|

市场调查报告书

商品编码

1936570

蔬果加工设备市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Fruit and Vegetable Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

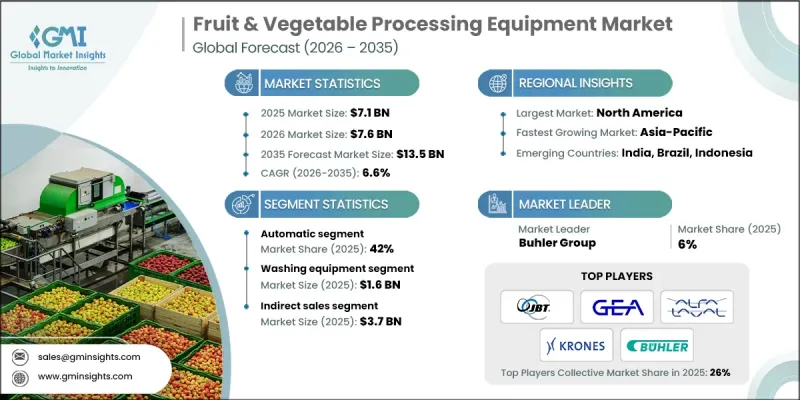

全球蔬果加工设备市场预计到 2025 年将达到 71 亿美元,到 2035 年将达到 135 亿美元,年复合成长率为 6.6%。

儘管该市场潜力巨大,但也面临着许多挑战,例如先进机械设备所需的高初始投资以及严格的国际食品安全标准。先进自动化设备的成本等因素可能会限制中小型製造商进入新兴市场,从而阻碍该行业充分发挥其潜力。北美地区对便捷即食食品的需求不断增长等消费趋势正在推动市场成长,而欧洲不断变化的法规和亚太地区的快速工业化则为商业化奠定了基础。消费者对营养丰富、保质期长的生鲜食品替代品的需求不断增长,促使加工设备成为关注焦点,而高压加工 (HPP) 和无菌包装等技术能够有效保留食品的风味和营养价值。日益增强的食品安全意识正在推动全球食品製造商采用先进的加工系统,从而持续扩大市场规模。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 71亿美元 |

| 预测金额 | 135亿美元 |

| 复合年增长率 | 6.6% |

到2025年,自动化领域将占据42%的市场份额,这主要得益于大规模生产的需求、降低人事费用以及对高加工精度的追求。全自动系统利用感测器和可程式逻辑控制器(PLC)完成清洗、去皮和切割等工序,最大限度地减少人工干预。这些系统在工业规模化生产中效率极高,能够轻柔地处理娇嫩的水果和蔬菜,减少物理损伤并最大限度地减少废弃物。然而,传统的手动操作往往会导致产品品质不稳定和废弃物增加,因此自动化对大型加工商的吸引力日益增强。

预计到2025年,间接销售业务将创造37亿美元的收入,占据主要市场份额。这一主导地位主要归功于本地分销商,他们透过在各个地区提供安装、维护和售后服务,扩大了设备製造商的业务范围,确保设备在不同地区可靠、快速地部署。

预计2025年,北美蔬果加工设备市场规模将达16亿美元。该地区高昂的人事费用推动了自动化加工解决方案的普及,而消费者日益增强的食品安全意识则推动了对先进设备的需求。北美在食品加工创新方面处于领先地位,高压加工(HPP)系统和人工智慧分类技术得到了快速应用。此外,美国食品药物管理局(FDA)的严格法规和永续性措施也在推动市场发展,为那些既能优化水和能源消耗又能满足安全和品质标准的设备创造了有利环境。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 产业影响因素

- 司机

- 对简便食品的需求迅速成长

- 向健康意识消费的转变

- 自动化和人工智慧集成

- 产业潜在风险与挑战

- 高初始资本投入

- 复杂的监理合规

- 机会

- 低温运输基础设施的扩展

- 新兴市场的采用情况

- 司机

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按类型

- 监管环境

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 按类型分類的市场估算与预测,2022-2035年

- 打扫

- 去皮

- 断开

- 果汁生产

- 漂烫

- 包装

- 其他的

第六章 2022-2035年各业务领域的市场估算与预测

- 自动的

- 半自动

- 手动的

7. 按最终用户分類的市场估计和预测,2022-2035 年

- 食品加工业

- 食品服务供应商

第八章 按类别分類的市场估计和预测,2022-2035年

- 水果

- 蔬菜

第九章 按应用领域分類的市场估算与预测,2022-2035年

- 生鲜产品和切好的蔬菜

- 罐头

- 干燥/脱水

- 冷冻

- 其他(泡菜、调味料等)

第十章 依最终用途产业分類的市场估计与预测,2022-2035年

- 小规模加工厂

- 中型加工厂

- 工业/大型加工厂

第十一章 按分销管道分類的市场估算与预测,2022-2035年

- 直销

- 间接销售

第十二章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十三章:公司简介

- Alfa Laval AB

- Bertuzzi Food Processing Srl

- Bucher Industries AG

- Buhler Group

- FENCO Food Machinery Srl

- GEA Group

- Heat and Control, Inc.

- JBT Corporation

- Key Technology, Inc.

- Krones AG

- Lyco Manufacturing, Inc.

- Marel

- Mepaco

- Navatta Group Food Processing Srl

- Sormac BV

The Global Fruit & Vegetable Processing Equipment Market was valued at USD 7.1 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 13.5 billion by 2035.

The market holds immense potential, but it faces challenges, primarily due to the high initial investment required for sophisticated machinery and stringent international food safety standards. These factors, particularly the cost of advanced automation, may limit smaller manufacturers from entering emerging markets and hinder the sector from reaching its full potential. Consumer trends, such as the growing demand for convenient, ready-to-eat food in North America, are shaping market growth, while evolving regulations in Europe and rapid industrialization in Asia Pacific are laying the commercial foundation. As demand increases for nutrient-rich, long shelf-life alternatives to fresh produce, processing equipment is gaining traction, offering techniques that preserve flavor and nutritional content, including high-pressure processing (HPP) and aseptic packaging. Heightened awareness of food safety is further motivating food manufacturers worldwide to adopt advanced processing systems, driving sustained market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.1 Billion |

| Forecast Value | $13.5 Billion |

| CAGR | 6.6% |

In 2025, the automatic segment accounted for 42% share, driven by the need for high-volume production, labor cost savings, and precision in processing. Fully automated systems move produce through washing, peeling, and cutting stages with minimal human involvement, using sensors and programmable logic controllers (PLCs). These systems are highly efficient for industrial-scale operations and handle delicate fruits and vegetables with care, reducing physical damage and minimizing waste. In contrast, traditional manual methods often lead to inconsistent product quality and higher wastage, making automation increasingly attractive for large-scale processors.

Indirect sales segment generated USD 3.7 billion in 2025, capturing a major market share. This dominance is largely due to local distributors who extend the reach of equipment manufacturers by providing installation, maintenance, and after-sales support in various regions, ensuring equipment reliability and faster adoption across diverse geographies.

North America Fruit & Vegetable Processing Equipment Market reached USD 1.6 billion in 2025. The region's high labor costs encourage the adoption of automated processing solutions, while strong consumer awareness of food safety drives demand for advanced equipment. North America is a leader in food processing innovation, with rapid adoption of HPP systems and AI-enabled sorting technologies. Strict FDA regulations and sustainability initiatives further reinforce the market, creating favorable conditions for equipment that optimizes water and energy consumption while meeting safety and quality standards.

Key players in the Global Fruit & Vegetable Processing Equipment Market include Alfa Laval AB, Bertuzzi Food Processing S.r.l., Bucher Industries AG, Buhler Group, FENCO Food Machinery S.r.l., GEA Group, Heat and Control, Inc., JBT Corporation, Key Technology, Inc., Krones AG, Lyco Manufacturing, Inc., Marel, Mepaco, Navatta Group Food Processing S.r.l., and Sormac B.V. Companies in this market are employing several strategies to strengthen their foothold and expand their presence. They are investing heavily in research and development to deliver high-efficiency, next-generation equipment with advanced automation and food safety features. Long-term partnerships with distributors and OEMs are secured to ensure market reach and reliable after-sales service. Strategic acquisitions and collaborations allow companies to broaden their product portfolios and enter new geographical markets. Manufacturers are also focusing on customizing equipment to meet local regulations and production requirements, while expanding regional production capacities to reduce costs and improve lead times. Additionally, companies are leveraging sustainability-focused innovations, such as energy- and water-efficient systems, to enhance competitiveness and align with global environmental standards, driving long-term growth and market leadership.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Operation

- 2.2.4 End Users

- 2.2.5 Category

- 2.2.6 Application

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in Demand for Convenience Foods

- 3.2.1.2 Shift Toward Health-Conscious Consumption

- 3.2.1.3 Automation and AI Integration

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Initial Capital Investment

- 3.2.2.2 Complex Regulatory Compliance

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of Cold-Chain Infrastructure

- 3.2.3.2 Emerging Markets Adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Washing

- 5.3 Peeling

- 5.4 Cutting

- 5.5 Juicing

- 5.6 Blanching

- 5.7 Packaging

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Operation 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automatic

- 6.3 Semi-automatic

- 6.4 Manual

Chapter 7 Market Estimates & Forecast, By End Users, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Food Processing Industries

- 7.3 Foodservice Providers

Chapter 8 Market Estimates & Forecast, By Category, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Fruits

- 8.3 Vegetables

Chapter 9 Market Estimates & Forecast, By Application, 2022-2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Fresh & Fresh-Cut

- 9.3 Canned

- 9.4 Drying & Dehydration

- 9.5 Frozen

- 9.6 Others (Pickling & seasoning, etc.)

Chapter 10 Market Estimates & Forecast, By End Use Industries, 2022-2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Small-Scale Processing plants

- 10.3 Medium-Scale Processing plants

- 10.4 Industrial/Large-Scale Processing plants

Chapter 11 Market Estimates & Forecast, By Distribution channel, 2022-2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Direct sales

- 11.3 Indirect sales

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 India

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Alfa Laval AB

- 13.2 Bertuzzi Food Processing S.r.l.

- 13.3 Bucher Industries AG

- 13.4 Buhler Group

- 13.5 FENCO Food Machinery S.r.l.

- 13.6 GEA Group

- 13.7 Heat and Control, Inc.

- 13.8 JBT Corporation

- 13.9 Key Technology, Inc.

- 13.10 Krones AG

- 13.11 Lyco Manufacturing, Inc.

- 13.12 Marel

- 13.13 Mepaco

- 13.14 Navatta Group Food Processing S.r.l.

- 13.15 Sormac B.V.

食品加工与处理设备市场:2026-2032年全球市场预测(依设备类型、运作模式、技术、加工能力、设备材质及最终用户划分)乳酪加工设备市场:2026-2032年全球市场预测(按产品类型、技术、产能、乳酪类型和最终用户划分)鸡蛋加工机械市场:2026-2032年全球市场预测(按机器类型、产品类型、製程、最终用途、自动化程度、产能和最终用户划分)水果加工市场:按产品类型、水果品种、分销管道和最终用途分類的全球市场预测 - 2026-2032 年商用奶昔机市场:按类型、容量、技术、动力来源、最终用户和销售管道划分-2026-2032年全球市场预测商用烤肉设备市场:按设备类型、容量、动力来源、最终用户和应用划分-2026-2032年全球市场预测腌製和滚揉设备市场:按类型、技术、产能、应用和最终用户划分-2026-2032年全球预测谷物加工设备市场:按设备类型、谷物类型、最终用途、製程、加工能力、技术和分销管道划分-全球预测,2026-2032年食品加工机械市场:按设备类型、自动化程度、运作模式、产能范围、动力来源和最终用途产业分類的全球预测,2026-2032年食品加工机械设备市场:依机器类型、操作方式、技术、应用、最终用户和分销管道划分,全球预测,2026-2032年

食品加工与处理设备市场:2026-2032年全球市场预测(依设备类型、运作模式、技术、加工能力、设备材质及最终用户划分)乳酪加工设备市场:2026-2032年全球市场预测(按产品类型、技术、产能、乳酪类型和最终用户划分)鸡蛋加工机械市场:2026-2032年全球市场预测(按机器类型、产品类型、製程、最终用途、自动化程度、产能和最终用户划分)水果加工市场:按产品类型、水果品种、分销管道和最终用途分類的全球市场预测 - 2026-2032 年商用奶昔机市场:按类型、容量、技术、动力来源、最终用户和销售管道划分-2026-2032年全球市场预测商用烤肉设备市场:按设备类型、容量、动力来源、最终用户和应用划分-2026-2032年全球市场预测腌製和滚揉设备市场:按类型、技术、产能、应用和最终用户划分-2026-2032年全球预测谷物加工设备市场:按设备类型、谷物类型、最终用途、製程、加工能力、技术和分销管道划分-全球预测,2026-2032年食品加工机械市场:按设备类型、自动化程度、运作模式、产能范围、动力来源和最终用途产业分類的全球预测,2026-2032年食品加工机械设备市场:依机器类型、操作方式、技术、应用、最终用户和分销管道划分,全球预测,2026-2032年