|

市场调查报告书

商品编码

1928979

祛水器市场机会、成长要素、产业趋势分析及2026年至2035年预测Steam Trap Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

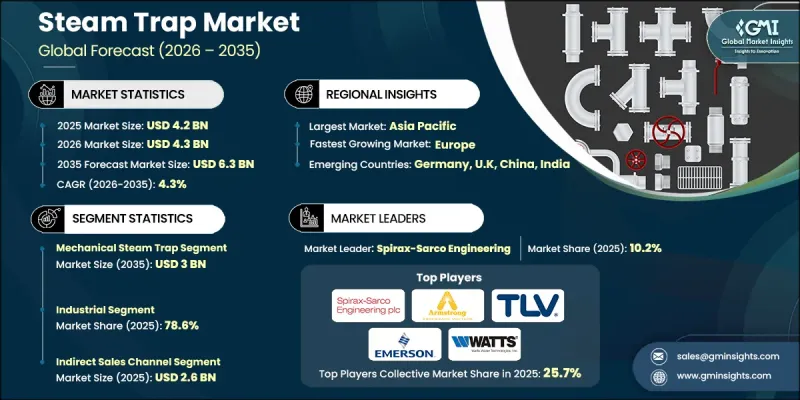

全球祛水器市场预计到 2025 年将达到 42 亿美元,到 2035 年将达到 63 亿美元,年复合成长率为 4.3%。

市场成长主要得益于节能技术的日益普及和工业蒸气系统自动化程度的提升。祛水器在维持最佳蒸气性能方面发挥关键作用,它能够防止蒸气网内的蒸气损失并高效排出冷凝水。提高系统效率可直接转化为减少能源浪费、降低营运成本和提高製程可靠性。对自动化监控和数据驱动型维护的日益重视正在变革时期蒸气系统的管理方式,使操作人员能够在最大限度地减少计划外停机时间的同时提高系统性能。监管压力和政策主导的节能措施不断加速以先进解决方案取代传统设备。提高蒸气系统效率可降低10-15%的总能耗,进而提升安装现代化蒸气疏水阀的经济价值。随着各行业将永续性、营运优化和排放置于优先地位,蒸气疏水阀仍然是各种工业环境中实现长期能源管理目标的关键组成部分。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 42亿美元 |

| 预测金额 | 63亿美元 |

| 复合年增长率 | 4.3% |

预计2025年,机械式祛水器的市场规模将达到19亿美元,到2035年将达到30亿美元。该细分市场凭藉其耐用性、运作可靠性和对严苛工业环境的适应性,保持着主导地位。这些疏水阀的设计旨在排放蒸气的同时高效排出冷凝水,从而确保系统稳定运作。祛水器运作不当会导致高达20%的总蒸气产量损失,凸显了正确选择和维护系统的重要性。

预计到2025年,工业应用将占据78.6%的市场。这一领域的成长得益于严格的能源效率法规、对即时系统监控日益增长的需求以及预测性维护方法的广泛应用。政府主导的永续性倡议也进一步推动了先进蒸气管理解决方案在工业设施中的应用。

预计到2025年,美国蒸气疏水阀市占率将达到79.4%。强劲的工业现代化进程、高自动化普及率以及严格的能源效率标准持续推动市场需求。减少能源损耗和排放的持续努力也促使企业继续投资先进的蒸气疏水阀技术。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 产业影响因素

- 司机

- 对工业自动化和流程效率的需求日益增长

- 扩大製造业节能解决方案的应用

- 政府有关排放减排的法规

- 产业潜在风险与挑战

- 较高的初始实施和维护成本

- 缺乏对蒸气疏水阀维护的认识与专业知识

- 机会

- 扩展智慧和物联网赋能的祛水器解决方案

- 工业发展和节能法规导致需求增加

- 司机

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按类型

- 按地区

- 监管环境

- 标准和合规要求

- 区域法规结构

- 认证标准

- 贸易统计

- 主要进口国

- 主要出口国

- 差距分析

- 风险评估与缓解

- 波特分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 按类型分類的市场估算与预测,2022-2035年

- 机械式蒸气疏水阀

- 动态蒸气带

- 恆温蒸气疏水阀

第六章 依功能分類的市场估计与预测,2022-2035年

- 蒸气管道

- 冷凝油油回收

第七章 按材料分類的市场估算与预测,2022-2035年

- 铸铁/球墨铸铁

- 碳钢

- 不銹钢

- 合金/特殊钢

第八章 市场估计与预测:依性别划分,2022-2035年

- 传统的

- 智慧诱捕器/监测诱捕器

第九章 按应用领域分類的市场估算与预测,2022-2035年

- 住宅

- 商业的

- 工业的

第十章 依最终用途分類的市场估计与预测,2022-2035年

- 流程工业

- 发电

- 暖通空调和区域供暖

- 製药和医疗保健

- 其他的

第十一章 按分销管道分類的市场估算与预测,2022-2035年

- 直销

- 间接

第十二章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十三章:公司简介

- ARI-Armaturen

- Armstrong International

- Ayvaz

- Emerson Electric

- Forbes Marshall

- Hoffman Specialty

- Miura

- Miyawaki

- Spirax-Sarco Engineering

- Thermax

- TLV International

- Velan

- Watson-McDaniel

- Watts Water Technologies

- Yoshitake

The Global Steam Trap Market was valued at USD 4.2 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 6.3 billion by 2035.

Market expansion is driven by rising adoption of energy-efficient technologies and increased automation across industrial steam systems. Steam traps play a critical role in maintaining optimal steam performance by efficiently removing condensate while preventing steam loss within distribution networks. Improved system efficiency directly supports reduced energy waste, lower operating costs, and enhanced process reliability. Growing emphasis on automated monitoring and data-driven maintenance is reshaping how steam systems are managed, allowing operators to improve performance while minimizing unexpected downtime. Regulatory pressure and policy-driven energy conservation initiatives continue to accelerate the replacement of outdated equipment with advanced solutions. Efficiency improvements in steam systems can reduce overall energy consumption by 10% to 15%, reinforcing the economic value of modern steam trap deployment. As industries prioritize sustainability, operational optimization, and emissions reduction, steam traps remain essential components in achieving long-term energy management goals across a wide range of industrial environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.2 Billion |

| Forecast Value | $6.3 Billion |

| CAGR | 4.3% |

The mechanical steam traps generated USD 1.9 billion in 2025 and are projected to reach USD 3 billion by 2035. This segment maintains leadership due to its durability, operational reliability, and suitability for demanding industrial conditions. These traps are designed to discharge condensate efficiently while retaining steam, supporting consistent system performance. Inefficient steam trap operation can result in losses of up to 20% of total steam generation, highlighting the importance of proper system selection and maintenance.

The industrial applications accounted for 78.6% share in 2025. Growth in this segment is supported by stricter energy-efficiency regulations, increasing demand for real-time system monitoring, and wider adoption of predictive maintenance practices. Government-led sustainability initiatives further encourage the deployment of advanced steam management solutions across industrial facilities.

United States Steam Trap Market held 79.4% share in 2025. Strong industrial modernization efforts, high automation adoption, and rigorous efficiency standards continue to drive demand. Ongoing focus on reducing energy losses and emissions supports continued investment in advanced steam trap technologies.

Key companies operating in the Global Steam Trap Market include Armstrong International, Spirax-Sarco Engineering, Emerson Electric, Forbes Marshall, TLV International, ARI-Armaturen, Thermax, Ayvaz, Miura, Velan, Watson-McDaniel, Watts Water Technologies, Yoshitake, Miyawaki, and Hoffman Specialty. Companies active in the Steam Trap Market strengthen their competitive position through product innovation, digital integration, and service-oriented strategies. Investment in intelligent monitoring capabilities and predictive maintenance solutions enhances system reliability and customer value. Manufacturers focus on improving durability, efficiency, and ease of integration with automated control systems. Strategic partnerships with industrial operators and energy service providers support long-term adoption and recurring revenue. Geographic expansion into emerging industrial regions broadens market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Function

- 2.2.4 Material

- 2.2.5 Connectivity

- 2.2.6 Application

- 2.2.7 End use

- 2.2.8 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased industrial automation and process efficiency demands

- 3.2.1.2 Rising adoption of energy-efficient solutions in manufacturing

- 3.2.1.3 Government regulations on energy conservation and emissions reduction

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial installation and maintenance costs

- 3.2.2.2 Limited awareness and expertise in steam trap maintenance

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of smart & IoT-enabled steam trap solutions

- 3.2.3.2 Rising demand driven by industrial growth & energy-efficiency regulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By type

- 3.6.2 By region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Gap analysis

- 3.10 Risk assessment and mitigation

- 3.11 Porter';s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Mechanical steam trap

- 5.3 Thermodynamic steam strap

- 5.4 Thermostatic steam trap

Chapter 6 Market Estimates & Forecast, By Function, 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Steam distribution

- 6.3 Condensate recovery

Chapter 7 Market Estimates & Forecast, By Material, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Cast/ductile iron

- 7.3 Carbon steel

- 7.4 Stainless steel

- 7.5 Alloy/specialty

Chapter 8 Market Estimates & Forecast, By Connectivity, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Conventional

- 8.3 Smart/monitored traps

Chapter 9 Market Estimates & Forecast, By Application, 2022-2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial

Chapter 10 Market Estimates & Forecast, By End Use, 2022-2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Process industry

- 10.3 Power generation

- 10.4 HVAC & district heating

- 10.5 Pharmaceuticals & healthcare

- 10.6 Others

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Direct

- 11.3 Indirect

Chapter 12 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 France

- 12.3.3 UK

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 ARI-Armaturen

- 13.2 Armstrong International

- 13.3 Ayvaz

- 13.4 Emerson Electric

- 13.5 Forbes Marshall

- 13.6 Hoffman Specialty

- 13.7 Miura

- 13.8 Miyawaki

- 13.9 Spirax-Sarco Engineering

- 13.10 Thermax

- 13.11 TLV International

- 13.12 Velan

- 13.13 Watson-McDaniel

- 13.14 Watts Water Technologies

- 13.15 Yoshitake

2026年全球祛水器市场报告2026年全球祛水器监测市场报告

2026年全球祛水器市场报告2026年全球祛水器监测市场报告 蒸气疏水阀市场规模、份额和成长分析(按类型、功能、材质、连接类型、应用、最终用途、通路和地区划分)—2026-2033年产业预测

蒸气疏水阀市场规模、份额和成长分析(按类型、功能、材质、连接类型、应用、最终用途、通路和地区划分)—2026-2033年产业预测 蒸气疏水阀市场 - 全球产业规模、份额、趋势、机会及预测(按产品、应用、材质、产业、地区及竞争格局划分),2021-2031年

蒸气疏水阀市场 - 全球产业规模、份额、趋势、机会及预测(按产品、应用、材质、产业、地区及竞争格局划分),2021-2031年 祛水器市场-2025-2030年预测

祛水器市场-2025-2030年预测 祛水器市场(按技术类型、材料、连接、最终用途行业、分销管道和应用)—2025-2030 年全球预测

祛水器市场(按技术类型、材料、连接、最终用途行业、分销管道和应用)—2025-2030 年全球预测 全球祛水器市场 2025-2029

全球祛水器市场 2025-2029 全球祛水器市场:按产品类型、按连接、按阀体材质、按压力、按尺寸、按应用、按最终用途行业、按地区 - 预测到 2029 年

全球祛水器市场:按产品类型、按连接、按阀体材质、按压力、按尺寸、按应用、按最终用途行业、按地区 - 预测到 2029 年 全球蒸汽消音器市场(2024-2028)

全球蒸汽消音器市场(2024-2028) 祛水器市场规模、份额、趋势分析报告:按产品、最终用途、按地区、细分市场预测,2024-2030 年

祛水器市场规模、份额、趋势分析报告:按产品、最终用途、按地区、细分市场预测,2024-2030 年