|

市场调查报告书

商品编码

1936582

PNT市场机会强劲、成长要素、产业趋势分析及2026年至2035年预测Assured PNT (Positioning, Navigation, and Timing) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

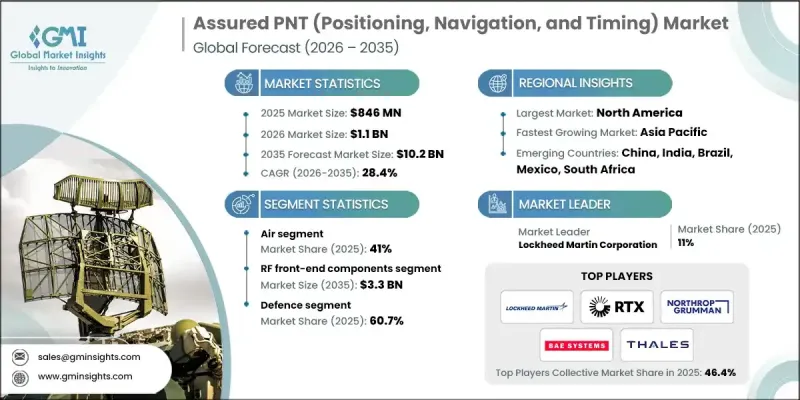

全球可靠的 PNT(定位、导航和授时)市场预计到 2025 年价值 8.46 亿美元,到 2035 年达到 102 亿美元,年复合成长率为 28.4%。

由于通讯、国防、能源和金融等高度依赖精度的产业对高可靠性的授时和定位解决方案的需求日益迫切,该市场正蓬勃发展。传统的基于GPS的系统面临干扰、欺骗和讯号中断等安全漏洞,因此部署可靠的PNT解决方案至关重要。这些系统整合了多种方法和冗余技术,即使某个资料来源发生故障,也能确保持续运作。产业正朝着更安全、更整合、多源的解决方案发展,这些解决方案结合了来自地球静止轨道、中地球轨道和低地球轨道(GEO)的GNSS星座、地面增强系统以及零信任安全框架。智慧城市、自动驾驶汽车和关键基础设施对GPS和GNSS的日益依赖,正在推动可靠PNT市场的演进。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 8.46亿美元 |

| 预测金额 | 102亿美元 |

| 复合年增长率 | 28.4% |

预计到2025年,航空业将占全球经济的41%。航空业越来越依赖可靠的PNT(定位、导航和时间)系统来确保飞行安全、实现自主运作并有效率地管理空中交通。先进的航空电子设备、感测器融合和导航系统即使在GPS讯号中断和空域拥挤的情况下也能确保精确定位。

到2025年,国防领域将占据60.7%的市场。在GPS讯号不可用或受干扰的环境下,强大的定位、导航和授时(PNT)系统对于任务执行至关重要。军事应用涵盖陆地、空中和海上平台,重点在于抗电子战能力、安全导航和战术性协调。

2025 年,欧洲可靠的 PNT(定位、导航和时间)市值将达到 2.167 亿美元。区域成长的驱动力包括 GNSS 弹性计画、多星座整合、地面增强系统以及国防、交通和关键基础设施领域的公私合营。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 紧急服务、军事和航太等领域对可靠资讯的需求日益增长

- 不断扩展的国防和安全应用需要可靠的导航

- GPS 安全性的日益下降凸显了开发高效定位、导航和授时 (PNT) 系统的必要性。

- 多源和混合PNT技术的应用日益广泛

- 产业潜在风险与挑战

- 高额的开发和培训成本

- 缺乏适当的规章制度和标准

- 市场机会

- 透过将可靠的定位导航与授时系统整合到自动驾驶车辆和无人机中来提高导航性能

- 海事和航空领域的成长需要强大的导航解决方案。

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 国防预算分析

- 全球国防费用趋势

- 区域国防预算分配

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 主要国防现代化项目

- 预算预测(2025-2034 年)

- 对产业成长的影响

- 各国国防预算

- 按部门分類的国防预算分配

- 人员

- 运作/维护

- 采购

- 研究与发展、测试与评估

- 基础设施和建筑

- 技术与创新

- 供应链韧性

- 地缘政治分析

- 劳动力分析

- 数位转型

- 併购和策略联盟

- 风险评估与管理

- 主要合约授予情况(2022-2025 年)

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 区域比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年主要发展动态

- 併购

- 合作伙伴关係和合资企业

- 技术进步

- 扩张与投资策略

- 数位转型计划

- 新兴/Start-Ups竞赛的趋势

第五章 2022-2035年各零件市场估算与预测

- 时序组件

- 手錶

- 频率标准/振盪器

- 射频前端组件

- 天线

- 功率放大器

- 应答器

- 讯号处理组件

- 接收器(支援GNSS、多卫星群、认证)

- 抗干扰/抗欺骗模组

- 惯性感测器和环境感测器

- 加速计

- 陀螺仪

- 磁力计

- 支援和整合组件

- 控制电子设备

- 软体定义PNT模组

- 介面和机壳

第六章 2022-2035年各平台市场估算与预测

- 飞机

- 军用机

- 战斗机

- 特种任务飞机

- 军用直升机

- 无人系统

- 军用机

- 土地

- 战斗车辆

- 主战坦克

- 装甲运兵车

- 装甲两栖车辆

- 其他的

- 无人地面车辆

- 战斗车辆

- 其他的

- 海军

- 驱逐舰

- 护卫舰

- 克尔维特

- 潜水艇

7. 依最终用途分類的市场估计与预测,2022-2035 年

- 防御

- 国防安全保障

第八章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第九章:公司简介

- 主要企业

- BAE Systems plc

- Lockheed Martin

- Northrop Grumman

- Raytheon Technologies

- 按地区分類的主要企业

- 北美洲

- General Dynamics

- Honeywell International

- Leidos

- 欧洲

- Leonardo

- Thales Group

- Hexagon AB

- 亚太地区

- Israel Aerospace Industries

- Collins Aerospace(RTX)

- KVH Industries

- 北美洲

- 小众玩家/干扰者

- Advanced Navigation

- Aevex Aerospace

- Bliley Technologies

- Curtiss-Wright

- Hemisphere GNSS

- SBG Systems

- Septentrio NV

The Global Assured PNT (Positioning, Navigation, and Timing) Market was valued at USD 846 million in 2025 and is estimated to grow at a CAGR of 28.4% to reach USD 10.2 billion by 2035.

The market is gaining momentum due to the critical need for resilient timing and positioning solutions across industries that rely heavily on precision, including telecommunications, defense, energy, and finance. Traditional GPS-based systems face vulnerabilities such as jamming, spoofing, and signal interruptions, making the adoption of Assured PNT solutions essential. These systems integrate multiple methods and redundant technologies to ensure continuous operation even if one source fails. The industry is moving toward more secure, integrated, and multi-source solutions, combining GEO, MEO, and LEO GNSS constellations, ground-based augmentation, and zero-trust security frameworks. Rising reliance on GPS and GNSS for smart cities, autonomous vehicles, and critical infrastructure is driving the evolution of the assured PNT market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $846 Million |

| Forecast Value | $10.2 Billion |

| CAGR | 28.4% |

The air segment held a 41% share in 2025, as aviation increasingly depends on assured PNT to maintain flight safety, enable autonomous operations, and manage air traffic efficiently. Advanced avionics, sensor fusion, and navigation systems ensure accurate positioning even during GPS outages or in congested airspace.

The defense segment accounted for 60.7% share in 2025. Assured PNT is critical for mission-focused operations in GPS-denied or jammed environments. Military applications span ground, air, and maritime platforms, focusing on electronic warfare resilience, secure navigation, and tactical coordination.

Europe Assured PNT (Positioning, Navigation, and Timing) Market was valued at USD 216.7 million in 2025. Regional growth is driven by GNSS resilience programs, multi-constellation integration, land-based augmentation systems, and public-private partnerships in defense, transportation, and critical infrastructure sectors.

Key players in the Global Assured PNT (Positioning, Navigation, and Timing) Market include Advanced Navigation, Aevex Aerospace, BAE Systems plc, Bliley Technologies, Curtiss-Wright, General Dynamics, Hemisphere GNSS, Hexagon AB, Honeywell International, Israel Aerospace Industries, KVH Industries, Leidos, Leonardo, Lockheed Martin, and Northrop Grumman. Companies in the Assured PNT (Positioning, Navigation, and Timing) Market are focusing on strengthening their presence through continuous innovation and product development, particularly in multi-source and resilient navigation technologies. Strategic collaborations and partnerships allow firms to expand market reach and integrate complementary solutions. Investments in cybersecurity and zero-trust models enhance product reliability and regulatory compliance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Component trends

- 2.2.2 Platform trends

- 2.2.3 End use trends

- 2.2.4 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in demand for reliable information in applications such as emergency services, military, and aerospace

- 3.2.1.2 Expansion of defense and security applications requiring reliable navigation

- 3.2.1.3 Growing vulnerabilities of GPS highlighting the need for assured PNT Systems

- 3.2.1.4 Rising adoption of multi-source and hybrid PNT technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and training cost

- 3.2.2.2 Lack of proper regulations and standard

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of assured PNT with autonomous vehicles and drones for enhanced navigation

- 3.2.3.2 Growth in maritime and aviation sectors requiring resilient navigation solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Defense budget analysis

- 3.11 Global defense spending trends

- 3.12 Regional defense budget allocation

- 3.12.1 North America

- 3.12.2 Europe

- 3.12.3 Asia Pacific

- 3.12.4 Middle East and Africa

- 3.12.5 Latin America

- 3.13 Key defense modernization programs

- 3.14 Budget forecast (2025-2034)

- 3.14.1 Impact on industry growth

- 3.14.2 Defense budgets by country

- 3.14.3 Defense budget allocation by segment

- 3.14.3.1 Personnel

- 3.14.3.2 Operations and maintenance

- 3.14.3.3 Procurement

- 3.14.3.4 Research, development, test and evaluation

- 3.14.3.5 Infrastructure and construction

- 3.14.3.6 Technology and innovation

- 3.15 Supply chain resilience

- 3.16 Geopolitical analysis

- 3.17 Workforce analysis

- 3.18 Digital transformation

- 3.19 Mergers, acquisitions, and strategic partnerships landscape

- 3.20 Risk assessment and management

- 3.21 Major contract awards (2022-2025)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Components, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Timing components

- 5.2.1 Atomic clocks

- 5.2.2 Frequency standards / oscillators

- 5.3 Rf front-end components

- 5.3.1 Antennas

- 5.3.2 Power amplifiers

- 5.3.3 Transponders

- 5.4 Signal Processing Components

- 5.4.1 Receivers (GNSS, multi-constellation, authenticated)

- 5.4.2 Anti-jam / anti-spoof modules

- 5.5 Inertial & environmental sensors

- 5.5.1 Accelerometers

- 5.5.2 Gyroscopes

- 5.5.3 Magnetometers

- 5.6 Supporting & integration components

- 5.6.1 Control electronics

- 5.6.2 Software-defined PNT modules

- 5.6.3 Interfaces & enclosures

Chapter 6 Market Estimates and Forecast, By Platform, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Air

- 6.2.1 Military aircraft

- 6.2.1.1 Fighter aircraft

- 6.2.1.2 Special mission aircraft

- 6.2.2 Military helicopters

- 6.2.3 Unmanned systems

- 6.2.1 Military aircraft

- 6.3 Land

- 6.3.1 Combat vehicles

- 6.3.1.1 Main battle tanks

- 6.3.1.2 Armored personnel carriers

- 6.3.1.3 Armored amphibious vehicles

- 6.3.1.4 Others

- 6.3.2 Unmanned ground vehicles

- 6.3.1 Combat vehicles

- 6.4 Others

- 6.4.1 Naval

- 6.4.2 Destroyers

- 6.4.3 Frigates

- 6.4.4 Corvettes

- 6.4.5 Submarines

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Defense

- 7.3 Homeland security

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 BAE Systems plc

- 9.1.2 Lockheed Martin

- 9.1.3 Northrop Grumman

- 9.1.4 Raytheon Technologies

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 General Dynamics

- 9.2.1.2 Honeywell International

- 9.2.1.3 Leidos

- 9.2.2 Europe

- 9.2.2.1 Leonardo

- 9.2.2.2 Thales Group

- 9.2.2.3 Hexagon AB

- 9.2.3 APAC

- 9.2.3.1 Israel Aerospace Industries

- 9.2.3.2 Collins Aerospace (RTX)

- 9.2.3.3 KVH Industries

- 9.2.1 North America

- 9.3 Niche Players / Disruptors

- 9.3.1 Advanced Navigation

- 9.3.2 Aevex Aerospace

- 9.3.3 Bliley Technologies

- 9.3.4 Curtiss-Wright

- 9.3.5 Hemisphere GNSS

- 9.3.6 SBG Systems

- 9.3.7 Septentrio N.V.

APNT(可靠定位、导航和授时)市场:按技术、组件类型和应用划分 - 2026-2032年全球市场预测

APNT(可靠定位、导航和授时)市场:按技术、组件类型和应用划分 - 2026-2032年全球市场预测 2026年全球A-PNT(可靠定位、导航和授时)市场报告2026年全球卫星定位、导航与授时(PNT)技术市场报告2026年全球弹性定位、导航与授时(PNT)地面站市场报告全球导航卫星系统(GNSS)独立定位、导航和授卫星群(PNT)星座市场报告(2026年)卫星定位、导航和时间同步技术市场:按技术、组件、应用、服务和最终用户划分-2026-2032年全球市场预测2026年全球定位、导航与授时(PNT)解决方案市场报告

2026年全球A-PNT(可靠定位、导航和授时)市场报告2026年全球卫星定位、导航与授时(PNT)技术市场报告2026年全球弹性定位、导航与授时(PNT)地面站市场报告全球导航卫星系统(GNSS)独立定位、导航和授卫星群(PNT)星座市场报告(2026年)卫星定位、导航和时间同步技术市场:按技术、组件、应用、服务和最终用户划分-2026-2032年全球市场预测2026年全球定位、导航与授时(PNT)解决方案市场报告 低地球轨道定位、导航和授时 (LEO PNT) 市场:依服务类型、频段和最终用途划分 - 全球预测至 2036 年

低地球轨道定位、导航和授时 (LEO PNT) 市场:依服务类型、频段和最终用途划分 - 全球预测至 2036 年 PNT市场权威分析-全球产业规模、份额、趋势、机会与预测:按平台、最终用户、地区和竞争对手划分,2021-2031年SLAM导航解决方案市场按组件、类型、应用、最终用户和部署模式划分,全球预测(2026-2032)

PNT市场权威分析-全球产业规模、份额、趋势、机会与预测:按平台、最终用户、地区和竞争对手划分,2021-2031年SLAM导航解决方案市场按组件、类型、应用、最终用户和部署模式划分,全球预测(2026-2032)