|

市场调查报告书

商品编码

1936502

医用氧气浓缩机市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Medical Oxygen Concentrators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

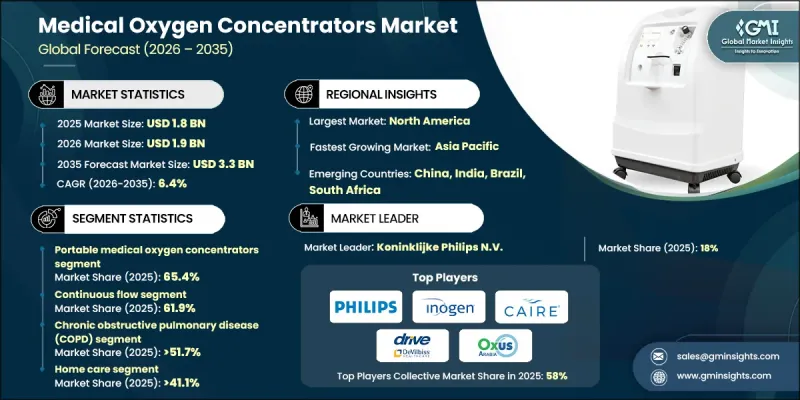

全球医用氧气浓缩机市场预计到 2025 年将达到 18 亿美元,到 2035 年将达到 33 亿美元,年复合成长率为 6.4%。

慢性呼吸系统疾病发生率上升、空气污染加剧以及全球老年人口比例增加是推动氧气浓缩器市场成长的主要因素。氧气浓缩机在为慢性呼吸系统疾病导致呼吸困难的患者提供长期氧气疗法发挥关键作用。这些设备透过过滤环境空气产生氧气,并将高浓度氧气直接输送给患者,无需笨重的储氧罐。医疗系统正越来越多地采用氧气浓缩器,将其作为一种经济高效、可靠且扩充性的呼吸解决方案。此外,居家医疗的明显转变也推动了市场成长,这得益于公共卫生措施、医疗设备取得途径的改善以及病患对舒适照护的偏好。设备效率、噪音降低和能源效率的提升也促进了氧气浓缩器的普及。人们对早期呼吸介入和长期疾病管理重要性的认识不断提高,也增强了医院、诊所和居家照护机构对氧气浓缩器的需求。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 18亿美元 |

| 预测金额 | 33亿美元 |

| 复合年增长率 | 6.4% |

截至2025年,携带式医用氧气浓缩机市占率达到65.4%。这些系统凭藉其紧凑轻巧的设计,为使用者提供行动性、便利性和持续供氧功能。患者越来越倾向于选择携带式解决方案,以便保持独立性,并在日常生活和旅行中不间断地接受治疗。更智慧的供氧系统、更长的电池续航时间和数位化连接等技术的不断进步,持续推动着这个细分市场的扩张。

预计到2025年,连续流氧气供应设备将占据61.9%的市场。连续流氧气供应设备能够提供稳定的氧气,因此对于需要在休息或睡眠期间持续接受治疗的患者来说至关重要。其可靠性和满足高氧气需求的能力使其在临床和居家医疗环境中广泛应用。

预计到2025年,美国医用氧气浓缩机市场规模将达到6.352亿美元。推动市场成长的因素包括:强大的医疗基础设施、广泛的保险覆盖范围以及居家医疗解决方案的日益普及。与数位健康平台和远端监控系统的整合,进一步加速了医用氧气浓缩器在各种医疗环境中的应用。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 影响价值链的因素

- 产业影响因素

- 成长驱动因素

- 全球老年人口基数不断成长

- 慢性阻塞性肺病全球盛行率不断上升

- 提高人们对居家医疗解决方案的认识

- 氧气浓缩机创新

- 产业潜在风险与挑战

- 严格的监管环境

- 设备高成本

- 市场机会

- 与数位化居家医疗生态系统的整合

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 科技趋势

- 当前技术趋势

- 新兴技术

- 未来市场趋势

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 世界

- 北美洲

- 欧洲

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 2022-2035年按产品分類的市场估算与预测

- 携带式医用氧气浓缩机

- 固定式医用氧气浓缩机

第六章 按技术分類的市场估计与预测,2022-2035年

- 连续流

- 脉衝流

第七章 按应用领域分類的市场估算与预测,2022-2035年

- 慢性阻塞性肺病(COPD)

- 气喘

- 呼吸窘迫症候群

- 其他用途

第八章 依最终用途分類的市场估算与预测,2022-2035年

- 医院

- 诊所

- 居家医疗

- 其他最终用户

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- BESCO Medical

- BPL Medical Technologies

- CAIRE

- Daikin Industries

- Drive DeVilbiss Healthcare

- ESAB Corporation

- Foshan Keyhub Electronic Industries

- Inogen

- Jiangsu Yuyue Medical Equipment &Supply(Yuwell)

- Koninklijke Philips NV

- O2 Concepts

- OXUS

- Precision Medical

- React Health

- Teijin Limited

The Global Medical Oxygen Concentrators Market was valued at USD 1.8 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 3.3 billion by 2035.

Growth is driven by the rising incidence of chronic respiratory disorders, increasing air pollution exposure, and the growing proportion of elderly populations worldwide. Oxygen concentrators play a vital role in delivering long-term oxygen therapy for patients facing breathing difficulties caused by chronic respiratory conditions. These devices generate oxygen by filtering ambient air and supplying concentrated oxygen directly to patients, eliminating the need for bulky storage cylinders. Healthcare systems increasingly adopt oxygen concentrators as cost-effective, reliable, and scalable respiratory solutions. The market also benefits from a clear shift toward home-based healthcare, supported by public health initiatives, improved access to medical devices, and patient preference for comfort-driven care. Advances in device efficiency, noise reduction, and energy performance further enhance adoption. Growing awareness of early respiratory intervention and long-term disease management strengthens demand across hospitals, clinics, and home care environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 6.4% |

The portable medical oxygen concentrators segment held 65.4% share in 2025. These systems provide mobility, convenience, and continuous oxygen support in compact and lightweight designs. Patients increasingly prefer portable solutions that allow independence and uninterrupted therapy during daily activities or travel. Ongoing technological improvements, including smarter oxygen delivery systems, extended battery performance, and digital connectivity, continue to drive segment expansion.

The continuous flow segment held a 61.9% share in 2025. Continuous flow devices deliver a constant oxygen supply, making them essential for patients requiring stable therapy during rest or sleep. Their reliability and ability to support higher oxygen needs make them widely used in both clinical and homecare settings.

United States Medical Oxygen Concentrators Market reached USD 635.2 million in 2025. Strong healthcare infrastructure, broad insurance coverage, and rising adoption of home healthcare solutions support market leadership. Integration with digital health platforms and remote monitoring systems further accelerates usage across care settings.

Key companies operating in the Global Medical Oxygen Concentrators Market include Koninklijke Philips N.V., Inogen, CAIRE, Drive DeVilbiss Healthcare, Teijin Limited, React Health, Precision Medical, O2 Concepts, Daikin Industries, Jiangsu Yuyue Medical Equipment & Supply, BPL Medical Technologies, BESCO Medical, Foshan Keyhub Electronic Industries, ESAB Corporation, and OXUS. Companies in the medical oxygen concentrators market strengthen their market position by focusing on product innovation, portability, and energy efficiency. Manufacturers invest in lightweight designs, quieter operation, and longer battery life to enhance patient comfort and usability. Expansion into homecare and telehealth-integrated solutions supports wider adoption. Strategic partnerships with healthcare providers and distributors improve market access and service reach. Regulatory compliance, quality certifications, and patient safety remain core priorities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Technology trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Globally increasing elderly population base

- 3.2.1.2 Rising COPD prevalence worldwide

- 3.2.1.3 Increasing awareness of home healthcare solutions

- 3.2.1.4 Technological innovations in oxygen concentrators

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory landscape

- 3.2.2.2 High cost of the device

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with digital home care ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Portable medical oxygen concentrators

- 5.3 Stationary medical oxygen concentrators

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Continuous flow

- 6.3 Pulse flow

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Chronic obstructive pulmonary disease (COPD)

- 7.3 Asthma

- 7.4 Respiratory distress syndrome

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Clinics

- 8.4 Home care

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 BESCO Medical

- 10.2 BPL Medical Technologies

- 10.3 CAIRE

- 10.4 Daikin Industries

- 10.5 Drive DeVilbiss Healthcare

- 10.6 ESAB Corporation

- 10.7 Foshan Keyhub Electronic Industries

- 10.8 Inogen

- 10.9 Jiangsu Yuyue Medical Equipment & Supply (Yuwell)

- 10.10 Koninklijke Philips N.V.

- 10.11 O2 Concepts

- 10.12 OXUS

- 10.13 Precision Medical

- 10.14 React Health

- 10.15 Teijin Limited

氧气浓缩机市场:按电源、类型、输送方式、流量、应用、最终用户和分销管道划分-2026-2032年全球市场预测VOC转子浓缩器市场按过滤类型、滤材、技术、空气流量、容尘量、应用、终端用户产业和分销管道划分,全球预测,2026-2032年

氧气浓缩机市场:按电源、类型、输送方式、流量、应用、最终用户和分销管道划分-2026-2032年全球市场预测VOC转子浓缩器市场按过滤类型、滤材、技术、空气流量、容尘量、应用、终端用户产业和分销管道划分,全球预测,2026-2032年 固定式氧气浓缩机市场规模、份额和成长分析:按产品类型、电源、便携性、最终用户和地区划分 - 2026-2033 年产业预测

固定式氧气浓缩机市场规模、份额和成长分析:按产品类型、电源、便携性、最终用户和地区划分 - 2026-2033 年产业预测 2026年全球氧气浓缩机市场报告

2026年全球氧气浓缩机市场报告 全球医用氧气浓缩机市场规模、份额、趋势和成长分析报告(2026-2034年)

全球医用氧气浓缩机市场规模、份额、趋势和成长分析报告(2026-2034年) 日本氧气浓缩机市场规模、份额、趋势和预测:按类型、技术、应用、最终用户和地区划分,2026-2034年

日本氧气浓缩机市场规模、份额、趋势和预测:按类型、技术、应用、最终用户和地区划分,2026-2034年 氧气浓缩机市场规模、份额和成长分析(按类型、技术、应用、最终用户和地区划分)—产业预测(2026-2033 年)

氧气浓缩机市场规模、份额和成长分析(按类型、技术、应用、最终用户和地区划分)—产业预测(2026-2033 年) 医用氧气浓缩机和氧气瓶市场规模、份额和成长分析(按模式、技术、最终用户和地区划分)—2026-2033年产业预测

医用氧气浓缩机和氧气瓶市场规模、份额和成长分析(按模式、技术、最终用户和地区划分)—2026-2033年产业预测 全球氧气浓缩机市场:市场规模、份额、趋势分析(按产品、应用、技术和地区划分)、细分市场预测(2025-2033 年)北美氧气浓缩机市场:市场规模、份额、趋势分析(按产品、应用、技术和国家划分)、细分市场预测(2025-2033 年)

全球氧气浓缩机市场:市场规模、份额、趋势分析(按产品、应用、技术和地区划分)、细分市场预测(2025-2033 年)北美氧气浓缩机市场:市场规模、份额、趋势分析(按产品、应用、技术和国家划分)、细分市场预测(2025-2033 年)