|

市场调查报告书

商品编码

1936599

肝癌药物市场机会、成长要素、产业趋势分析及2026年至2035年预测Liver Cancer Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

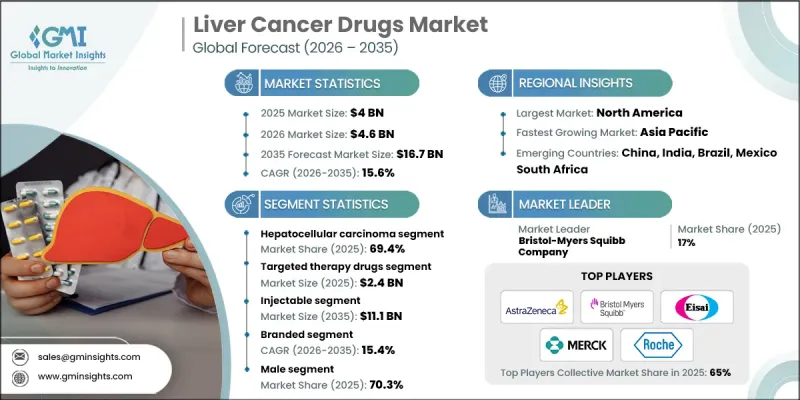

全球肝癌治疗市场预计到 2025 年将达到 40 亿美元,到 2035 年将达到 167 亿美元,年复合成长率为 15.6%。

全球原发性肝癌发病率不断上升,以及因诊断延迟和根治性选择有限而导致的高死亡率,推动了市场成长。肝癌仍然是最致命的肿瘤疾病之一,因此迫切需要有效的药物疗法来延长存活期并延缓疾病进展。肝癌治疗市场涵盖用于治疗肝臟恶性肿瘤的药物的研发、生产和商业化,包括旨在改善治疗效果和生活品质的疗法。药物研发的重点正日益转向标靶治疗、免疫疗法、生物製药和化疗方案。由于许多患者在确诊时已处于晚期,全身性治疗在疾病管理中发挥关键作用。强大的肿瘤学研发管线、支持性的法规结构以及不断扩大的医保覆盖范围,持续促进创新并加速病患获得治疗。随着精准医疗和联合治疗策略的兴起,对肝癌治疗的製药投资不断增加,为市场的持续长期成长奠定了基础。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 40亿美元 |

| 预测金额 | 167亿美元 |

| 复合年增长率 | 15.6% |

2025年,肝细胞癌细分市场占据了69.4%的市场份额,预计到2035年将以15.5%的复合年增长率成长。这一主导地位反映了该癌症类型在全球范围内的高发病率以及治疗方法(包括联合治疗和免疫疗法)的不断进步。基础肝病的持续高发生率也持续支撑着对有效治疗方案的强劲需求。

预计到2025年,注射剂市场规模将达到27亿美元,到2035年将成长至111亿美元。注射剂製剂广泛应用于高级医疗机构,因为它们非常适合需要严格控制给药和临床监测的免疫疗法和生物製药。注射剂在一线疗法和联合治疗中的既定地位进一步巩固了其市场主导地位。

预计到2025年,北美肝癌治疗市场将占据41.1%的市场。这一区域主导地位得益于健全的监管体系、先进的诊断基础设施、创新治疗方法的早期应用以及完善的临床研究生态系统。有利的医保报销政策以及对早期检测和治疗优化的日益重视,将继续推动市场需求。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 产业影响因素

- 司机

- 全球肝癌发生率不断上升

- 转向标靶治疗和免疫肿瘤疗法

- 老龄人口的增加

- 医疗保健成本不断上涨以及对肿瘤学的关注

- 产业潜在风险与挑战

- 高昂的治疗费用和报销限制

- 诊断延迟会限制治疗合格。

- 市场机会

- 下一代联合治疗治疗和个人化治疗

- 新兴和高负担地区的成长潜力

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 各地区肝癌统计数据

- 未来市场趋势

- 管道分析

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 世界

- 北美洲

- 欧洲

- 亚太地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 按类型分類的市场估算与预测,2022-2035年

- 肝细胞癌

- 胆管癌

- 肝母细胞瘤

- 肝转移

- 其他类型

6. 2022-2035年按药物类别分類的市场估算与预测

- 化疗药物

- 标靶治疗药物

- 免疫疗法

7. 依行政途径分類的市场估计与预测,2022-2035 年

- 口服

- 注射

8. 按药物类型分類的市场估计和预测,2022-2035 年

- 学名药

- 品牌产品

第九章 依性别分類的市场估计与预测,2022-2035年

- 男性

- 女士

第十章 依最终用途分類的市场估计与预测,2022-2035年

- 医院

- 专科癌症中心

- 研究和学术机构

第十一章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- AbbVie

- Amgen

- AstraZeneca

- Bayer

- Bristol-Myers Squibb Company

- Eisai

- Exelixis

- F. Hoffmann-La Roche

- Glenmark Pharmaceuticals

- Johnson &Johnson

- Merck &Co.

- Regeneron Pharmaceuticals

- Sanofi

- Servier Pharmaceuticals

- Taiho Pharmaceutical

The Global Liver Cancer Drugs Market was valued at USD 4 billion in 2025 and is estimated to grow at a CAGR of 15.6% to reach USD 16.7 billion by 2035.

Market growth is driven by the rising incidence of primary liver cancers worldwide and the persistently high mortality rates associated with delayed diagnosis and limited curative treatment options. Liver cancer remains one of the most fatal oncology indications, creating an urgent need for effective drug-based therapies that can extend survival and slow disease progression. The liver cancer drugs market encompasses the research, production, and commercialization of pharmaceutical treatments used to manage liver malignancies, including therapies designed to improve outcomes and quality of life. Drug innovation is increasingly focused on targeted agents, immunotherapies, biologics, and chemotherapy-based regimens. Because many patients are diagnosed at advanced stages, systemic therapies play a critical role in disease management. Strong oncology research pipelines, supportive regulatory frameworks, and expanding reimbursement coverage continue to encourage innovation and accelerate patient access. As precision medicine and combination treatment strategies gain traction, pharmaceutical investment in liver cancer therapeutics is intensifying, positioning the market for sustained long-term expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4 Billion |

| Forecast Value | $16.7 Billion |

| CAGR | 15.6% |

The hepatocellular carcinoma segment accounted for 69.4% share in 2025 and is expected to grow at a CAGR of 15.5% throughout 2035. This dominance reflects the high global burden of this cancer type and continued advancements in treatment approaches, including combination therapies and immune-based drugs. Ongoing prevalence of underlying liver conditions continues to support strong demand for effective therapeutic options.

The injectable segment generated USD 2.7 billion in 2025 and is projected to grow to USD 11.1 billion by 2035. Injectable formulations are widely used in advanced treatment settings due to their suitability for immunotherapies and biologics, which require controlled administration and clinical supervision. Their established role in first line and combination regimens further supports segment leadership.

North America Liver Cancer Drugs Market held 41.1% share in 2025. Regional dominance is supported by strong regulatory pathways, advanced diagnostic infrastructure, early adoption of innovative therapies, and a well-developed clinical research ecosystem. Favorable reimbursement policies and increasing focus on early detection and treatment optimization continue to drive demand.

Key companies operating in the Global Liver Cancer Drugs Market include Merck & Co., F. Hoffmann-La Roche, AstraZeneca, Bayer, Bristol-Myers Squibb Company, Regeneron Pharmaceuticals, Johnson & Johnson, Eisai, Exelixis, Sanofi, Amgen, AbbVie, Taiho Pharmaceutical, Servier Pharmaceuticals, and Glenmark Pharmaceuticals. Companies in the liver cancer drugs market are strengthening their competitive position through aggressive research and development initiatives focused on novel drug targets and combination therapies. Many players are expanding immuno-oncology portfolios and investing in precision medicine to improve treatment response rates. Strategic collaborations with research institutions and biotechnology firms are accelerating clinical development timelines. Companies are also prioritizing regulatory approvals across multiple regions to expand market access. Lifecycle management strategies, including label expansions and next-generation formulations, are being used to extend product value.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Drug class trends

- 2.2.4 Route of administration trends

- 2.2.5 Medication type trends

- 2.2.6 Gender trends

- 2.2.7 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global incidence of liver cancer

- 3.2.1.2 Shift toward targeted and immuno-oncology therapies

- 3.2.1.3 Expanding geriatric population

- 3.2.1.4 Rising healthcare expenditure and oncology focus

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs and reimbursement constraints

- 3.2.2.2 Late diagnosis limiting treatment eligibility

- 3.2.3 Market opportunities

- 3.2.3.1 Next-generation combination and personalized therapies

- 3.2.3.2 Growth potential in emerging, high-burden regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Liver cancer statistics, by region

- 3.6 Future market trends

- 3.7 Pipeline analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Hepatocellular carcinoma

- 5.3 Cholangiocarcinoma

- 5.4 Hepatoblastoma

- 5.5 Liver metastasis

- 5.6 Other types

Chapter 6 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Chemotherapeutic agents

- 6.3 Targeted therapy drugs

- 6.4 Immunotherapy drugs

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

Chapter 8 Market Estimates and Forecast, By Medication Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Generic

- 8.3 Branded

Chapter 9 Market Estimates and Forecast, By Gender, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Male

- 9.3 Female

Chapter 10 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Hospitals

- 10.3 Specialty cancer centers

- 10.4 Research and academic centers

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AbbVie

- 12.2 Amgen

- 12.3 AstraZeneca

- 12.4 Bayer

- 12.5 Bristol-Myers Squibb Company

- 12.6 Eisai

- 12.7 Exelixis

- 12.8 F. Hoffmann-La Roche

- 12.9 Glenmark Pharmaceuticals

- 12.10 Johnson & Johnson

- 12.11 Merck & Co.

- 12.12 Regeneron Pharmaceuticals

- 12.13 Sanofi

- 12.14 Servier Pharmaceuticals

- 12.15 Taiho Pharmaceutical

肝癌治疗市场:2026-2032年全球市场预测(依治疗方法、癌症类型、给药途径、药物类别、最终用户和分销管道划分)

肝癌治疗市场:2026-2032年全球市场预测(依治疗方法、癌症类型、给药途径、药物类别、最终用户和分销管道划分) 肝癌药物市场-全球产业规模、份额、趋势、机会及预测(依癌症类型、器材、年龄、病因、给药途径、通路、地区及竞争格局划分,2021-2031年)急性高氨血症治疗市场(依药物类型、适应症、给药途径及通路划分)-2026-2032年全球预测肝转移治疗市场依给药途径、产品类型、治疗类型、治疗线、原发肿瘤类型、最终用户和分销管道划分,全球预测,2026-2032年

肝癌药物市场-全球产业规模、份额、趋势、机会及预测(依癌症类型、器材、年龄、病因、给药途径、通路、地区及竞争格局划分,2021-2031年)急性高氨血症治疗市场(依药物类型、适应症、给药途径及通路划分)-2026-2032年全球预测肝转移治疗市场依给药途径、产品类型、治疗类型、治疗线、原发肿瘤类型、最终用户和分销管道划分,全球预测,2026-2032年 肝癌药物市场规模、份额和成长分析(按药物、类型、通路和地区划分)-2026-2033年产业预测

肝癌药物市场规模、份额和成长分析(按药物、类型、通路和地区划分)-2026-2033年产业预测 2026 年至 2032 年肝癌治疗市场(按流程、类型、最终用户和地区划分)

2026 年至 2032 年肝癌治疗市场(按流程、类型、最终用户和地区划分) 肝癌药物市场规模、份额、趋势分析报告:按治疗、类型、分销管道、地区分類的细分趋势,2025-2030 年

肝癌药物市场规模、份额、趋势分析报告:按治疗、类型、分销管道、地区分類的细分趋势,2025-2030 年 肝癌药物市场,按药物类别、治疗类型、给药途径、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

肝癌药物市场,按药物类别、治疗类型、给药途径、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 肝转移治疗市场 - 按药物类别(标靶治疗、化疗、免疫治疗)、原发性癌症(结直肠癌、乳癌、肺癌)、配销通路(医院药房、专业药房)、全球预测(2024 - 2032 )

肝转移治疗市场 - 按药物类别(标靶治疗、化疗、免疫治疗)、原发性癌症(结直肠癌、乳癌、肺癌)、配销通路(医院药房、专业药房)、全球预测(2024 - 2032 )