|

市场调查报告书

商品编码

1936607

汽车高阶轮胎市场机会、成长要素、产业趋势分析及2026年至2035年预测Automotive Premium Tires Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

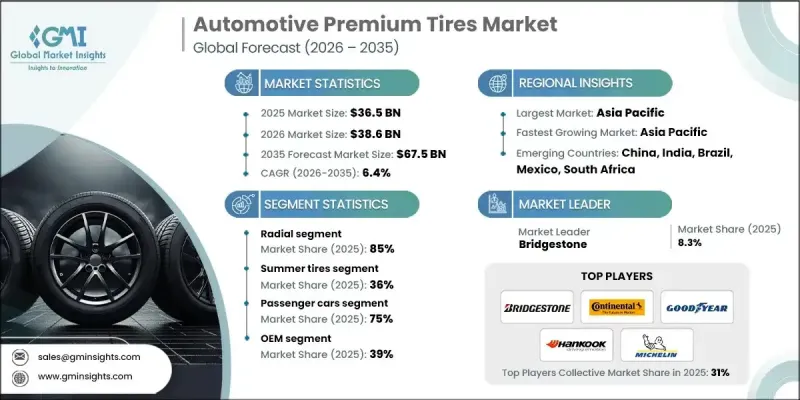

全球高阶汽车轮胎市场预计到 2025 年将达到 365 亿美元,到 2035 年将达到 675 亿美元,年复合成长率为 6.4%。

这一成长主要得益于高端乘用车和多用途车销量的提升,以及整车製造商对抓地力强、高速稳定性好、驾驶舒适性佳的轮胎需求不断增长。汽车製造商如今将高端轮胎定位为车辆整体性能的重要组成部分,这不仅维持了基准需求,也支撑了长期高价值的供应协议。消费者越来越关注煞车效率、湿地抓地力、低噪音和高速稳定性。高端轮胎凭藉先进的胎面花纹和工程橡胶配方满足了这些期望,促使消费者升级原厂轮胎并接受更高的更换成本。这一趋势正在增强整车製造商和售后市场的需求,使高端轮胎从可选项转变为以价值主导的细分市场。在北美和欧洲,老旧车队支撑着稳定的轮胎更换需求。豪华车车主越来越多地选择性能达到或超过原厂规格的替换轮胎,这推动了售后市场收入的成长,并稳定了成熟汽车市场对高性能轮胎解决方案的需求。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 365亿美元 |

| 预测金额 | 675亿美元 |

| 复合年增长率 | 6.4% |

到2025年,子午线轮胎市占率将达到85%,预计2026年至2035年将以6.9%的复合年增长率成长,这主要得益于操控精准、耐用性和低滚动阻力等优势。随着燃油效率和乘坐舒适性成为关键设计考量因素,汽车製造商(OEM)正持续将子午线轮胎作为高端和高性能车型的标准配备。

预计到 2025 年,夏季轮胎市占率将达到 36%,到 2035 年将以 5.1% 的复合年增长率成长。这些轮胎专为温暖气候设计,优先考虑高速行驶时的牵引力、转向响应和稳定性,从而提供与高端车辆定位相符的精緻驾驶体验。

预计到2025年,美国高阶汽车轮胎市场规模将达到81.8亿美元。随着国内市场向电动车和大型车辆转型,对低滚动阻力、高承载能力和有效降噪的高端轮胎的需求日益增长。消费者越来越重视轮胎的胎面寿命、能源效率和全路况性能,这促使製造商在原厂配套和替换市场通路拓展其高端特种轮胎产品线。

目录

第一章调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 对豪华和高性能汽车的需求不断增长

- 注重安全性、舒适性和操控性。

- 已开发市场汽车拥有量不断成长

- OEM高阶定位

- 产业潜在风险与挑战

- 价格敏感度高限制了成本敏感型市场中的采用率。

- 原物料价格波动对利润率的影响

- 市场机会

- 新兴经济体高端汽车销售不断成长

- 电动车轮胎的需求趋势

- 售后市场的客製化需求

- 智慧永续轮胎

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 美国运输部(DOT) 标准

- 职业安全与健康管理局 (OSHA) 指南

- 美国环保署(EPA)

- 欧洲

- EN ISO轮胎标准

- 欧盟海关和安全法规

- BS EN/CEN 标准

- 国家标准(UNE、DIN等)

- 亚太地区

- 中国国家标准(GB标准)

- 日本JIS标准要求

- 韩国KS认证

- 印度BIS标准

- 泰国工业标准协会(TISI)

- 拉丁美洲

- INMETRO(国家计量研究院)

- INTI认证(国家技术研究院)

- NOM 标准(墨西哥官方标准)

- 中东和非洲

- ESMA/阿联酋合格评定计划 (ECAS)

- 海湾合作委员会技术法规

- SABS认证

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 定价分析

- 产品定价

- 区域定价

- 生产统计

- 生产基地

- 消费基础

- 出口和进口

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 电动车专用轮胎的经济性和设计性权衡

- 滚动阻力和耐用性之间的权衡

- 吸音泡沫的成本溢价

- 对平均售价和利润率的影响

- 电动车和内燃机汽车之间的替代经济模式

- 原物料风险和成本敏感度分析

- 通路层面利润与定价分析

- 消费行为及高级会员采纳分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 依轮胎类型分類的市场估计与预测,2022-2035年

- 夏季轮胎

- 冬季轮胎

- 全天候轮胎

- 全地形轮胎

- 其他的

第六章 依轮胎结构分類的市场估计与预测,2022-2035年

- 子午线轮胎

- 偏见

第七章 依车辆类型分類的市场估计与预测,2022-2035年

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型商用车

- 中型商用车(MCV)

- 重型商用车(HCV)

第八章 按轮圈尺寸分類的市场估算与预测,2022-2035年

- 小于15英寸

- 15到20英寸

- 20吋或以上

第九章 依技术分類的市场估计与预测,2022-2035年

- 防爆胎技术

- 自密封轮胎

- 环保轮胎

- 降噪技术

- 其他的

第十章 依销售管道分類的市场估计与预测,2022-2035年

- OEM

- 售后市场

第十一章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 俄罗斯

- 波兰

- 罗马尼亚

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ANZ

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- 世界公司

- Apollo Tyres

- Bridgestone

- Continental

- Cooper Tire &Rubber Company

- Goodyear Tire &Rubber Company

- Hankook Tire &Technology

- Kumho Tire

- Michelin

- Pirelli

- Sumitomo Rubber Industries

- Toyo Tire

- Yokohama Rubber Company

- 本地製造商

- CEAT

- Giti Tire

- JK Tyre &Industries

- Linglong Tire

- Maxxis International

- MRF Tyres

- Nexen Tire

- Nokian Tyres

- Sailun

- 新兴製造商

- Double Coin

- Laufenn

- Petlas

- Radar Tires

- Triangle Tyre

- ZC Rubber

The Global Automotive Premium Tires Market was valued at USD 36.5 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 67.5 billion by 2035.

Growth is strongly supported by rising sales of high-end passenger vehicles and utility vehicles, along with increasing OEM demand for tires that deliver superior grip, high-speed stability, and refined ride quality. Automakers now position premium tires as an integral part of overall vehicle performance, which sustains baseline demand and supports long-term, higher-value supply agreements. Consumers show heightened awareness of braking efficiency, traction on wet surfaces, reduced road noise, and stability at elevated speeds. Premium tires address these expectations through advanced tread patterns and engineered rubber blends, encouraging customers to upgrade from factory-fitted tires and accept higher replacement costs. This behavior strengthens both OEM and replacement demand and reinforces premium tires as a value-driven segment rather than a discretionary purchase. In North America and Europe, an aging vehicle fleet supports a consistent cycle of replacement tire demand. Owners of premium vehicles increasingly choose replacement tires that match or exceed original specifications, which drives aftermarket revenue growth and stabilizes demand for high-performance tire solutions across mature automotive markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $36.5 Billion |

| Forecast Value | $67.5 Billion |

| CAGR | 6.4% |

The radial tires segment held an 85% share in 2025 and is forecasted to grow at a CAGR of 6.9% from 2026 to 2035, supported by advantages in handling precision, durability, and reduced rolling resistance. OEMs continue to standardize radial tires across luxury and performance-focused models, particularly as efficiency and ride quality become critical design priorities.

The summer tire segment held a 36% share in 2025 and is expected to grow at a CAGR of 5.1% through 2035. These tires are engineered for warm-weather conditions and prioritize traction, steering response, and stability at higher speeds, delivering a refined driving experience that aligns with premium vehicle positioning.

US Automotive Premium Tires Market reached USD 8.18 billion in 2025. As the domestic market shifts toward electric vehicles and larger vehicle formats, demand is rising for premium tires that offer low rolling resistance, enhanced load capacity, and effective noise control. Buyers increasingly value tread life, energy efficiency, and all-condition performance, prompting manufacturers to expand specialized premium tire offerings across OEM and replacement channels.

Key companies operating in the Global Automotive Premium Tires Market include Michelin, Bridgestone, Goodyear Tire & Rubber Company, Continental, Pirelli, Hankook Tire & Technology, Yokohama Rubber Company, Sumitomo Rubber Industries (Dunlop), Apollo Tyres, and Cooper Tire & Rubber Company. Companies in the automotive premium tires market focus on product innovation, OEM collaboration, and portfolio diversification to strengthen their competitive position. Manufacturers invest heavily in advanced materials and compound technologies to improve durability, efficiency, and ride comfort. Strategic partnerships with automakers help secure long-term supply contracts and early inclusion in new vehicle platforms. Firms also expand premium replacement tire ranges to capture higher-margin aftermarket demand. Geographic expansion and localized production reduce supply chain risk and enhance responsiveness to regional demand trends.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Tire

- 2.2.3 Tire construction

- 2.2.4 Rim size

- 2.2.5 Vehicle

- 2.2.6 Technology

- 2.2.7 Sales channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising luxury & performance vehicle demand

- 3.2.1.2 Focus on safety, comfort & handling

- 3.2.1.3 Growing vehicle parc in developed markets

- 3.2.1.4 OEM premium positioning

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High price sensitivity limiting adoption in cost-conscious markets

- 3.2.2.2 Volatility in raw material prices impacting margins

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding premium vehicle sales in emerging economies

- 3.2.3.2 EV-specific tire demand

- 3.2.3.3 Aftermarket customization demand

- 3.2.3.4 Smart & sustainable tires

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. Department of Transportation (DOT) Standards

- 3.4.1.2 Occupational Safety and Health Administration (OSHA) Guidelines

- 3.4.1.3 U.S. Environmental Protection Agency (EPA)

- 3.4.2 Europe

- 3.4.2.1 EN ISO Tire Standards

- 3.4.2.2 European Union Customs and Safety Regulations

- 3.4.2.3 BS EN / CEN Standards

- 3.4.2.4 National Standards (UNE, DIN, etc.)

- 3.4.3 Asia Pacific

- 3.4.3.1 China GB (Guobiao) Standards

- 3.4.3.2 Japan JIS Requirements

- 3.4.3.3 Korea KS Certification

- 3.4.3.4 Indian BIS Standards

- 3.4.3.5 Thai Industrial Standards Institute (TISI)

- 3.4.4 Latin America

- 3.4.4.1 INMETRO (National Institute of Metrology)

- 3.4.4.2 INTI certification (Instituto Nacional de Tecnologia Industrial)

- 3.4.4.3 NOM standards (Norma Oficial Mexicana)

- 3.4.5 Middle East & Africa

- 3.4.5.1 ESMA / Emirates Conformity Assessment Scheme (ECAS)

- 3.4.5.2 GCC technical regulations

- 3.4.5.3 SABS certification

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis

- 3.8.1 Pricing by product

- 3.8.2 Pricing by region

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 EV-Specific Tire Economics & Design Trade-offs

- 3.13.1 Rolling resistance vs durability trade-offs

- 3.13.2 Acoustic foam cost premium

- 3.13.3 Impact on ASP and margins

- 3.13.4 EV vs ICE replacement economics

- 3.14 Raw Material Risk & Cost Sensitivity Analysis

- 3.15 Channel-Level Margin & Pricing Analysis

- 3.16 Consumer Behavior & Premium Adoption Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Tire, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Summer tires

- 5.3 Winter tires

- 5.4 All-season tires

- 5.5 All terrain tires

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Tire Construction, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Radial

- 6.3 Bias

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV (Light commercial vehicle)

- 7.3.2 MCV (Medium commercial vehicle)

- 7.3.3 HCV (Heavy commercial vehicle)

Chapter 8 Market Estimates & Forecast, By Rim Size, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Below 15 inches

- 8.3 15-20 inches

- 8.4 Above 20 inches

Chapter 9 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Run-flat technology

- 9.3 Self-sealing tires

- 9.4 Eco-friendly tires

- 9.5 Noise reduction technology

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Nordics

- 11.3.7 Russia

- 11.3.8 Poland

- 11.3.9 Romania

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Vietnam

- 11.4.7 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 Apollo Tyres

- 12.1.2 Bridgestone

- 12.1.3 Continental

- 12.1.4 Cooper Tire & Rubber Company

- 12.1.5 Goodyear Tire & Rubber Company

- 12.1.6 Hankook Tire & Technology

- 12.1.7 Kumho Tire

- 12.1.8 Michelin

- 12.1.9 Pirelli

- 12.1.10 Sumitomo Rubber Industries

- 12.1.11 Toyo Tire

- 12.1.12 Yokohama Rubber Company

- 12.2 Regional players

- 12.2.1 CEAT

- 12.2.2 Giti Tire

- 12.2.3 JK Tyre & Industries

- 12.2.4 Linglong Tire

- 12.2.5 Maxxis International

- 12.2.6 MRF Tyres

- 12.2.7 Nexen Tire

- 12.2.8 Nokian Tyres

- 12.2.9 Sailun

- 12.3 Emerging players

- 12.3.1 Double Coin

- 12.3.2 Laufenn

- 12.3.3 Petlas

- 12.3.4 Radar Tires

- 12.3.5 Triangle Tyre

- 12.3.6 ZC Rubber

汽车智慧轮胎市场:按车辆类型、轮胎类型、应用和销售管道划分-2026-2032年全球市场预测

汽车智慧轮胎市场:按车辆类型、轮胎类型、应用和销售管道划分-2026-2032年全球市场预测 智慧轮胎市场-全球产业规模、份额、趋势、机会、预测:按类型、车辆类型、技术类型、销售管道类型、地区和竞争格局划分,2021-2031年超高性能轮胎市场-全球产业规模、份额、趋势、机会和预测:按轮胎类型、需求类别、车辆类型、地区和竞争格局划分,2021-2031年高性能乘用车轮胎市场-全球产业规模、份额、趋势、机会及预测(2021-2031)

智慧轮胎市场-全球产业规模、份额、趋势、机会、预测:按类型、车辆类型、技术类型、销售管道类型、地区和竞争格局划分,2021-2031年超高性能轮胎市场-全球产业规模、份额、趋势、机会和预测:按轮胎类型、需求类别、车辆类型、地区和竞争格局划分,2021-2031年高性能乘用车轮胎市场-全球产业规模、份额、趋势、机会及预测(2021-2031) 超高性能轮胎市场规模、份额及成长分析(按车辆类型、轮胎类型、技术及地区划分)-2026-2033年产业预测

超高性能轮胎市场规模、份额及成长分析(按车辆类型、轮胎类型、技术及地区划分)-2026-2033年产业预测 高性能轮圈市场规模、份额及成长分析(按材料、车辆类型、应用、直径尺寸、销售管道和地区划分)-2026-2033年产业预测

高性能轮圈市场规模、份额及成长分析(按材料、车辆类型、应用、直径尺寸、销售管道和地区划分)-2026-2033年产业预测 全球高性能轮胎市场

全球高性能轮胎市场 全球高性能车轮市场预测(至 2032 年):按类型、材料、车辆类型、轮圈尺寸、製造流程、表面处理、销售管道、应用和地区划分全球高性能轮圈市场

全球高性能车轮市场预测(至 2032 年):按类型、材料、车辆类型、轮圈尺寸、製造流程、表面处理、销售管道、应用和地区划分全球高性能轮圈市场 高性能轮胎:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

高性能轮胎:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)