|

市场调查报告书

商品编码

1936489

工业能源储存系统市场机会、成长要素、产业趋势分析及2026年至2035年预测Industrial Energy Storage System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

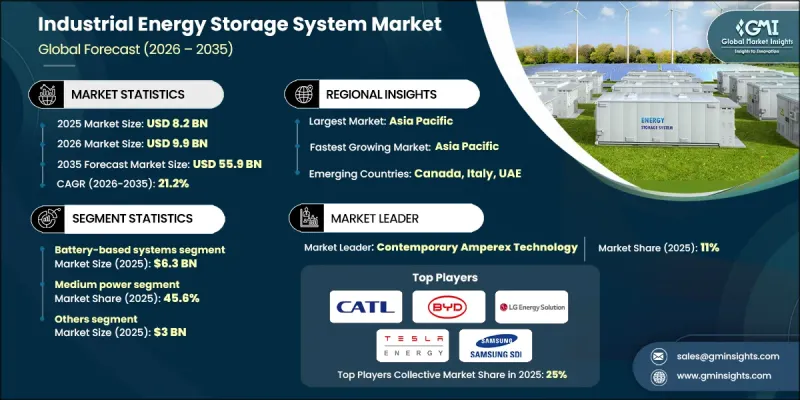

全球工业能源储存系统市场预计到 2025 年将达到 82 亿美元,到 2035 年将达到 559 亿美元,年复合成长率为 21.2%。

市场成长受到工业企业日益增长的压力,这些企业需要与全球气候目标和内部永续性措施保持一致。世界各国政府都在收紧排放法规,而随着碳定价机制和排放交易计画的日益普及,长期依赖石化燃料的成本也不断上升。随着工业活动转型为电气化并更依赖可再生能源,能源储存系统对于维持营运连续性和应对电力供应波动变得至关重要。工业储能正日益被视为实现脱碳目标、增强能源安全和提高低碳经济韧性的战略基础。随着电力基础设施、可再生能源发电和储能解决方案的普及,工业能源储存系统係统正日益被视为长期资产,而非辅助设备。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 82亿美元 |

| 预测金额 | 559亿美元 |

| 复合年增长率 | 21.2% |

除了监管合规之外,干净科技成本的下降也促使企业加快对永续能源解决方案的投资。工业企业采用能源储存系统不仅是为了实现其环境目标,也是为了提升财务绩效。这些系统被广泛认为是能够帮助稳定能源消耗、提高营运成本可预测性并降低整体能源相关成本的有效工具。因此,工业储能的商业价值在众多工业应用领域中持续增强。

预计2025年,电池技术市场规模将达到63亿美元。这一主导地位反映了工业环境中对电池的依赖性日益增强,以平衡能源需求和生产要求。这些系统旨在储存低需求时期或再生能源来源产生的多余电力,并在需求增加时释放。这种能力使企业能够提高效率和柔软性,同时在高成本时期减少对电网的依赖。电池解决方案还具有扩充性的架构,使其能够部署在各种规模的设施中,同时支援稳定的效能和运作管理。

到2025年,中功率储能係统将占据45.6%的市场份额,成为最大的功率细分市场。这类系统尤其适用于需要在容量和基础设施投资之间取得平衡的工业环境。中功率储能解决方案能够提供足够的电力来应对尖峰时段能源需求、支援可再生能源併网并提高运作可靠性,同时避免了高容量储能係统带来的复杂性和高成本。这种平衡使得该细分市场对众多寻求可靠高效储能解决方案的工业用户极具吸引力。

预计2025年,美国工业能源储存系统市场规模将达到21亿美元,占79.7%的市占率。推动美国市场扩张的主要因素包括:强劲的脱碳倡议、现场可再生能源的日益普及以及应对电力成本波动的需求。工业营运商正在加速采用能源储存系统,以提高电力品质、控制能源成本并增强业务永续营运。社区能源系统的蓬勃发展也有助于提高系统韧性,同时降低停电风险。随着法规结构的不断完善,工业参与者正获得新的市场机制,进而提升储能资产的经济价值。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 产业影响因素

- 司机

- 工业脱碳和净零排放目标

- 可再生能源併网

- 数位化和智慧型能源管理

- 产业潜在风险与挑战

- 高昂的初始投资成本

- 技术风险和性能不确定性

- 机会

- 长期储能解决方案

- 数位平台和人工智慧优化

- 司机

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 透过储存系统

- 监管环境

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

5. 2022-2035年按储存系统分類的市场估算与预测

- 机械系统

- 压缩空气储能

- 抽水蓄能水力发电

- 热力系统

- 电池储能係统

第六章 依产量范围分類的市场估计与预测,2022-2035年

- 低功率(超过 200kW)

- 中功率(200千瓦至5兆瓦)

- 高功率(小于5兆瓦)

第七章 按应用领域分類的市场估算与预测,2022-2035年

- 能源套利和时间转移

- 尖峰用电调节和负载平衡

- 可再生能源併网与稳定

- 电网稳定和电压支撑

- 电力传输和分配的延误

8. 2022-2035年按最终用途产业分類的市场估算与预测

- 矿业

- 石油和天然气

- 食品/饮料

- 製药

- 车

- 其他(资料中心等)

第九章 按分销管道分類的市场估算与预测,2022-2035年

- 直销

- 间接销售

第十章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章 公司简介

- Atlas Copco

- BYD

- Caterpillar

- Contemporary Amperex Technology

- Cummins

- ESS

- Fluence Energy

- LG Energy Solution

- Northvolt

- Powin Energy

- Samsung SDI

- Sumitomo Electric Industries

- Tesla Energy

- Wartsila Energy

The Global Industrial Energy Storage System Market was valued at USD 8.2 billion in 2025 and is estimated to grow at a CAGR of 21.2% to reach USD 55.9 billion by 2035.

Market growth is strongly influenced by mounting pressure on industrial organizations to align with global climate objectives and internal sustainability commitments. Governments worldwide are implementing stricter emissions regulations, while the long-term cost of fossil fuel dependence continues to rise as carbon pricing mechanisms and emissions trading programs gain traction. As industrial operations shift toward electrified processes and greater reliance on renewable energy, energy storage systems are becoming essential to maintain operational continuity and manage fluctuations in power supply. Industrial energy storage is increasingly viewed as a strategic enabler that supports decarbonization goals, strengthens energy security, and improves resilience in a low-carbon economy. The broader adoption of electric infrastructure, renewable power generation, and storage solutions is reinforcing the role of industrial energy storage systems as long-term assets rather than auxiliary equipment.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.2 Billion |

| Forecast Value | $55.9 Billion |

| CAGR | 21.2% |

Beyond regulatory compliance, declining costs of clean technologies are encouraging companies to accelerate investments in sustainable energy solutions. Industrial enterprises are adopting energy storage systems not only to support environmental targets but also to improve financial performance. These systems are widely recognized as tools that help stabilize energy consumption, improve predictability of operating expenses, and reduce overall energy-related costs. As a result, the business case for industrial energy storage continues to strengthen across a wide range of industrial applications.

The battery-based technologies segment generated USD 6.3 billion in 2025. Their leadership position reflects the growing reliance on batteries to balance energy demand with production requirements in industrial settings. These systems are designed to store excess electricity generated during low-demand periods or from renewable sources and release it when demand rises. This capability allows organizations to reduce dependence on grid electricity during high-cost periods while improving efficiency and flexibility. Battery-based solutions also benefit from scalable architectures, enabling deployment across facilities of varying sizes while supporting consistent performance and operational control.

The medium power category accounted for 45.6% share in 2025, making it the largest power segment. Systems within this range are particularly well-suited for industrial environments that require a balance between capacity and infrastructure investment. Medium power energy storage solutions offer sufficient output to manage peak energy requirements, support renewable integration, and enhance operational reliability without the complexity or cost associated with higher-capacity installations. This balance has made the segment highly attractive to a broad range of industrial users seeking dependable and efficient storage solutions.

United States Industrial Energy Storage System Market held 79.7% share in 2025, generating USD 2.1 billion. Market expansion in the country is driven by strong decarbonization initiatives, rising adoption of onsite renewable energy, and the need to address fluctuating electricity costs. Industrial operators are increasingly deploying energy storage systems to improve power quality, manage energy expenses, and strengthen operational continuity. The growing development of localized energy systems is also enhancing resilience while reducing exposure to power interruptions. As regulatory frameworks evolve, industrial participants are gaining access to new market mechanisms that enhance the economic value of energy storage assets.

Key companies active in the Global Industrial Energy Storage System Market include LG Energy Solution, Tesla Energy, Wartsila Energy, BYD, Fluence Energy, Caterpillar, Samsung SDI, Cummins, Northvolt, Atlas Copco, Contemporary Amperex Technology, ESS, Powin Energy, and Sumitomo Electric Industries. Companies operating in the industrial energy storage system market are strengthening their market position through a combination of technology innovation, strategic partnerships, and geographic expansion. Manufacturers are prioritizing investments in advanced battery chemistries, system efficiency improvements, and digital energy management capabilities to enhance performance and reliability. Many players are expanding their solution portfolios to address diverse industrial requirements while offering modular designs that support scalable deployment.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Storage systems

- 2.2.3 Power range

- 2.2.4 Application

- 2.2.5 End use industry

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Industrial decarbonization & net-zero targets

- 3.2.1.2 Renewable energy integration

- 3.2.1.3 Digitalization & smart energy management

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High upfront capex

- 3.2.2.2 Technology risk & performance uncertainty

- 3.2.3 Opportunities

- 3.2.3.1 Long-duration storage solutions

- 3.2.3.2 Digital platforms & AI optimization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By storage systems

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Storage system, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Mechanical systems

- 5.3 Compressed air energy storage

- 5.4 Pumped hydro power

- 5.5 Thermal systems

- 5.6 Battery-based systems

Chapter 6 Market Estimates and Forecast, By Power Range, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low power (>200kW)

- 6.3 Medium power (200kW-5MW)

- 6.4 High power (<5 MW)

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Energy arbitrage & time-shifting

- 7.3 Peak shaving & load leveling

- 7.4 Renewable integration & firming

- 7.5 Grid stability & voltage support

- 7.6 Transmission & distribution deferral

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Mining

- 8.3 Oil & gas

- 8.4 Food & beverage

- 8.5 Pharmaceutical

- 8.6 Automotive

- 8.7 Others (data center etc.)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Atlas Copco

- 11.2 BYD

- 11.3 Caterpillar

- 11.4 Contemporary Amperex Technology

- 11.5 Cummins

- 11.6 ESS

- 11.7 Fluence Energy

- 11.8 LG Energy Solution

- 11.9 Northvolt

- 11.10 Powin Energy

- 11.11 Samsung SDI

- 11.12 Sumitomo Electric Industries

- 11.13 Tesla Energy

- 11.14 Wartsila Energy

2026年全球能源储存系统市场报告

2026年全球能源储存系统市场报告 全球牵引能源储存系统市场(按电池化学成分、车辆类型、电芯类型、电压范围、应用和最终用户划分)预测(2026-2032年)微型太阳能能源储存系统市场(按电池类型、容量范围、最终用途和应用划分),全球预测(2026-2032)

全球牵引能源储存系统市场(按电池化学成分、车辆类型、电芯类型、电压范围、应用和最终用户划分)预测(2026-2032年)微型太阳能能源储存系统市场(按电池类型、容量范围、最终用途和应用划分),全球预测(2026-2032) 能源储存系统市场规模、份额及成长分析(按技术、应用、最终用途、容量和地区划分)-2026-2033年产业预测

能源储存系统市场规模、份额及成长分析(按技术、应用、最终用途、容量和地区划分)-2026-2033年产业预测 日本储能係统市场报告(按技术、应用、最终用户和地区划分,2026-2034年)

日本储能係统市场报告(按技术、应用、最终用户和地区划分,2026-2034年) 户外液冷能源储存系统:全球市占率及排名、总销售量及需求预测(2025-2031年)能源储存系统(ESS)-全球市场份额和排名、总收入和需求预测(2025-2031年)

户外液冷能源储存系统:全球市占率及排名、总销售量及需求预测(2025-2031年)能源储存系统(ESS)-全球市场份额和排名、总收入和需求预测(2025-2031年) 全球智慧能源储存系统係统市场全球电子机械能源储存系统係统市场全球电化学能源储存系统係统市场

全球智慧能源储存系统係统市场全球电子机械能源储存系统係统市场全球电化学能源储存系统係统市场