|

市场调查报告书

商品编码

1936533

汽车高压电容器市场机会、成长要素、产业趋势分析及2026年至2035年预测Automotive High Voltage Electric Capacitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

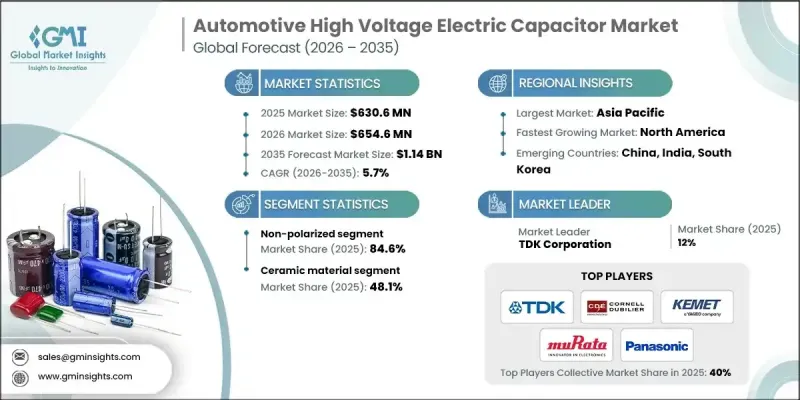

全球汽车高压电容器市场预计到 2025 年将达到 6.306 亿美元,到 2035 年将达到 11.4 亿美元,年复合成长率为 5.7%。

由于汽车架构向 800 伏特的过渡,市场正呈现强劲的成长动能。 800 伏特的架构能够实现更快的充电速度、更轻的电缆重量以及在指定功率下更低的电流。汽车製造商正在将驱动系统从约 400 伏特升级到 800 伏特,以提高效率和性能。电压的提升对逆变器和车载充电器提出了更高的电气负载要求,因此,高品质的直流链路电容器对于确保电源稳定性、低 ESR/ESL 性能、高纹波电流承受能力和热可靠性至关重要。采用碳化硅 (SiC) 逆变器扩大了开关频率范围,这就要求电容器设计具备更严格的电感控制、先进的自修復薄膜以及在严苛的汽车工况下依然能够保持的强大耐久性。随着双马达全轮驱动和双向动力系统的普及,这些电容器对于抑制电磁干扰 (EMI)、能量回收煞车和维持电能品质也至关重要。公共直流快速充电基础设施的普及进一步增加了尖峰功率需求,对高压电容器提出了更高的电气和热负载要求,凸显了耐用设计的重要性。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 6.306亿美元 |

| 预测金额 | 11.4亿美元 |

| 复合年增长率 | 5.7% |

预计到2025年,非极化电容器市占率将达到84.6%,并在2035年之前以5.6%的复合年增长率成长。非极化直流链路电容器是电动汽车驱动逆变器和DC/DC转换器中高频去耦的基础技术。 SiC和GaN开关的广泛应用要求电容器具备低ESR/ESL、高涟波电流容量以及在高速开关条件下优异的自癒性能。製造商正在推出专为800-920V系统设计的模组化直流链路薄膜电容器。这些电容器可降低电感、简化并联,并实现紧凑布局,同时也能提高车辆运行工况下的热性能。在各种运作环境和条件下,性能、可靠性和效率至关重要,因此这些解决方案在高压电动车平台中变得越来越重要。

极化电解电容器市场(包括电解电容器和混合聚合物电解电容器)预计到2035年将以5%的复合年增长率成长。在高压汽车应用中,这些电容器作为直流母线上的大容量储能元件,能够有效处理高功率整流引起的低频纹波,并缓衝超快速充电和逆变器功率提升所带来的电压瞬变。它们的重新兴起满足了对大容量储能、高电容密度和纹波电流耐受性的需求,是对非极化直流母线薄膜电容器性能的有力补充。

预计2025年,美国汽车高压电容器市场将占75%的市场份额,市场规模达8,910万美元。该地区的成长主要得益于高功率充电通道的快速扩张、车队电气化以及直流母线电压要求的不断提高,这些因素都要求车载电容器能够承受更严苛的电气和热工况。联邦政府的倡议、资助计画和标准化工作正在为电动车基础设施制定互通性、可靠性和性能要求,并间接影响电容器的规格。这推动了对更高涟波容差、低等效串联电阻/等效串联电阻以及优异的热稳定性和湿度稳定性的需求。消费者对电动车的接受度不断提高以及政府对电气化倡议的支持,也进一步促进了市场成长。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 监管环境

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 成长潜力分析

- 波特五力分析

- PESTEL 分析

- 新的机会与趋势

- 数位化和物联网集成

- 拓展新兴市场

第四章 竞争情势

- 介绍

- 公司市占率分析

- 策略倡议

- 竞争标竿分析

- 战略仪錶板

- 创新与科技趋势

第五章 依极化程度分類的市场规模及预测(2022-2035年)

- 偏振

- 非极化

第六章 依材料分類的市场规模及预测(2022-2035年)

- 薄膜电容器

- 陶瓷电容器

- 电解电容器

- 其他的

第七章 2022-2035年各地区市场规模及预测

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 法国

- 德国

- 义大利

- 奥地利

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

第八章:公司简介

- 芦荟电容器

- 奥斯汀电气外壳和电容器

- Cornell Dubilier

- United Chemi-Con

- Elna

- Havells

- Kemet

- Kyocera AVX

- Lelon Electronics

- Murata Manufacturing

- Nichicon Corporation

- Panasonic

- RUBYCON Corporation

- Samsung Electro-Mechanics

- Schneider Electric

- Siemens

- Taiyo Yuden

- TDK

- Vishay Intertechnology

- Yageo Group

The Global Automotive High Voltage Electric Capacitor Market was valued at USD 630.6 million in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 1.14 billion by 2035.

The market is witnessing strong momentum due to the shift toward 800-volt vehicle architectures, which are enabling faster charging, reduced cable weight, and lower current for a given power. Automakers are upgrading traction systems from ~400 V to 800 V to enhance efficiency and performance. This voltage escalation increases electrical stress on inverters and onboard chargers, making high-quality DC link capacitors critical for power stability, low ESR/ESL performance, high ripple current tolerance, and thermal reliability. Adoption of SiC-based inverters is widening switching frequency ranges, necessitating capacitor designs with tighter inductance control, advanced self-healing films, and robust endurance under harsh automotive duty cycles. With dual-motor all-wheel-drive and bidirectional power systems becoming more common, these capacitors are also crucial for EMI suppression, regenerative braking, and maintaining power quality. Rising public DC fast charging infrastructure further drives peak power requirements, imposing heavier electrical and thermal loads on HV capacitors, underscoring the need for durable designs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $630.6 Million |

| Forecast Value | $1.14 Billion |

| CAGR | 5.7% |

The non-polarized capacitor segment accounted for 84.6% share in 2025 and is expected to grow at a CAGR of 5.6% through 2035. Non-polarized DC link capacitors are the backbone of high-frequency decoupling in EV traction inverters and DC/DC converters. The widespread adoption of SiC and GaN switches demands low ESR/ESL, high ripple current capacity, and superior self-healing under fast switching conditions. Manufacturers are launching modular DC link film capacitors designed for 800-920 V systems, which reduce inductance, simplify parallelization, and allow compact layouts while improving thermal performance under automotive duty cycles. These solutions are increasingly essential in high-voltage EV platforms where performance, reliability, and efficiency are critical under varying operational and environmental conditions.

The polarized electrolytic capacitors segment, including aluminum and hybrid polymer types, is forecast to grow at a CAGR of 5% by 2035. In HV automotive applications, these capacitors serve as bulk energy reservoirs on DC buses, efficiently handling low-frequency ripple from high-power rectification and buffering voltage transients associated with ultra-fast charging and rising inverter power levels. Their renewed adoption supports applications where large energy storage, high capacitance density, and tolerance to ripple currents are required, complementing the performance of non-polarized DC link film capacitors.

U.S. Automotive High Voltage Electric Capacitor Market held 75% share in 2025, generating USD 89.1 million. Growth in this region is driven by rapid expansion of high-power charging corridors, fleet electrification, and rising DC bus voltage requirements, which push onboard capacitors to withstand harsher electrical and thermal profiles. Federal initiatives, funding programs, and standardization efforts are establishing interoperability, reliability, and performance expectations for EV infrastructure, indirectly shaping capacitor specifications to meet higher ripple endurance, lower ESL/ESR, and robust thermal and humidity bias performance. Increasing consumer adoption of EVs and government support for electrification initiatives further reinforce market growth.

Key players in the Global Automotive High Voltage Electric Capacitor Market include Vishay Intertechnology, Murata Manufacturing, Nichicon Corporation, TDK, Yageo Group, Panasonic, RUBYCON Corporation, Aloe Capacitors, Austin Electrical Enclosures & Capacitors, Cornell Dubilier, United Chemi-Con, Elna, Havells, Kemet, Kyocera AVX, Lelon Electronics, Schneider Electric, and Siemens. Companies in the Automotive High Voltage Electric Capacitor Market are pursuing strategies to strengthen their market presence by investing in R&D to develop capacitors with higher thermal endurance, lower ESR/ESL, and improved ripple current tolerance suitable for 800-920 V systems. Firms are expanding production capacities and forming partnerships with automakers and power electronics suppliers to ensure integration in next-generation EV platforms. Modular capacitor design and scalable solutions enable faster adoption across diverse EV architectures. Strategic acquisitions and collaborations are also being leveraged to access advanced materials, self-healing film technology, and SiC/GaN inverter expertise.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Polarization trends

- 2.1.3 Material trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Polarization, 2022 - 2035 (‘000 Units, USD Million)

- 5.1 Key trends

- 5.2 Polarized

- 5.3 Non-polarized

Chapter 6 Market Size and Forecast, By Material, 2022 - 2035 (‘000 Units, USD Million)

- 6.1 Key trends

- 6.2 Film capacitor

- 6.3 Ceramic capacitor

- 6.4 Electrolytic capacitor

- 6.5 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (‘000 Units, USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.3.5 Austria

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 South Africa

- 7.5.3 UAE

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 Aloe Capacitors

- 8.2 Austin Electrical Enclosures & Capacitors

- 8.3 Cornell Dubilier

- 8.4 United Chemi-Con

- 8.5 Elna

- 8.6 Havells

- 8.7 Kemet

- 8.8 Kyocera AVX

- 8.9 Lelon Electronics

- 8.10 Murata Manufacturing

- 8.11 Nichicon Corporation

- 8.12 Panasonic

- 8.13 RUBYCON Corporation

- 8.14 Samsung Electro-Mechanics

- 8.15 Schneider Electric

- 8.16 Siemens

- 8.17 Taiyo Yuden

- 8.18 TDK

- 8.19 Vishay Intertechnology

- 8.20 Yageo Group