|

市场调查报告书

商品编码

1936530

犬类关节炎治疗市场机会、成长要素、产业趋势分析及2026年至2035年预测Canine Arthritis Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

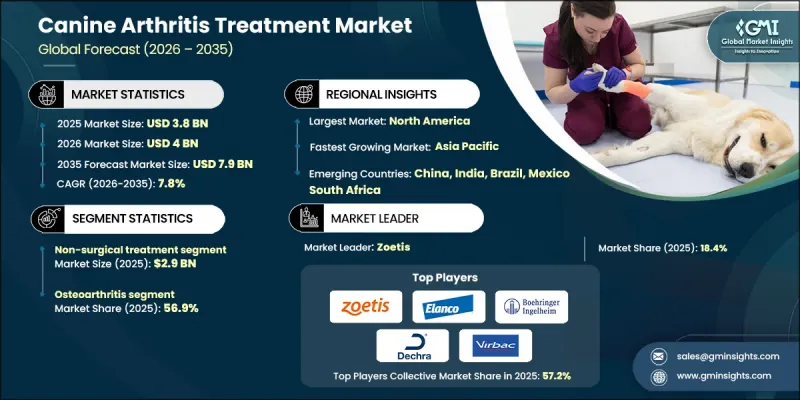

全球犬类关节炎治疗市场预计到 2025 年将达到 38 亿美元,到 2035 年将达到 79 亿美元,年复合成长率为 7.8%。

犬类骨关节炎(OA)发生率的上升推动了市场扩张。犬类关节炎的治疗方法多种多样,旨在缓解患有骨关节炎和其他退化性关节疾病的犬隻的关节疼痛、发炎和活动受限。这些治疗方法旨在透过个人化的多学科方法,根据疾病的严重程度和犬隻的个别需求,减轻不适、恢復关节功能并改善整体健康状况。治疗方案包括药物疗法,例如非类固醇消炎剂(NSAIDs)、皮质类固醇和鸦片类止痛药,以及新型生物疗法,例如单株抗体、含有葡萄糖胺和Omega-3脂肪酸的营养补充剂、物理疗法,以及在某些情况下进行的手术。多方面治疗策略的采用正在推动市场成长,因为药物疗法、补充剂和物理疗法的结合提供了一种更全面的管理方法,旨在改善犬隻的长期关节健康和活动能力。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 38亿美元 |

| 预测金额 | 79亿美元 |

| 复合年增长率 | 7.8% |

到2025年,非手术治疗市场将占据77.1%的份额,创造29亿美元的收入。这一主导地位反映出宠物饲主和兽医越来越倾向于在考虑手术干预之前,先尝试药物、单株抗体、补充剂和物理復健等非侵入性疗法。非手术疗法还具有成本效益高、易于取得等优势,可用于慢性疾病的长期管理。人们日益认识到疾病预防和延缓关节炎进展的重要性,这正推动着这些治疗方法在全球范围内被宠物广泛采用。

预计到2025年,骨关节炎细分市场将占犬类关节炎治疗市场56.9%的份额。骨关节炎是犬隻最常见的退化性关节疾病之一,也是犬类关节炎整体负担的重要组成部分。骨关节炎在各年龄层犬类中的发生率不断上升,凸显了製定有效长期管理策略的必要性,这也使得骨关节炎成为犬类关节炎治疗市场的主要细分领域。

预计到2025年,北美犬类关节炎治疗市占率将达到43.3%。该地区市场成长得益于宠物拥有率高、兽医护理支出高以及先进的兽医基础设施。强大的诊所、专科医院和诊断中心网络确保了对关节炎等慢性疾病的早期诊断和持续管理。北美宠物饲主对创新治疗方法的投入意愿进一步推动了多模式治疗方法和高品质兽药产品的普及。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 产业影响因素

- 司机

- 宠物拥有率不断提高以及宠物的人性化

- 犬类骨关节炎发生率不断上升

- 动物医药和治疗方法的进展

- 扩大兽医基础设施和远端医疗

- 产业潜在风险与挑战

- 长期治疗高成本

- 来自替代疗法的竞争

- 市场机会

- 下一代治疗方法的研发与商业化进展

- 司机

- 成长潜力分析

- 监管环境

- 各国养狗数量统计数据

- 管道分析

- 未来市场趋势

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 世界

- 北美洲

- 欧洲

- 亚太地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

5. 按治疗类型分類的市场估算与预测,2022-2035 年

- 非手术治疗

- 按类型

- 製药

- 非类固醇消炎剂(NSAIDs)

- 皮质类固醇

- 阿片类止痛药

- 其他药物

- 补充

- 葡萄糖胺

- 软骨素

- 甲基磺酰甲烷

- 其他补充剂

- 製药

- 透过行政途径

- 口服

- 注射

- 其他给药途径

- 透过分销管道

- 兽医院药房

- 零售药房

- 网路药房

- 按类型

- 外科手术

- 其他治疗方法

6. 按关节炎类型分類的市场估计和预测,2022-2035 年

- 骨关节炎

- 创伤性关节炎

- 骨软骨病

- 类风湿性关节炎

第七章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第八章:公司简介

- AdvaCare Pharma

- American Regent

- Auburn Laboratories

- Boehringer Ingelheim Animal Health

- CEVA Sante Animale

- Dechra Pharmaceuticals

- Deley Naturals

- Elanco Animal Health

- K9 Vitality

- Norbrook Laboratories

- Nutramax Laboratories Veterinary Sciences

- Thorne Vet

- Vetoquinol

- VetriScience

- VetStem

- Virbac

- Zoetis

The Global Canine Arthritis Treatment Market was valued at USD 3.8 billion in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 7.9 billion by 2035.

The market expansion is driven by the rising incidence of osteoarthritis (OA) in dogs. Canine arthritis treatment encompasses a range of therapies designed to manage joint pain, inflammation, and reduced mobility in dogs affected by osteoarthritis or other degenerative joint disorders. These treatments aim to alleviate discomfort, restore joint function, and improve overall well-being through individualized, multimodal approaches that match disease severity and the dog's specific needs. Options include pharmaceutical interventions such as NSAIDs, corticosteroids, and opioid pain relievers, along with newer biologic therapies like monoclonal antibodies, nutritional supplements including glucosamine and omega-3 fatty acids, physical therapy, and, in certain cases, surgical procedures. Adoption of multimodal treatment strategies has strengthened market growth, as combining medications, supplements, and physical therapies provides more comprehensive management for long-term joint health and improved mobility in dogs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.8 Billion |

| Forecast Value | $7.9 Billion |

| CAGR | 7.8% |

In 2025, the non-surgical treatments segment held a 77.1% share, generating USD 2.9 billion. This dominance reflects the growing preference among pet owners and veterinarians for non-invasive therapies, such as pharmaceuticals, monoclonal antibodies, supplements, and physical rehabilitation, before considering surgical intervention. Non-surgical approaches are also more cost-effective and accessible for managing chronic conditions over the long term. Increased awareness of disease prevention and the importance of slowing arthritis progression is encouraging broader adoption of these therapies among pet populations worldwide.

The osteoarthritis segment held 56.9% share in 2025. Osteoarthritis is one of the most common degenerative joint disorders in dogs, contributing significantly to the overall burden of canine arthritis. Rising OA prevalence across age groups emphasizes the need for effective, long-term management strategies, positioning osteoarthritis as the dominant segment in the canine arthritis treatment market.

North America Canine Arthritis Treatment Market accounted for 43.3% share in 2025. Market growth in this region is fueled by high pet ownership rates, substantial spending on veterinary care, and advanced veterinary infrastructure. A strong network of clinics, specialty hospitals, and diagnostic centers ensures early diagnosis and continuous management of chronic conditions such as arthritis. North American pet owners' willingness to invest in innovative treatments further drives the adoption of multimodal therapies and high-quality veterinary products.

Key players in the Global Canine Arthritis Treatment Market include Zoetis, VetriScience, Elanco Animal Health, Boehringer Ingelheim Animal Health, K9 Vitality, Dechra Pharmaceuticals, CEVA Sante Animale, Norbrook Laboratories, Nutramax Laboratories Veterinary Sciences, VetStem, Thorne Vet, Auburn Laboratories, Virbac, AdvaCare Pharma, Deley Naturals, American Regent, and JBT Corporation. Leading companies in the canine arthritis treatment market are implementing a range of strategies to strengthen their position and expand their market footprint. They are heavily investing in research and development to introduce innovative pharmaceuticals, biologics, and nutritional supplements tailored for canine joint health. Strategic partnerships with veterinary clinics, specialty hospitals, and distributors are being established to expand market access and provide localized support. Companies are also focusing on acquiring smaller firms with complementary technologies, allowing rapid portfolio expansion and entry into new geographies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Treatment type trends

- 2.2.3 Arthritis type trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership and humanization of pets

- 3.2.1.2 Increasing prevalence of osteoarthritis in dogs

- 3.2.1.3 Advancements in veterinary pharmaceuticals and therapies

- 3.2.1.4 Expansion of veterinary infrastructure and telemedicine

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of long-term treatment

- 3.2.2.2 Competition from alternative therapies

- 3.2.3 Market opportunities

- 3.2.3.1 Growing development and commercialization of next-generation therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Canine population statistics, by country

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Non-surgical treatment

- 5.2.1 By type

- 5.2.1.1 Pharmaceuticals

- 5.2.1.1.1 Non-steroidal anti-inflammatory drugs (NSAIDs)

- 5.2.1.1.2 Corticosteroids

- 5.2.1.1.3 Opioid pain relievers

- 5.2.1.1.4 Other pharmaceuticals

- 5.2.1.2 Supplements

- 5.2.1.2.1 Glucosamine

- 5.2.1.2.2 Chondroitin

- 5.2.1.2.3 Methylsulfonylmethane

- 5.2.1.2.4 Other supplements

- 5.2.1.1 Pharmaceuticals

- 5.2.2 By route of administration

- 5.2.2.1 Oral

- 5.2.2.2 Injectable

- 5.2.2.3 Other routes of administration

- 5.2.3 By distribution channel

- 5.2.3.1 Veterinary hospital pharmacies

- 5.2.3.2 Retail pharmacies

- 5.2.3.3 Online pharmacies

- 5.2.1 By type

- 5.3 Surgical procedures

- 5.4 Other treatment types

Chapter 6 Market Estimates and Forecast, By Arthritis Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Osteoarthritis

- 6.3 Traumatic arthritis

- 6.4 Osteochondrosis

- 6.5 Rheumatoid arthritis

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 AdvaCare Pharma

- 8.2 American Regent

- 8.3 Auburn Laboratories

- 8.4 Boehringer Ingelheim Animal Health

- 8.5 CEVA Sante Animale

- 8.6 Dechra Pharmaceuticals

- 8.7 Deley Naturals

- 8.8 Elanco Animal Health

- 8.9 K9 Vitality

- 8.10 Norbrook Laboratories

- 8.11 Nutramax Laboratories Veterinary Sciences

- 8.12 Thorne Vet

- 8.13 Vetoquinol

- 8.14 VetriScience

- 8.15 VetStem

- 8.16 Virbac

- 8.17 Zoetis