|

市场调查报告书

商品编码

1936593

牙科旅游市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Dental Tourism Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

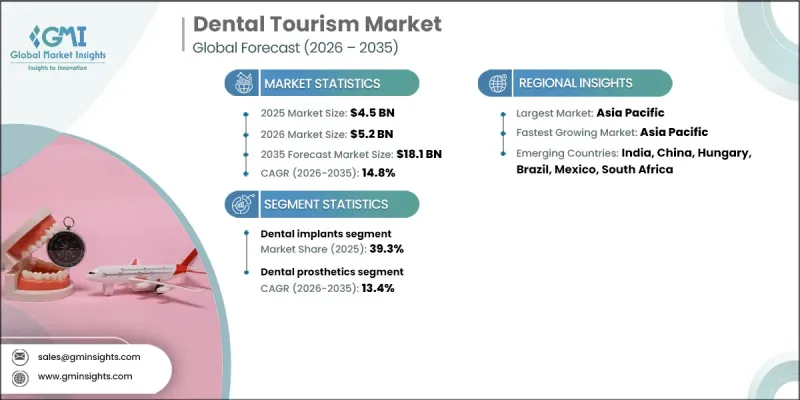

全球牙科旅游市场预计到 2025 年将达到 45 亿美元,并以 14.8% 的复合年增长率成长,到 2035 年达到 181 亿美元。

已开发国家牙科费用的上涨、海外优质牙科服务的普及以及对美容牙科和先进牙科手术需求的不断增长,共同推动了牙科旅游市场的强劲增长。牙科旅游是指患者为了节省费用、缩短等待时间或获得更先进的治疗方案,而前往国内或国外接受牙科治疗。全球互联互通的改善、旅行政策的放宽以及结构化的医疗旅游框架的建立,都为市场发展带来了积极影响,简化了患者协调和治疗的连续性。数位化咨询和虚拟治疗计划的引入,使得病人参与。这种数位化增强了患者的决策信心,并简化了治疗计画。此外,医疗服务提供者正日益将牙科服务与更广泛的健康旅游体验相结合,提升了牙科旅游的整体吸引力,并有望在2025年后持续推动市场成长。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 45亿美元 |

| 预测金额 | 181亿美元 |

| 复合年增长率 | 14.8% |

预计到2025年,人工植牙市场份额将达到39.3%,主要受牙齿脱落率上升和对耐用修復方案需求成长的推动。植入技术的不断进步和持续的高治疗成功率是推动该细分市场成长的主要动力。已开发地区植入手术高成本,使得海外治疗成为一个颇具吸引力的选择,患者可以从降低总体成本且保证临床品质的套餐计划中获益。这种成本效益仍然是植入市场需求成长的关键驱动因素。

预计到2025年,牙科诊所市占率将达到72.6%,到2035年将达到138亿美元。牙科诊所因其能够以具有竞争力的价格提供专业治疗,仍然是首选的治疗场所。来自高成本地区的患者数量不断增加,提高了诊所的使用率和收入潜力,使牙科诊所成为牙科旅游生态系统中的关键服务提供者。

预计到2025年,美国牙医旅游市场规模将达到5.781亿美元。市场成长的主要驱动因素是国内牙科治疗费用高昂以及患者自付费用较高,这些因素促使人们选择出国就医。费用差异持续影响患者的决策,使得牙科旅游成为经济上颇具吸引力的选择。

目录

第一章调查方法

- 研究途径

- 品质保证

- GMI人工智慧政策与资料完整性承诺

- 资讯来源完整性通讯协定

- GMI人工智慧政策与资料完整性承诺

- 调查可追溯性和可靠性评分

- 勘测和步道组成部分

- 评分组成部分

- 数据收集

- 主要资讯的部分列表

- 资料探勘资讯来源

- 付费资讯来源

- 区域资讯来源

- 付费资讯来源

- 基本估计值与计算

- 两种方法的基准年计算均适用。

- 预测模型

- 量化市场影响分析

- 生长参数对预测值的数学影响

- 量化市场影响分析

- 研究透明度附录

- 资讯来源归属框架

- 品质保证指标

- 对信任的承诺

第二章执行摘要

第三章业界考察

- 生态系分析

- 产业影响因素

- 司机

- 牙科疾病呈上升趋势

- 无保险或保险不足的患者人数不断增加

- 牙科治疗技术的进步

- 人们对牙科旅游选择的认识不断提高

- 产业潜在风险与挑战

- 牙科旅游的高昂费用

- 全球牙科法规缺乏统一标准。

- 市场机会

- 扩大远距牙科和线上咨询

- 个人化和美容牙科治疗的增长

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 科技趋势

- 当前技术趋势

- 新兴技术

- 医疗保险覆盖范围

- 未来市场趋势

- 波特五力分析

- PESTEL 分析

- 客户洞察

- 投资环境

- 差距分析

第四章 竞争情势

- 介绍

- 企业矩阵分析

- 竞争定位矩阵

- 主要市场公司的竞争分析

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 按服务分類的市场估算与预测,2022-2035年

- 人工植牙

- 正畸

- 美容牙科治疗

- 牙科修补

- 其他服务

6. 依最终用途分類的市场估计与预测,2022-2035 年

- 牙医诊所

- 医院

- 其他最终用户

第七章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 比利时

- 波兰

- 匈牙利

- 捷克共和国

- 土耳其

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第八章:公司简介

- ACIBADEM Healthcare Group

- Apollo Hospitals

- Bumrungrad International Hospital

- Cancun Dental Specialists

- DentAkademi

- Fortis Healthcare

- Fulop Clinic

- KPJ Healthcare Berhad

- Kreativ Dental Clinic

- Manipal Hospitals

- Max Healthcare

- Mount Elizabeth Medical Centre

- Raffles Medical Group

- Thonglor Dental Hospital(TDH)

- Vera Smile

The Global Dental Tourism Market was valued at USD 4.5 billion in 2025 and is estimated to grow at a CAGR of 14.8% to reach USD 18.1 billion by 2035.

Strong market growth is driven by rising dental treatment costs in developed economies, increasing access to high-quality dental services abroad, and growing demand for cosmetic and advanced dental procedures. Dental tourism involves patients traveling domestically or internationally to receive dental care that offers cost advantages, reduced waiting periods, or access to advanced treatment options. The market benefits from improved global connectivity, favorable travel policies, and the development of structured healthcare tourism frameworks that simplify patient coordination and care continuity. The integration of digital consultations and virtual treatment planning has transformed patient engagement by enabling early assessment and transparent cost evaluation before travel. This digital shift improves decision confidence and streamlines planning. Additionally, providers are increasingly aligning dental services with broader wellness-focused travel experiences, which enhances the overall appeal of dental tourism and supports sustained market momentum beyond 2025.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.5 Billion |

| Forecast Value | $18.1 Billion |

| CAGR | 14.8% |

The dental implants segment held a 39.3% share in 2025, supported by the rising incidence of tooth loss and growing preference for durable restorative solutions. Continued advancements in implant technology and consistently high treatment success rates are reinforcing segment growth. The high cost of implant procedures in developed regions makes overseas treatment an attractive alternative, as patients benefit from bundled offerings that reduce overall expenses while maintaining clinical quality. This cost efficiency remains a key driver of demand within the implants segment.

The dental clinics segment held a 72.6% share in 2025 and is expected to reach USD 13.8 billion by 2035. Clinics remain the preferred care setting due to their ability to deliver specialized treatments at competitive prices. Rising patient inflows from high-cost regions are increasing utilization rates and revenue potential, positioning clinics as the primary service providers within the dental tourism ecosystem.

U.S. Dental Tourism Market reached USD 578.1 million in 2025. Market expansion is influenced by high domestic dental costs and significant out-of-pocket expenses, which encourage outbound travel for treatment. Cost disparities continue to shape patient decision-making, making dental tourism a financially attractive alternative.

Key companies operating in the Global Dental Tourism Market include Apollo Hospitals, ACIBADEM Healthcare Group, Fortis Healthcare, Raffles Medical Group, Manipal Hospitals, Max Healthcare, Bumrungrad International Hospital, KPJ Healthcare Berhad, Mount Elizabeth Medical Centre, Fulop Clinic, DentAkademi, Kreativ Dental Clinic, Thonglor Dental Hospital, Vera Smile, and Cancun Dental Specialists. Companies in the dental tourism market are strengthening their competitive position through service integration, digital engagement, and international partnerships. Leading providers are investing in virtual consultation platforms, multilingual patient support, and coordinated care models to improve accessibility and trust. Strategic alliances with travel facilitators and insurers help streamline patient journeys. Many operators are expanding treatment portfolios and enhancing accreditation standards to reinforce quality perception. Geographic expansion, targeted marketing, and bundled pricing strategies further enable companies to attract international patients and build long-term market presence.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Service trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of dental diseases

- 3.2.1.2 Rising number of uninsured or underinsured patients

- 3.2.1.3 Advancements in dental treatment technologies

- 3.2.1.4 Growing awareness of dental tourism options

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with dental tourism

- 3.2.2.2 Lack of standardized global dental care regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of tele-dentistry and virtual consultations

- 3.2.3.2 Growth in personalized and cosmetic dental treatments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Medical coverage scenario

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Customer insights

- 3.11 Investment landscape

- 3.12 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive positioning matrix

- 4.4 Competitive analysis of major market players

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Service, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Dental implants

- 5.3 Orthodontics

- 5.4 Dental cosmetics

- 5.5 Dental prosthetics

- 5.6 Other services

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Dental clinics

- 6.3 Hospitals

- 6.4 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Belgium

- 7.3.6 Poland

- 7.3.7 Hungary

- 7.3.8 Czech Republic

- 7.3.9 Turkey

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 ACIBADEM Healthcare Group

- 8.2 Apollo Hospitals

- 8.3 Bumrungrad International Hospital

- 8.4 Cancun Dental Specialists

- 8.5 DentAkademi

- 8.6 Fortis Healthcare

- 8.7 Fulop Clinic

- 8.8 KPJ Healthcare Berhad

- 8.9 Kreativ Dental Clinic

- 8.10 Manipal Hospitals

- 8.11 Max Healthcare

- 8.12 Mount Elizabeth Medical Centre

- 8.13 Raffles Medical Group

- 8.14 Thonglor Dental Hospital (TDH)

- 8.15 Vera Smile