|

市场调查报告书

商品编码

1928978

焊接设备及耗材市场机会、成长要素、产业趋势分析及2026年至2035年预测Welding Equipment and Consumables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球焊接设备和耗材市场预计到 2025 年将达到 147 亿美元,到 2035 年将达到 243 亿美元,年复合成长率为 5.2%。

快速的都市化和大规模基础设施建设推动了焊接行业的扩张,这需要可靠、高强度的焊接解决方案。现代化基础设施计划需要先进的焊接技术,以确保桥樑、铁路、公路和工业设施的耐久性和结构完整性。除了建筑业之外,向永续建筑方式的转变也推动了对创新焊接技术的需求,这些技术能够提高效率并最大限度地减少对环境的影响。公共和私营部门的基础设施投资正在创造持续的成长机会。同时,随着电动车和轻量化材料的应用,汽车和运输业正在经历转型,这进一步推动了对能够处理新型合金和复合材料的专用焊接设备和耗材的需求。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 147亿美元 |

| 预测金额 | 243亿美元 |

| 复合年增长率 | 5.2% |

预计到2025年,焊条市场规模将达到50亿美元,并在2035年之前以4.6%的复合年增长率成长。焊条因其经济高效、用途广泛以及在户外和恶劣环境下可靠运作而备受欢迎,使其成为建筑、维修和维护应用中不可或缺的材料。其坚固耐用的设计使其能够在其他焊材可能失效的环境中高效焊接,例如在风、雨和极端温度下。此外,焊条还与多种金属和合金相容,可在各种计划中提供一致的焊接品质。

预计到2025年,电弧焊接市占率将达到43.4%。电弧焊接的适应性和高效性使其成为汽车、建筑和重工业等对焊接品质要求极高的行业的核心技术。手工电弧焊接(SMAW)、气体保护金属电弧焊接(GMAW)和电弧焊接(SAW)等技术被广泛用于在各种金属和合金上实现持久、精确的焊接。

美国焊接设备及耗材市场预计到2025年将达到27亿美元,2026年至2035年的复合年增长率(CAGR)为5.7%。美国市场拥有强大的工业基础和高度发展的製造业,汽车、航太和能源产业自动化和机器人焊接系统的普及推动了对精密设备的需求。为满足严格的安全和品质标准,企业正加速投资尖端焊接技术和耗材,以支援先进的工业流程。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 产业影响因素

- 司机

- 基础设施建设和工业化

- 汽车和运输业的扩张

- 焊接工艺的技术进步

- 挑战与困难

- 较高的初始投资和维护成本

- 熟练劳动力短缺

- 机会

- 自动化和工业4.0的采用

- 可再生能源领域需求不断成长

- 司机

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 监管环境

- 北美洲

- 美国:消费品安全委员会(CPSC)联邦法规(CFR)第16篇第1512部分

- 加拿大:国际标准化组织(ISO)4210

- 欧洲

- 德国:德国标准化协会 (DIN) 欧洲标准 (EN) ISO 4210

- 英国:欧洲标准 (EN) ISO 4210/英国合格评定 (UKCA)

- 法国:欧洲标准 (EN) ISO 4210

- 亚太地区

- 中国:国家标准(GB)3565

- 印度:印度标准 (IS) 10613

- 日本:日本工业标准(JIS)D 9110

- 拉丁美洲

- 巴西:巴西技术标准协会 (ABNT) 巴西标准 (NBR) ISO 4210

- 墨西哥:国际标准化组织(ISO)4210

- 中东和非洲

- 南非:南非国家标准 (SANS) 311

- 沙乌地阿拉伯:沙乌地阿拉伯标准、计量和品质组织 (SASO) 海湾标准组织 (GSO) ISO 4210

- 北美洲

- 贸易统计(HS编码-8501)

- 主要进口国

- 主要出口国

- 波特分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 按类型分類的市场估算与预测,2022-2035年

- 棒状电极

- 单线

- 磁通绕组

- 缝纫线

- 其他(棒状电极、保护气体等)

第六章 按技术分類的市场估计与预测,2022-2035年

- 电弧焊接

- 电阻焊接

- 氧乙炔焊

- 固体焊接

- 其他(电子束等)

第七章 按应用领域分類的市场估算与预测,2022-2035年

- 车

- 建筑/施工

- 船

- 航太/国防

- 石油和天然气

- 其他(金属、采矿等)

第八章 按分销管道分類的市场估算与预测,2022-2035年

- 直销

- 间接

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

第十章:公司简介

- Ador Welding Ltd.

- Air Liquide Welding

- Arcon Welding Equipment

- Bohler Welding

- Denyo Co., Ltd.

- ESAB

- Fronius International GmbH

- Hyundai Welding Co., Ltd.

- Illinois Tool Works Inc.(ITW)

- Jasic Technology Co., Ltd.

- Kemppi Oy

- Lincoln Electric

- Miller Electric

- Panasonic Welding Systems

- Tianjin Golden Bridge Welding Materials Group

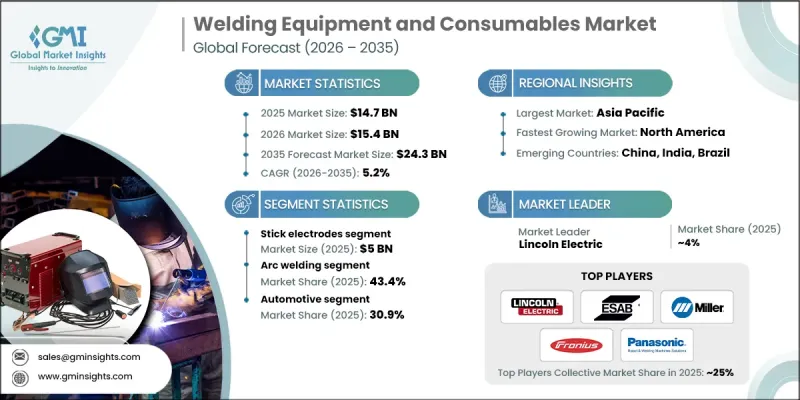

The Global Welding Equipment and Consumables Market was valued at USD 14.7 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 24.3 billion by 2035.

The industry's expansion is fueled by rapid urbanization and large-scale infrastructure developments that demand reliable and high-strength welding solutions. Modern infrastructure projects require advanced welding techniques to ensure durability and structural integrity across bridges, railways, highways, and industrial facilities. Beyond construction, the shift toward sustainable building practices has increased the need for innovative welding technologies that improve efficiency and minimize environmental impact. Investments from both public and private sectors in infrastructure are creating consistent growth opportunities. At the same time, the automotive and transportation industries are undergoing transformation due to the adoption of electric vehicles and lightweight materials, further driving demand for specialized welding equipment and consumables capable of handling new alloys and composites.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.7 Billion |

| Forecast Value | $24.3 Billion |

| CAGR | 5.2% |

The stick electrodes segment accounted for USD 5 billion in 2025 and is expected to grow at a CAGR of 4.6% through 2035. These electrodes remain popular due to their cost-effectiveness, versatility, and ability to perform reliably in outdoor and challenging conditions, making them indispensable for construction, repair, and maintenance applications. Their robust design allows welders to work efficiently in environments with wind, rain, or extreme temperatures, where other consumables might fail. Stick electrodes also offer compatibility with a wide range of metals and alloys, providing consistent weld quality across diverse projects.

The arc welding segment held a 43.4% share in 2025. Arc welding's adaptability and efficiency make it central to industries requiring high-quality welds, including automotive, construction, and heavy engineering. Techniques such as shielded metal arc welding (SMAW), gas metal arc welding (GMAW), and submerged arc welding (SAW) are widely employed to achieve durable and precise welds across various metals and alloys.

U.S. Welding Equipment and Consumables Market generated USD 2.7 billion in 2025 and is projected to grow at a CAGR of 5.7% from 2026 to 2035. The U.S. market benefits from a robust industrial base and a highly developed manufacturing sector, where widespread adoption of automated and robotic welding systems in automotive, aerospace, and energy industries is driving demand for high-precision equipment. The focus on meeting stringent safety and quality standards has accelerated investments in cutting-edge welding technologies and consumables to support advanced industrial processes.

Major players in the Global Welding Equipment and Consumables Market include Ador Welding Ltd., Air Liquide Welding, Arcon Welding Equipment, Bohler Welding, Denyo Co., Ltd., ESAB, Fronius International GmbH, Hyundai Welding Co., Ltd., Illinois Tool Works Inc. (ITW), Jasic Technology Co., Ltd., Kemppi Oy, Lincoln Electric, Miller Electric, Panasonic Welding Systems, and Tianjin Golden Bridge Welding Materials Group. Companies in the Global Welding Equipment and Consumables Market are pursuing multiple strategies to strengthen their market presence and expand their foothold. They are investing in research and development to introduce advanced, high-efficiency welding solutions tailored for industrial, construction, and automotive applications. Partnerships and collaborations with infrastructure and automotive companies allow them to offer integrated solutions and secure long-term contracts. Many are focusing on expanding their geographic reach, particularly in emerging markets where infrastructure growth is rapid. The adoption of automation, robotic welding systems, and smart welding technologies helps enhance operational efficiency for clients, increasing brand loyalty.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 Application

- 2.2.5 Distribution channels

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Infrastructure development and industrialization

- 3.2.1.2 Automotive and transportation sector expansion

- 3.2.1.3 Technological advancements in welding processes

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High initial investment and maintenance costs

- 3.2.2.2 Shortage of skilled workforce

- 3.2.3 Opportunities

- 3.2.3.1 Adoption of automation and industry 4.0

- 3.2.3.2 Growing demand in renewable energy sector

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.1.1 US: Consumer Product Safety Commission (CPSC) 16 Code of Federal Regulations (CFR) part 1512

- 3.7.1.2 Canada: International Organization for Standardization (ISO) 4210

- 3.7.2 Europe

- 3.7.2.1 Germany: Deutsches Institut fur Normung (DIN) European Norm (EN) ISO 4210

- 3.7.2.2 UK: European Norm (EN) ISO 4210 / United Kingdom Conformity Assessed (UKCA)

- 3.7.2.3 France: European Norm (EN) ISO 4210

- 3.7.3 Asia Pacific

- 3.7.3.1 China: Guobiao (GB) 3565

- 3.7.3.2 India: Indian Standard (IS) 10613

- 3.7.3.3 Japan: Japanese Industrial Standard (JIS) D 9110

- 3.7.4 Latin America

- 3.7.4.1 Brazil: Associacao Brasileira de Normas Tecnicas (ABNT) Norma Brasileira (NBR) ISO 4210

- 3.7.4.2 Mexico: International Organization for Standardization (ISO) 4210

- 3.7.5 Middle East & Africa

- 3.7.5.1 South Africa: South African National Standard (SANS) 311

- 3.7.5.2 Saudi Arabia: Saudi Standards, Metrology and Quality Organization (SASO) Gulf Standardization Organization (GSO) ISO 4210

- 3.7.1 North America

- 3.8 Trade statistics (HS Code - 8501)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter';s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Stick electrodes

- 5.3 Solid wires

- 5.4 Flux coiled wires

- 5.5 Saw wires

- 5.6 Others (rod electrodes, shielding gas, etc.)

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Arc welding

- 6.3 Resistance welding

- 6.4 Oxy-fuel welding

- 6.5 Solid state welding

- 6.6 Others (electron beam, etc.)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Building and construction

- 7.4 Marine

- 7.5 Aerospace & defense

- 7.6 Oil & gas

- 7.7 Others (metal, mining, etc.)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Ador Welding Ltd.

- 10.2 Air Liquide Welding

- 10.3 Arcon Welding Equipment

- 10.4 Bohler Welding

- 10.5 Denyo Co., Ltd.

- 10.6 ESAB

- 10.7 Fronius International GmbH

- 10.8 Hyundai Welding Co., Ltd.

- 10.9 Illinois Tool Works Inc. (ITW)

- 10.10 Jasic Technology Co., Ltd.

- 10.11 Kemppi Oy

- 10.12 Lincoln Electric

- 10.13 Miller Electric

- 10.14 Panasonic Welding Systems

- 10.15 Tianjin Golden Bridge Welding Materials Group

2026年全球焊接设备、配件及耗材市场报告2026年全球发动机驱动焊接机市场报告2026年全球等离子焊接市场报告2026年全球缝焊机市场报告

2026年全球焊接设备、配件及耗材市场报告2026年全球发动机驱动焊接机市场报告2026年全球等离子焊接市场报告2026年全球缝焊机市场报告 微型对接焊机市场材料类型、操作模式、焊接电流、电极类型、电源、应用和最终用户产业划分,全球预测,2026-2032年超音波电池焊接机市场(依电池类型、模式、终端用户产业和销售管道)——2026-2032年全球预测雷射视觉焊接追踪系统市场:依追踪模式、雷射类型、成像技术、系统类型和应用划分-全球预测,2026-2032年

微型对接焊机市场材料类型、操作模式、焊接电流、电极类型、电源、应用和最终用户产业划分,全球预测,2026-2032年超音波电池焊接机市场(依电池类型、模式、终端用户产业和销售管道)——2026-2032年全球预测雷射视觉焊接追踪系统市场:依追踪模式、雷射类型、成像技术、系统类型和应用划分-全球预测,2026-2032年 欧洲焊接设备市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)

欧洲焊接设备市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年) 堆焊市场-全球产业规模、份额、趋势、机会和预测,依焊接方法、基材、最终用户产业、地区和竞争格局划分,2021-2031年预测

堆焊市场-全球产业规模、份额、趋势、机会和预测,依焊接方法、基材、最终用户产业、地区和竞争格局划分,2021-2031年预测 焊接设备市场规模、份额及成长分析(按类型、技术、应用和地区划分)-2026-2033年产业预测

焊接设备市场规模、份额及成长分析(按类型、技术、应用和地区划分)-2026-2033年产业预测