceborne

- 6.3 Ground-based

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Hardware

- 7.3 Software

- 7.4 Services

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Navigation

- 8.3 Impact assessment

- 8.3.1 Flood and drought

- 8.3.2 Seismic hazard

- 8.3.3 Open-pit mine

- 8.3.4 Others

- 8.4 Monitoring

- 8.4.1 Subsidence & field

- 8.4.2 Infrastructure stability

- 8.4.3 Glacier and ice sheet

- 8.4.4 Volcanic activity

- 8.4.5 Others

- 8.5 Mapping & planning

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By End use, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Aerospace & defense

- 9.3 Agriculture

- 9.4 Civil engineering & construction

- 9.5 Environmental monitoring

- 9.6 Mining

- 9.7 Oil & gas

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Airbus Defence and Space

- 11.1.2 Lockheed Martin Corporation

- 11.1.3 Northrop Grumman Corporation

- 11.1.4 Raytheon Technologies

- 11.1.5 Thales Group

- 11.1.6 BAE Systems

- 11.1.7 Leonardo S.p.A.

- 11.1.8. L3 Harris Technologies

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 Capella Space

- 11.2.1.2 MDA Ltd.

- 11.2.1.3 Orbital Insight

- 11.2.1.4 SkyGeo

- 11.2.2 Europe

- 11.2.2.1 GAMMA Remote Sensing AG

- 11.2.2.2 CGG

- 11.2.2.3 Tre Altamira

- 11.2.2.4 Tele-Rilevamento Europa

- 11.2.2.5 sarmap SA

- 11.2.3 Asia Pacific

- 11.2.3.1 ICEYE

- 11.2.3.2 Synspective

- 11.2.1 North America

- 11.3 Niche / Disruptors

- 11.3.1 3vGeomatics

- 11.3.2 GroundProbe

- 11.3.3 PCI Geomatics

合成孔径雷达卫星市场:按应用、最终用户、轨道类型、频段和组件分類的全球预测(2026-2032年)

合成孔径雷达卫星市场:按应用、最终用户、轨道类型、频段和组件分類的全球预测(2026-2032年) 全球合成孔径雷达市场规模、份额、趋势和成长分析报告(2026-2034年)

全球合成孔径雷达市场规模、份额、趋势和成长分析报告(2026-2034年) 星载合成孔径雷达 (SAR) 资料和服务市场:依频段(X 波段、L 波段、C 波段、S 波段)、成像模式(聚束、条带、扫描 SAR)、组件、应用和最终用户划分 - 全球预测至 2036 年

星载合成孔径雷达 (SAR) 资料和服务市场:依频段(X 波段、L 波段、C 波段、S 波段)、成像模式(聚束、条带、扫描 SAR)、组件、应用和最终用户划分 - 全球预测至 2036 年 合成孔径雷达市场-全球产业规模、份额、趋势、机会、预测:按应用、平台、频段、地区和竞争格局划分,2021-2031年

合成孔径雷达市场-全球产业规模、份额、趋势、机会、预测:按应用、平台、频段、地区和竞争格局划分,2021-2031年 合成孔径雷达市场规模、份额和成长分析(按组件、平台、频宽、模式、应用和地区划分)—产业预测(2026-2033 年)合成孔径雷达 (SAR) 成像市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测 (2024-2032)

合成孔径雷达市场规模、份额和成长分析(按组件、平台、频宽、模式、应用和地区划分)—产业预测(2026-2033 年)合成孔径雷达 (SAR) 成像市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测 (2024-2032) 合成孔径雷达市场规模、份额和趋势分析报告:2024-2030 年按组件、平台、频段、模式、应用、区域和细分市场进行的预测全球合成孔径雷达市场规模(按产品、应用、地区、范围和预测)

合成孔径雷达市场规模、份额和趋势分析报告:2024-2030 年按组件、平台、频段、模式、应用、区域和细分市场进行的预测全球合成孔径雷达市场规模(按产品、应用、地区、范围和预测) 合成孔径雷达 (SAR) 市场、机会、成长动力、产业趋势分析与预测,2024-2032 年

合成孔径雷达 (SAR) 市场、机会、成长动力、产业趋势分析与预测,2024-2032 年 2030 年亚太地区合成孔径雷达市场预测 - 区域分析 - 按组件、频段、应用、平台和模式

2030 年亚太地区合成孔径雷达市场预测 - 区域分析 - 按组件、频段、应用、平台和模式