|

市场调查报告书

商品编码

1936616

夜光颜料市场机会、成长要素、产业趋势分析及2026年至2035年预测Phosphorescent Pigments Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球发光颜料市场预计到 2025 年将达到 7.95 亿美元,到 2035 年将达到 15 亿美元,年复合成长率为 6.8%。

市场成长得益于光致发光材料在安全关键型应用领域(例如商业建筑、公共基础设施、交通设施和工业环境)的日益普及。即使在断电情况下也能提供可靠照明的光致发光材料,随着紧急应变和可见性日益受到重视,其需求持续成长。建筑安全和消防法规结构要求安装断电后仍能正常运作的可见性引导系统,进一步巩固了这项稳定需求。颜料技术的不断进步,透过提高亮度、延长发光持续时间和增强抗环境应力能力,进一步加速了市场扩张。材料性能的提升拓展了其在涂料、工程塑胶和特殊材料领域的应用,使製造商能够瞄准更高价值的应用。持续的技术创新透过提高耐高温、耐湿和抗紫外线能力,增强了材料的长期性能。随着安全标准的不断改进和全球基础设施投资的增加,光致发光颜料仍然是可见性关键应用领域的重要组成部分,从而维持了市场的稳定成长。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 7.95亿美元 |

| 预测金额 | 15亿美元 |

| 复合年增长率 | 6.8% |

预计到2025年,铝酸锶颜料市场规模将达到5.088亿美元。这类颜料凭藉其优异的发光性能、持久的余辉时间和更高的能量吸收效率,在全球市场占据主导地位。其卓越的性能使其成为需要持久可见性的应用领域的首选解决方案。此外,这类颜料的无害成分也进一步促进了其在受监管行业中的广泛应用,尤其是在需要遵守严格安全标准的建筑和交通运输行业。

预计到2025年,安全和识别领域市场规模将达到2.624亿美元,成为该市场最重要的应用领域之一。在这些应用中,磷光颜料用于在紧急情况下保持可见性,而无需外部电源。对职场安全、紧急应变和建筑规范合规性的日益重视,持续推动商业、工业和公共建筑领域对磷光颜料的稳定需求。基础设施建设的不断发展也进一步增强了该领域对整体市场成长的贡献。

预计到2025年,北美发光颜料市场规模将达到1.749亿美元,并在整个预测期内保持强劲成长动能。该地区对安全标准和基础设施韧性的严格监管是维持市场需求的关键因素。此外,商业建筑和交通设施的持续投资也推动了光致发光材料在各种应用领域的普及。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 安全和应急标誌的需求日益增长

- 颜料性能的技术进步

- 消费品和装饰应用领域的拓展

- 产业潜在风险与挑战

- 某些条件下的性能劣化

- 监管和环境挑战

- 市场机会

- 智慧基础设施和城市发展的成长

- 环保节能解决方案

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 产品类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 依产品类型分類的市场估算与预测,2022-2035年

- 铝酸锶

- 硫化锌

- 其他的

第六章 按应用领域分類的市场估算与预测,2022-2035年

- 油漆和涂料

- 塑胶和聚合物

- 印刷油墨

- 安全列印

- 装饰性的

- 安全/标誌

- 紧急出口指示牌

- 道路标线

- 家用电子电器

- 显示背光

- 穿戴式装置

- 其他的

7. 2022-2035年按最终用途产业分類的市场估算与预测

- 汽车/运输设备

- 航太/国防

- 包装

- 纺织业

- 建造

- 船

- 其他的

第八章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- Nemoto &Co., Ltd.

- United Mineral and Chemical Corp.

- Zegen Advanced Materials

- Lumentics

- iSuoChem

- OliKrom

- Lab Alley

- RTP Company

- Badger Color Concentrates, Inc

- Techno Glow Inc

- Vishnu Priya Chemicals Pvt Ltd

- Chemical Bull

- Zhejiang Minhui Luminous Technology Co., Ltd

- AB Enterprises

- Stanford Advanced Materials

- SINO SUNMAN INTERNATIONAL

- Solstice Advanced Materials Inc.

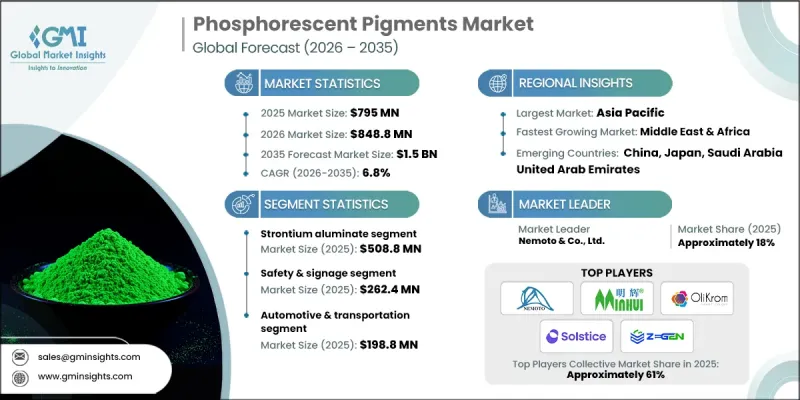

The Global Phosphorescent Pigments Market was valued at USD 795 million in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 1.5 billion by 2035.

Market growth is supported by rising adoption of photoluminescent materials in safety-focused applications across commercial buildings, public infrastructure, transportation facilities, and industrial environments. Increasing emphasis on emergency preparedness and visibility continues to drive demand, as phosphorescent materials provide reliable illumination during power interruptions. Regulatory frameworks related to building safety and fire protection have reinforced consistent consumption by mandating visible guidance systems that function without electricity. Ongoing advancements in pigment technology are further accelerating market expansion by improving brightness intensity, glow duration, and resistance to environmental stress. Enhanced material performance has broadened usage across coatings, engineered plastics, and specialty materials, enabling manufacturers to target higher-value applications. Continuous innovation has improved durability under exposure to heat, moisture, and ultraviolet conditions, supporting long-term performance. As safety standards evolve and infrastructure investment increases globally, phosphorescent pigments remain essential components in visibility-driven applications, sustaining steady market momentum.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $795 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 6.8% |

The strontium aluminate-based pigments segment reached USD 508.8 million in 2025. These pigments dominate global demand due to their superior luminosity, extended afterglow duration, and enhanced energy absorption efficiency. Their performance advantages have positioned them as preferred solutions for applications requiring long-lasting visibility. The non-hazardous composition of these pigments further supports widespread acceptance across regulated industries, particularly in construction and transportation environments that require compliance with strict safety standards.

The safety and signage segment accounted for USD 262.4 million in 2025, representing one of the most substantial usage segments within the market. These applications rely on phosphorescent pigments to maintain visibility in emergency situations without external power sources. Growing focus on workplace safety, emergency preparedness, and building compliance continues to drive steady demand across commercial, industrial, and public settings. Increased infrastructure development further strengthens this segment's contribution to overall market growth.

North America Phosphorescent Pigments Market generated USD 174.9 million in 2025 and is expected to witness attractive growth throughout the forecast period. Strong regulatory enforcement related to safety compliance and infrastructure resilience supports sustained regional demand. Ongoing investments in commercial construction and transportation facilities reinforce the adoption of photoluminescent materials across multiple applications.

Key companies operating in the Global Phosphorescent Pigments Market include Nemoto & Co., Ltd., Zegen Advanced Materials, United Mineral and Chemical Corp., RTP Company, Lumentics, Stanford Advanced Materials, iSuoChem, OliKrom, Techno Glow Inc, Badger Color Concentrates, Inc, Zhejiang Minhui Luminous Technology Co., Ltd, Vishnu Priya Chemicals Pvt Ltd, Chemical Bull, AB Enterprises, Lab Alley, SINO SUNMAN INTERNATIONAL, and Solstice Advanced Materials Inc. Companies in the phosphorescent pigments market strengthen their competitive position through continuous material innovation, capacity expansion, and application-focused product development. Manufacturers invest heavily in research to enhance glow efficiency, durability, and environmental stability. Strategic partnerships with coatings, plastics, and construction material suppliers support wider adoption. Portfolio diversification across industrial, commercial, and infrastructure applications improves revenue resilience.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand in safety & emergency signage

- 3.2.1.2 Technological advancements in pigment performance

- 3.2.1.3 Expansion in consumer goods & decorative applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Performance degradation under certain conditions

- 3.2.2.2 Regulatory & environmental challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in smart infrastructure & urban development

- 3.2.3.2 Eco-friendly & energy-saving solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Strontium aluminate

- 5.3 Zinc sulfide

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Coatings & paints

- 6.3 Plastics & polymers

- 6.4 Printing inks

- 6.4.1 Security printing

- 6.4.2 Decorative

- 6.5 Safety & signage

- 6.5.1 Emergency exit signs

- 6.5.2 Road marking

- 6.6 Consumer electronics

- 6.6.1 Display backlighting

- 6.6.2 Wearables

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive & transportation

- 7.3 Aerospace & defense

- 7.4 Packaging

- 7.5 Textiles

- 7.6 Construction

- 7.7 Marine

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Nemoto & Co., Ltd.

- 9.2 United Mineral and Chemical Corp.

- 9.3 Zegen Advanced Materials

- 9.4 Lumentics

- 9.5 iSuoChem

- 9.6 OliKrom

- 9.7 Lab Alley

- 9.8 RTP Company

- 9.9 Badger Color Concentrates, Inc

- 9.10 Techno Glow Inc

- 9.11 Vishnu Priya Chemicals Pvt Ltd

- 9.12 Chemical Bull

- 9.13 Zhejiang Minhui Luminous Technology Co., Ltd

- 9.14 AB Enterprises

- 9.15 Stanford Advanced Materials

- 9.16 SINO SUNMAN INTERNATIONAL

- 9.17 Solstice Advanced Materials Inc.