|

市场调查报告书

商品编码

1936567

机械往復式发动机市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Mechanical Reciprocating Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

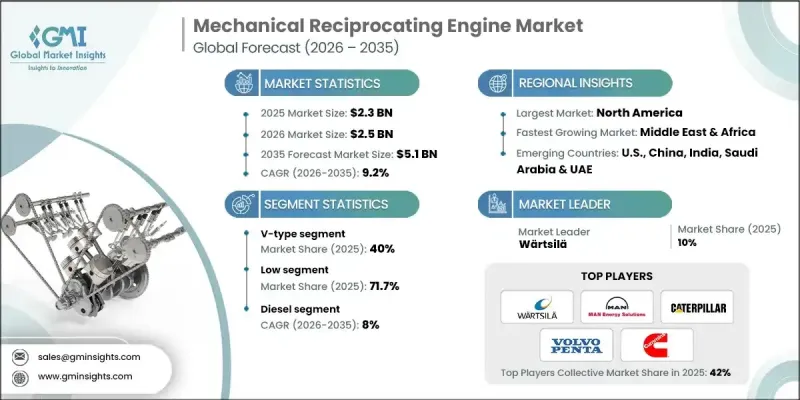

全球机械往復式引擎市场预计到 2025 年将达到 23 亿美元,到 2035 年将达到 51 亿美元,年复合成长率为 9.2%。

市场扩张得益于工业基础设施的持续发展以及政府机构和私营部门不断增加的资本投资。这些投资促进了产能扩张、设施现代化和更广泛的产业多元化,共同创造了多个终端用户领域的持续需求。机械往復式引擎凭藉其久经考验的可靠性和适应性,在全球动力和运动系统中继续发挥至关重要的作用。这些引擎透过连续的运行循环,将气缸内活塞的直线运动转化为旋转运动,从而在各种运行条件下提供稳定的动力。对农村电气化的日益重视、支持性的法规结构以及对备用和紧急电源需求的日益增长的认识,正在推动市场成长。政府主导的电力普及计画进一步增强了需求。儘管机械往復式引擎技术已经成熟,但在持续和间歇运行环境下对可靠机械动力的需求不断增长的驱动下,该行业仍在透过提高效率和优化排放气体不断发展。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 23亿美元 |

| 预测金额 | 51亿美元 |

| 复合年增长率 | 9.2% |

预计到2035年,直列式引擎市场规模将达14亿美元。该市场的成长主要归功于其结构简单、性能可靠且易于维护。直列式引擎具有动力输出稳定、运作效率高、使用寿命长等优点,使其成为成本控制、耐用性和易维护性要求较高的应用领域的理想选择。其在众多工业和交通运输相关应用领域的广泛适用性也持续支撑着市场需求的稳定成长。

预计到2025年,低速机械往復式引擎市占率将达到71.7%,到2035年市场规模将达到35亿美元。该细分市场受益于重型发电和推进系统日益增长的需求,这些系统需要长期稳定的性能。低速机械往復式引擎因其燃油效率高、机械强度高以及能够在严苛负载条件下连续运转而备受青睐,使其成为高能耗工业应用的首选。

据估计,到2025年,美国机械往復式引擎市场规模将达到8.262亿美元,占全球市场份额的74%。美国市场强劲成长的驱动力来自发电、船舶作业和工业设备应用领域对可靠高效引擎的持续需求。引擎技术的不断进步、对监管要求的不断满足以及对排放气体日益增长的关注,都在推动市场普及并增强市场的长期稳定性。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 原物料供应及采购分析

- 製造能力评估

- 供应链韧性与风险因素

- 配电网路分析

- 监管环境

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 成长潜力分析

- 波特五力分析

- PESTEL 分析

- 船用往復式引擎成本结构分析

- 价格趋势分析(美元/兆瓦)

- 按地区

- 按额定输出

- 投资分析及未来展望

- 将永续发展措施与工业4.0结合

第四章 竞争情势

- 介绍

- 按地区分類的公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 战略仪錶板

- 策略倡议

- 重要伙伴关係与合作

- 重大併购活动

- 产品创新与新产品发布

- 市场扩大策略

- 竞争标竿分析

- 创新与永续性格局

第五章 依燃料类型分類的市场规模及预测(2022-2035年)

- 气体

- 柴油引擎

- 其他的

第六章 依额定产量区分的市场规模及预测,2022-2035年

- 0.5 MW~1 MW

- 1兆瓦以上~2兆瓦

- 2兆瓦至3.5兆瓦

- 3.5兆瓦~5兆瓦以上

第七章 依成长速度分類的市场规模及预测,2022-2035年

- 慢速

- 中速

- 高速

8. 依汽缸配置分類的市场规模及预测,2022-2035年

- 系列

- V型

- 径向

- 对置活塞

第九章 2022-2035年各地区市场规模及预测

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 法国

- 德国

- 俄罗斯

- 义大利

- 西班牙

- 荷兰

- 丹麦

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 泰国

- 新加坡

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 卡达

- 阿曼

- 科威特

- 埃及

- 土耳其

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

第十章:公司简介

- AB Volvo Penta

- Caterpillar

- Cummins

- Deutz AG

- Doosan Corporation

- Escorts Kubota Limited

- Fairbanks Morse Defense

- GE Vernova

- JC Bamford Excavators Ltd.

- Kawasaki Heavy Industries, Ltd.

- KUBOTA Corporation

- Lister Petter

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Motorenfabrik Hatz GmbH &Co. KG

- Perkins Engines Company Limited

- Rehlko

- Rolls-Royce

- Siemens Energy

- Wartsila

The Global Mechanical Reciprocating Engine Market was valued at USD 2.3 billion in 2025 and is estimated to grow at a CAGR of 9.2% to reach USD 5.1 billion by 2035.

Market expansion is supported by the continued development of industrial infrastructure and rising capital investment from both government bodies and private sector participants. These investments are contributing to capacity expansion, facility modernization, and broader industrial diversification, which together are creating sustained demand across multiple end-use sectors. Mechanical reciprocating engines continue to play a critical role within global power and motion systems due to their proven reliability and adaptability. These engines operate by converting linear piston movement within cylinders into rotational mechanical output through sequential operating cycles, delivering dependable power across a wide range of operating conditions. Increasing focus on rural electrification, supportive regulatory frameworks, and heightened awareness of backup and emergency power requirements are reinforcing market growth. Government-led power access initiatives are further strengthening demand. Despite being a mature technology, the segment continues to evolve through efficiency improvements and emissions optimization, driven by rising requirements for dependable mechanical power in both continuous and intermittent operating environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.3 Billion |

| Forecast Value | $5.1 Billion |

| CAGR | 9.2% |

The inline engine configuration segment is projected to reach USD 1.4 billion by 2035. Growth in this segment is attributed to its simple structural layout, dependable performance, and ease of servicing. Engines with a linear cylinder arrangement provide stable output, operational efficiency, and long service life, making them well-suited for applications where cost control, durability, and maintenance simplicity are essential. Their broad applicability across multiple industrial and mobility-related uses continues to support steady demand.

The low-speed mechanical reciprocating engines segment accounted for 71.7% share in 2025 and is expected to reach USD 3.5 billion by 2035. This segment is benefiting from increasing reliance on heavy-duty power generation and propulsion systems that require consistent performance over extended operating periods. These engines are favored for their fuel efficiency, mechanical robustness, and ability to operate continuously under demanding load conditions, making them a preferred choice for energy-intensive industrial applications.

United States Mechanical Reciprocating Engine Market held 74% share, generating USD 826.2 million in 2025. Market strength in the country is driven by sustained demand for reliable and efficient engines across power generation, marine operations, and industrial equipment usage. Continued advancements in engine technology, adherence to regulatory requirements, and an increased focus on emissions performance are supporting adoption and reinforcing long-term market stability.

Key companies operating in the Global Mechanical Reciprocating Engine Market include Caterpillar, Cummins, Wartsila, MAN Energy Solutions, Mitsubishi Heavy Industries, Rolls-Royce, Siemens Energy, Kawasaki Heavy Industries, AB Volvo Penta, KUBOTA Corporation, Perkins Engines Company, Deutz AG, Fairbanks Morse Defense, GE Vernova, Doosan Corporation, Motorenfabrik Hatz, Escorts Kubota, JC Bamford Excavators, Lister Petter, and Rehlko. Companies active in the mechanical reciprocating engine market are strengthening their competitive position through technology enhancement, portfolio diversification, and strategic geographic expansion. Leading manufacturers are investing in improved fuel efficiency, emissions reduction technologies, and advanced control systems to meet evolving regulatory and customer requirements. Many players are expanding service networks and aftermarket support to improve lifecycle value and customer retention. Strategic partnerships with industrial operators and infrastructure developers are enabling tailored engine solutions for specific applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Fuel trends

- 2.1.3 Rated power trends

- 2.1.4 Speed trends

- 2.1.5 Cylinder configuration trends

- 2.1.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of marine reciprocating engines

- 3.8 Price trend analysis (USD/MW)

- 3.8.1 By region

- 3.8.2 By rated power

- 3.9 Investment analysis & future prospects

- 3.10 Sustainability initiatives & industry 4.0 integration

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.4.1 Key partnerships & collaborations

- 4.4.2 Major M&A activities

- 4.4.3 Product innovations & launches

- 4.4.4 Market expansion strategies

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 Gas

- 5.3 Diesel

- 5.4 Others

Chapter 6 Market Size and Forecast, By Rated Power, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 0.5 MW - 1 MW

- 6.3 > 1 MW - 2 MW

- 6.4 > 2 MW - 3.5 MW

- 6.5 > 3.5 MW - 5 MW

Chapter 7 Market Size and Forecast, By Speed, 2022 - 2035 (USD Million & MW)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Size and Forecast, By Cylinder Configuration, 2022 - 2035 (USD Million & MW)

- 8.1 Key trends

- 8.2 Inline

- 8.3 V-type

- 8.4 Radial

- 8.5 Opposed piston

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MW)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 France

- 9.3.3 Germany

- 9.3.4 Russia

- 9.3.5 Italy

- 9.3.6 Spain

- 9.3.7 Netherlands

- 9.3.8 Denmark

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Thailand

- 9.4.7 Singapore

- 9.5 Middle East & Africa

- 9.5.1 UAE

- 9.5.2 Saudi Arabia

- 9.5.3 Qatar

- 9.5.4 Oman

- 9.5.5 Kuwait

- 9.5.6 Egypt

- 9.5.7 Turkey

- 9.5.8 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

- 9.6.3 Chile

Chapter 10 Company Profiles

- 10.1 AB Volvo Penta

- 10.2 Caterpillar

- 10.3 Cummins

- 10.4 Deutz AG

- 10.5 Doosan Corporation

- 10.6 Escorts Kubota Limited

- 10.7 Fairbanks Morse Defense

- 10.8 GE Vernova

- 10.9 JC Bamford Excavators Ltd.

- 10.10 Kawasaki Heavy Industries, Ltd.

- 10.11 KUBOTA Corporation

- 10.12 Lister Petter

- 10.13 MAN Energy Solutions

- 10.14 Mitsubishi Heavy Industries

- 10.15 Motorenfabrik Hatz GmbH & Co. KG

- 10.16 Perkins Engines Company Limited

- 10.17 Rehlko

- 10.18 Rolls-Royce

- 10.19 Siemens Energy

- 10.20 Wartsila

2026年史特灵引擎全球市场报告

2026年史特灵引擎全球市场报告 先进触媒技术市场分析及预测(至2035年):类型、产品、技术、应用、材料类型、最终用户、製程、组件、安装类型

先进触媒技术市场分析及预测(至2035年):类型、产品、技术、应用、材料类型、最终用户、製程、组件、安装类型 汽车引擎活塞环:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

汽车引擎活塞环:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球同步环市场规模、份额、趋势和成长分析报告(2026-2034)2026年全球铝活塞市场报告2026年全球氢内燃机市场报告

全球同步环市场规模、份额、趋势和成长分析报告(2026-2034)2026年全球铝活塞市场报告2026年全球氢内燃机市场报告 汽车引擎市场-全球产业规模、份额、趋势、机会、预测:按车辆类型、部署类型、燃料类型、地区和竞争格局划分,2021-2031年汽车引擎皮带市场-全球产业规模、份额、趋势、机会与预测:按服务类型、车辆类型、使用者群体、地区和竞争格局划分,2021-2031年

汽车引擎市场-全球产业规模、份额、趋势、机会、预测:按车辆类型、部署类型、燃料类型、地区和竞争格局划分,2021-2031年汽车引擎皮带市场-全球产业规模、份额、趋势、机会与预测:按服务类型、车辆类型、使用者群体、地区和竞争格局划分,2021-2031年 双燃料氨发动机市场:按功率输出、发动机类型、燃料混合比、最终用途和应用分類的全球预测(2026-2032年)引擎油底壳市场按车辆类型、材质、油底壳类型、通路和最终用途产业划分-2026-2032年全球预测

双燃料氨发动机市场:按功率输出、发动机类型、燃料混合比、最终用途和应用分類的全球预测(2026-2032年)引擎油底壳市场按车辆类型、材质、油底壳类型、通路和最终用途产业划分-2026-2032年全球预测