|

市场调查报告书

商品编码

1936510

SDV即服务平台市场机会、成长要素、产业趋势分析及预测(2026-2035年)SDV-as-a-Service (SDVaaS) Platform Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

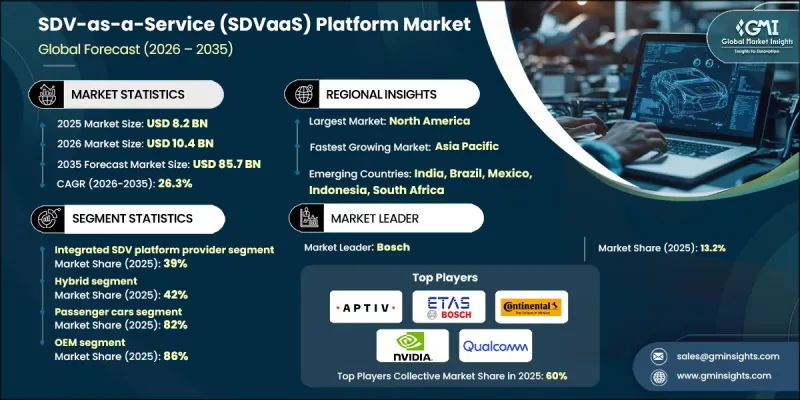

全球 SDV 即服务平台市场预计到 2025 年将达到 82 亿美元,到 2035 年将达到 857 亿美元,年复合成长率为 26.3%。

市场成长与消费者对类似智慧型手机的车载体验、频繁的软体升级以及高度个人化的出行功能的需求日益增长直接相关。汽车製造商正积极响应这一趋势,采用支援空中下载 (OTA)、数位化功能启用和订阅服务的云端平台,使车辆即使在售后也能持续发展。车辆正日益成为软体定义产品而非静态机器,从而在整个所有权生命週期中实现持续价值创造。这种转变正在重塑收入模式,增强客户参与,并拓展售后商机。原始设备製造商 (OEM) 利用软体定义车辆即服务 (SDVaaS) 平台建立可扩展的数位生态系统,即时连接车辆、驾驶员和云端服务。随着消费者对无缝连接和智慧功能的期望不断提高,SDVaaS 已成为全球乘用车和商用车领域下一代车辆策略的基础要素。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 82亿美元 |

| 预测金额 | 857亿美元 |

| 复合年增长率 | 26.3% |

汽车製造商正积极从分散式ECU架构向由区域电子电气架构支援的集中式运算转型。这种架构转变为SDVaaS经营模式奠定了必要的技术基础,同时简化了车辆布线,提高了系统效率,并实现了跨多个平台的统一服务交付。集中式和区域式设计支援软体重用、新功能的快速部署以及跨不同车型系列的轻鬆扩充性。 OEM厂商正日益与云端服务供应商、人工智慧开发人员和科技公司合作,加速SDV平台的成熟。这些伙伴关係提供了高级分析、高效能运算和安全的云端接口,从而缩短了开发週期,并实现了远端产品开发、部署、维护和生命週期管理。 SDVaaS平台使汽车製造商能够提供更丰富的数位体验,并在整个车辆生命週期中保持与客户的持续互动。

预计到2025年,整合式软体定义车辆(SDV)平台将占据39%的市场份额,并在2026年至2035年间以27%的复合年增长率成长。这些供应商之所以占据主导地位,是因为它们提供全面的端到端解决方案,将车辆云端基础设施、作业系统和应用层整合到一个统一的平台中。这种整合支援大规模的空中升级,并可在多种车型和产品系列中实现动态服务部署。透过提供完整的生态系统而非孤立的工具,整合供应商简化了原始设备製造商(OEM)的采用流程,加速了向完全软体定义车辆的转型,同时确保了全球车队的一致性、安全性和可扩展性。

预计到2025年,混合部署模式将占据42%的市场份额,并在2035年之前以27.3%的复合年增长率成长。混合SDVaaS部署将本地基础设施与私有云和公共云端环境相结合,为企业提供更大的营运柔软性和成本控制。汽车製造商可以在本地管理敏感工作负载,同时利用云端的可扩展性进行资料处理、分析和功能扩展。这种方法能够在满足监管、性能和安全要求的同时,实现精准的成本优化。混合部署支援分阶段的SDV推广,使OEM厂商能够在日益复杂的车辆软体环境中,平衡创新速度和基础设施稳定性。

美国智慧网联汽车即服务(SDV-as-a-Service)平台市场预计到2025年将达到26.2亿美元。美国在智慧网联汽车应用领域保持主导地位,这得益于主要汽车製造商和科技公司之间的密切合作,尤其是在创新中心,这些中心致力于推动联网汽车基础设施、空中下载(OTA)功能、车联网(V2X)通讯和自动驾驶系统的发展。联邦政府的支持进一步巩固了这一优势,相关政策鼓励自动驾驶汽车测试和互联出行计画。这些措施刺激了研发投资,并推动了先进智慧网联汽车技术在高速公路、智慧走廊和城市环境中的试点测试,使美国成为全球智慧网联汽车创新和应用中心。

目录

第一章调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 消费者对个人化的需求

- 集中式电子电气架构的采用现状

- 拓展OEM技术伙伴关係

- 监管主导的安全OTA

- 产业潜在风险与挑战

- 网路安全和隐私风险

- 分散的跨品牌标准

- 市场机会

- 订阅平台收入

- 与原始设备製造商和云端平台建立策略合作伙伴关係

- 第三方开发者生态系统

- 数据驱动的出行服务

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 美国运输部(DOT) 标准

- 职业安全与健康管理局 (OSHA) 指南

- 美国环保署(EPA)

- 欧洲

- EN ISO 容器标准

- 欧盟海关和安全法规

- BS EN/CEN 标准

- 国家标准(UNE、DIN等)

- 亚太地区

- 中国国家标准(GB标准)

- 日本JIS标准要求

- 韩国KS认证

- 印度BIS标准

- 泰国工业标准协会(TISI)

- 拉丁美洲

- INMETRO(国家计量研究院)

- INTI认证(国家技术研究院)

- NOM 标准(墨西哥官方标准)

- 中东和非洲

- ESMA/阿联酋合格评定计划 (ECAS)

- 海湾合作委员会技术法规

- SABS认证

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 成本細項分析

- 供应商成本结构

- 引入成本构成

- 持续营运成本

- 间接客户成本

- 专利分析

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 用例

- 经营模式模式和获利模式

- SDVaaS经营模式整体情况

- 平台许可订阅模式

- 按使用量付费和计量收费模式

- 开发即服务 (DaaS) 模型

- 收益分成和伙伴关係模式

- 买方决策标准与采购行为

- 买方环境概览

- 决策流程分析

- 关键评价标准

- 供应商选择和招标流程

- 谈判动态

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 2022-2035年各平台市场估算与预测

- 整合SDV平台提供者

- 领域解决方案供应商

- 组件特定平台

- 设计和开发即服务

- 软体维运服务 (SOaaS)

第六章 依车辆类型分類的市场估计与预测,2022-2035年

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型商用车

- 中型商用车(MCV)

- 重型商用车(HCV)

第七章 按应用领域分類的市场估算与预测,2022-2035年

- ADAS和自动驾驶平台

- 作业系统和中介软体平台

- 资讯娱乐和连接平台

- 车辆效率和性能平台

- 安全、安保和功能安全平台

第八章 按车型分類的市场估计与预测,2022-2035年

- 本地部署

- 私有云端

- 公共云端

- 杂交种

9. 依最终用途分類的市场估计与预测,2022-2035 年

- 技术原生型和SDV优先的OEM厂商

- 传统汽车製造商

- 一级和二级汽车零件製造商

- 汽车软体和技术供应商

- 半导体和计算平台提供商

第十章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 俄罗斯

- 波兰

- 罗马尼亚

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ANZ

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章:公司简介

- 世界公司

- Amazon Web Services(AWS)

- Aptiv

- ARM

- BlackBerry

- Continental

- Microsoft

- NVIDIA

- Qualcomm

- Robert Bosch

- 当地公司

- Elektrobit Automotive

- ETAS

- HERE Technologies

- Infineon Technologies

- NXP Semiconductors

- Red Hat

- Renesas Electronics

- STMicroelectronics

- TTTech Auto

- Visteon

- 新兴企业

- Aurora Innovation

- Canoo

- Motional

- Sonatus

- Woven by Toyota

The Global SDV-as-a-Service Platform Market was valued at USD 8.2 billion in 2025 and is estimated to grow at a CAGR of 26.3% to reach USD 85.7 billion by 2035.

Market growth directly links to rising consumer demand for smartphone-style vehicle experiences, frequent software enhancements, and highly personalized mobility features. Automakers actively respond by adopting cloud-enabled software platforms that support over-the-air updates, digital feature activation, and subscription-based services, allowing vehicles to evolve well after purchase. Vehicles increasingly function as software-defined products rather than static machines, enabling continuous value creation across the ownership lifecycle. This transformation reshapes revenue models, strengthens customer engagement, and expands post-sale monetization opportunities. OEMs rely on SDVaaS platforms to deliver scalable digital ecosystems that connect vehicles, drivers, and cloud services in real time. As expectations for seamless connectivity and intelligent features rise, SDVaaS becomes a foundational element in next-generation vehicle strategies across passenger and commercial segments worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.2 Billion |

| Forecast Value | $85.7 Billion |

| CAGR | 26.3% |

Automakers actively transition from distributed ECU structures to centralized computing supported by zonal electronic and electrical architectures. This architectural shift creates the technical foundation required for SDVaaS business models while simplifying vehicle wiring, improving system efficiency, and enabling unified service delivery across multiple platforms. Centralized and zonal designs allow software reuse, faster deployment of new features, and easier scalability across different vehicle lines. OEMs increasingly collaborate with cloud providers, AI developers, and technology companies to accelerate SDV platform maturity. These partnerships provide advanced analytics, high-performance computing, and secure cloud interfaces that shorten development timelines and support remote product creation, deployment, maintenance, and lifecycle management. SDVaaS platforms empower automakers to deliver richer digital experiences and maintain continuous interaction with customers throughout the vehicle lifespan.

The integrated SDV platform segment held 39% share in 2025 and will grow at a CAGR of 27% from 2026 to 2035. These providers dominate because they deliver comprehensive, end-to-end solutions that combine vehicle cloud infrastructure, operating systems, and application layers into unified platforms. Such integration supports large-scale OTA updates and enables dynamic service deployment across multiple vehicle models and product portfolios. By offering complete ecosystems rather than isolated tools, integrated providers simplify adoption for OEMs and accelerate the transition toward fully software-defined vehicles while ensuring consistency, security, and scalability across global fleets.

The hybrid deployment model segment held a 42% share in 2025 and is expected to grow at a CAGR of 27.3% through 2035. Hybrid SDVaaS deployments blend on-premises infrastructure with private and public cloud environments, giving enterprises greater operational flexibility and cost control. Automakers manage sensitive workloads locally while leveraging cloud scalability for data processing, analytics, and feature expansion. This approach allows precise cost optimization while meeting regulatory, performance, and security requirements. Hybrid deployments support phased SDV rollouts and enable OEMs to balance innovation speed with infrastructure stability as vehicle software complexity increases.

US SDV-as-a-Service Platform Market reached USD 2.62 billion in 2025. The US maintains leadership in SDV adoption due to strong collaboration between major automakers and technology firms, particularly within innovation hubs that advance connected vehicle infrastructure, OTA capabilities, V2X communication, and autonomous systems. Federal support strengthens this position through policies that encourage autonomous vehicle testing and connected mobility initiatives. These measures boost research investments and enable real-world validation of advanced SDV technologies across highways, smart corridors, and urban environments, positioning the US as a global center for SDV innovation and deployment.

Key players active in the Global SDV-as-a-Service Platform Market include NVIDIA, Bosch, Amazon Web Services, Qualcomm Technologies, Google, Continental, Microsoft, BlackBerry QNX, Vector Informatik, and Aptiv. Companies operating in the SDV-as-a-Service Platform Market strengthen their foothold by investing heavily in end-to-end software ecosystems, cloud-native architectures, and scalable computing platforms. Strategic alliances with automakers, semiconductor firms, and AI developers help providers expand technical capabilities and accelerate deployment timelines. Vendors focus on modular platform designs that allow OEMs to customize features while maintaining core system stability. Continuous innovation in cybersecurity, data analytics, and real-time vehicle intelligence remains central to competitive positioning.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Platform

- 2.2.3 Vehicle

- 2.2.4 Application

- 2.2.5 Deployment model

- 2.2.6 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Consumer demand for personalization

- 3.2.1.2 Centralized E/E architectures adoption

- 3.2.1.3 OEM-tech partnerships expansion

- 3.2.1.4 Regulatory-driven secure OTA

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cybersecurity and privacy risks

- 3.2.2.2 Fragmented cross-brand standards

- 3.2.3 Market opportunities

- 3.2.3.1 Subscription-based platform revenues

- 3.2.3.2 OEM-cloud strategic alliances

- 3.2.3.3 Third-party developer ecosystems

- 3.2.3.4 Data-driven mobility services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. Department of Transportation (DOT) Standards

- 3.4.1.2 Occupational Safety and Health Administration (OSHA) Guidelines

- 3.4.1.3 U.S. Environmental Protection Agency (EPA)

- 3.4.2 Europe

- 3.4.2.1 EN ISO Container Standards

- 3.4.2.2 European Union Customs and Safety Regulations

- 3.4.2.3 BS EN / CEN Standards

- 3.4.2.4 National Standards (UNE, DIN, etc.)

- 3.4.3 Asia Pacific

- 3.4.3.1 China GB (Guobiao) Standards

- 3.4.3.2 Japan JIS Requirements

- 3.4.3.3 Korea KS Certification

- 3.4.3.4 Indian BIS Standards

- 3.4.3.5 Thai Industrial Standards Institute (TISI)

- 3.4.4 Latin America

- 3.4.4.1 INMETRO (National Institute of Metrology)

- 3.4.4.2 INTI certification (Instituto Nacional de Tecnologia Industrial)

- 3.4.4.3 NOM standards (Norma Official Mexicana)

- 3.4.5 Middle East & Africa

- 3.4.5.1 ESMA / Emirates Conformity Assessment Scheme (ECAS)

- 3.4.5.2 GCC technical regulations

- 3.4.5.3 SABS certification

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Vendor cost structure

- 3.8.2 Implementation of cost components

- 3.8.3 Ongoing operational costs

- 3.8.4 Indirect customer costs

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Business & Monetization models

- 3.12.1 SDVaaS business model landscape

- 3.12.2 Platform licensing & subscription models

- 3.12.3 Usage-based & consumption pricing models

- 3.12.4 Development-as-a-service (DaaS) models

- 3.12.5 Revenue sharing & partnership models

- 3.13 Buyer decision criteria & procurement behavior

- 3.13.1 Buyer landscape overview

- 3.13.2 Decision-making process analysis

- 3.13.3 Critical evaluation criteria

- 3.13.4 Vendor selection & RFP process

- 3.13.5 Negotiation dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Platform, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Integrated SDV platform provider

- 5.3 Domain solution provider

- 5.4 Component specialist platform

- 5.5 Design & development as a service

- 5.6 Software operations as a service

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicle

- 6.3.1 LCV (Light commercial vehicle)

- 6.3.2 MCV (Medium commercial vehicle)

- 6.3.3 HCV (Heavy commercial vehicle)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 ADAS & autonomous driving platforms

- 7.3 Operating system & middleware platforms

- 7.4 Infotainment & connectivity platforms

- 7.5 Vehicle efficiency & performance platforms

- 7.6 Safety, security & functional safety platforms

Chapter 8 Market Estimates & Forecast, By Deployment model, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 On-Premises

- 8.3 Private Cloud

- 8.4 Public Cloud

- 8.5 Hybrid

Chapter 9 Market Estimates & Forecast, By End use, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Tech-native & SDV-first OEMs

- 9.3 Legacy automotive OEMs

- 9.4 Tier-1 & tier-2 automotive suppliers

- 9.5 Automotive software & technology providers

- 9.6 Semiconductor & computing platform providers

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 Amazon Web Services (AWS)

- 11.1.2 Aptiv

- 11.1.3 ARM

- 11.1.4 BlackBerry

- 11.1.5 Continental

- 11.1.6 Google

- 11.1.7 Microsoft

- 11.1.8 NVIDIA

- 11.1.9 Qualcomm

- 11.1.10 Robert Bosch

- 11.2 Regional players

- 11.2.1 Elektrobit Automotive

- 11.2.2 ETAS

- 11.2.3 HERE Technologies

- 11.2.4 Infineon Technologies

- 11.2.5 NXP Semiconductors

- 11.2.6 Red Hat

- 11.2.7 Renesas Electronics

- 11.2.8 STMicroelectronics

- 11.2.9 TTTech Auto

- 11.2.10 Visteon

- 11.3 Emerging players

- 11.3.1 Aurora Innovation

- 11.3.2 Canoo

- 11.3.3 Motional

- 11.3.4 Sonatus

- 11.3.5 Woven by Toyota