|

市场调查报告书

商品编码

1936626

磺酸盐聚合物市场机会、成长要素、产业趋势分析及2026年至2035年预测Sulfone Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

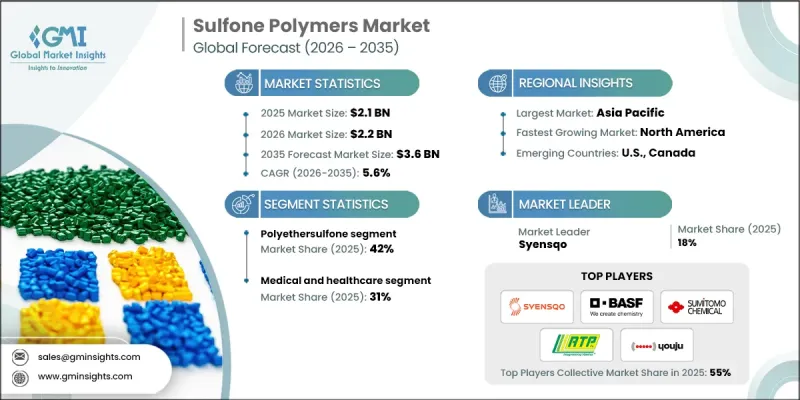

全球磺酸盐聚合物市场预计到 2025 年将达到 21 亿美元,到 2035 年将达到 36 亿美元,年复合成长率为 5.6%。

该市场涵盖聚砜(PSU)、聚醚砜(PESU)、聚苯砜(PPSU) 和聚醚酰亚胺 (PEI) 的收入,这些产品以原生颗粒、膜级粉末和复合配方的形式供应。定价受多种因素影响,例如分子量分布、材料纯度、灭菌认证、阻燃等级以及食品和水接触认证,其中特种等级的产品价格通常高出 20-40%。由于这些等级产品的高附加价值特性,即使需求略微转向医疗和膜应用领域,也可能对收入产生不成比例的影响。在医疗领域,生物相容性、灭菌耐久性和长寿命性能是买家优先考虑的因素,而 PPSU 医疗组件可以承受多次蒸气灭菌循环。在水处理领域,薄膜性能(包括通量效率和污垢恢復能力)至关重要,而基于 PES 的薄膜已展现出高通量和清洗后快速恢復的特性。在电子和航太产业中,高玻璃化转变温度、尺寸稳定性和热变形温度能够满足严苛环境下的关键应用需求,进而推动稳定的需求和高产品良率。高性能材料的特性以及满足严格监管标准的能力,正在推动其在全球多个行业的市场扩张。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 21亿美元 |

| 预测金额 | 36亿美元 |

| 复合年增长率 | 5.6% |

预计到2025年,聚醚砜(PESU)市占率将达到42%。 PESU具有均衡的性能成本比,加上其亲水性、优异的耐化学性和高达220°C的热稳定性,使其非常适合用于水过滤、血液透析和工业分离膜。市售PESU粉末的分子量范围为45,000至68,000,其设计兼顾了溶解性和易于膜製备的特性。

预计到2025年,电子电气应用领域将占据22%的市场份额,这主要得益于磺酸盐聚合物的热稳定性、耐化学性和精确的尺寸控制。这些材料越来越多地应用于电子元件、绝缘模组以及需要在高温环境下运作并能保持性能公差的组件中,即使在高化学腐蚀条件下也能如此。对于照明应用而言,具有透明性和紫外线稳定性的砜类聚合物也是首选,因为这些应用对长期可靠性和耐热劣化要求极高。磺酸盐聚合物的多功能性和在严苛工作环境下的优异性能,使其在各种工业应用中得到更广泛的应用。

预计到2025年,北美磺酸盐聚合物市占率将达到27%。这项强劲的区域需求主要得益于先进的医疗设备製造、严格的医疗品质标准以及蓬勃发展的航太业。包括FDA核准和ASTM医疗应用标准在内的法规结构,为磺酸盐聚合物在关键医疗器材中的应用提供了支持。为减少废弃物和降低单次手术成本,可重复使用医疗设备的普及进一步提升了耐灭菌材料(如PSU和PPSU)的吸引力。此外,美国和加拿大航太製造业的集中,以及其庞大的供应链和工业基础,也推动了对航太磺酸盐聚合物的需求。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 2022-2035年依产品分類的市场规模及预测

- 聚砜(PSU)

- 聚醚砜(PESU)

- 聚苯砜(PPSU)

- 聚醚酰亚胺(PEI)

- 其他的

第六章 依性能等级分類的市场规模及预测,2022-2035年

- 标准级/商业级

- 医疗/保健等级

- 食品接触级

- 航太级

- 阻燃等级

- 其他的

7. 依最终用途产业分類的市场规模及预测,2022-2035年

- 医疗保健

- 医院及透析中心

- 医疗设备製造商

- 製药加工设备

- 航太

- 商业航空

- 军用/国防飞机

- 空间应用

- 车

- 内燃机(ICE)车辆

- 电动车(EV)

- 混合动力汽车

- 电气和电子设备

- 家用电子电器

- 半导体製造

- 资料中心伺服器

- 5G基础设施

- 水和污水处理

- 地方政府业务

- 工业水处理

- 海水淡化厂

- 食品/饮料加工

- 食品加工设备製造商

- 商用厨房/餐厅

- 电器产品

- 工业和製造业

- 管道和空调设备

- 化学处理设备

- 石油和天然气应用

- 能源与氢能经济

- 燃料电池製造商

- 电解设备製造商

- 氢能基础设施建设

- 其他的

第八章 2022-2035年各地区市场规模及预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- RTP Company

- Youju New Materials

- BASF SE

- SABIC

- Solvay

- Sumitomo Chemical

- Shandong Haoran Special Plastic

- Syensqo

- Mitsubishi Gas Chemical Company

- Atul Ltd

- Avient Corporation

- Ovation Polymers

- ASEP Industries Sdn Bhd

- Aurorium

- 3DXTech

- Foshan Plolima Material

The Global Sulfone Polymers Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 3.6 billion by 2035.

The market includes revenue generated from polysulfone (PSU), polyethersulfone (PESU), polyphenylsulfone (PPSU), and polyetherimide (PEI), offered as virgin pellets, membrane-grade powders, and compounded formulations. Pricing structures are influenced by factors such as molecular weight distribution, material purity, sterilization certifications, flame-retardant ratings, and approvals for food and water contact, which can command 20-40% premiums for specialized grades. Even small shifts in volume toward healthcare or membrane applications can have a disproportionate impact on revenue due to the high-value nature of these grades. In the healthcare sector, buyers prioritize biocompatibility, sterilization durability, and long lifecycle performance, which allow PPSU medical components to withstand multiple steam cycles. In water treatment, membrane performance, including flux efficiency and fouling recovery, is critical, and PES-based membranes have demonstrated high throughput with rapid recovery after cleaning. In electronics and aerospace, high glass transition temperatures, dimensional stability, and heat deflection capabilities support critical applications under extreme conditions, driving consistent demand and higher per-unit revenue. The combination of high-performance material properties and the ability to meet stringent regulatory standards is fueling global market expansion across multiple industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 5.6% |

The polyethersulfone segment held 42% share in 2025. Its balanced property-to-cost ratio, combined with hydrophilic behavior, excellent chemical resistance, and thermal stability up to 220°C, makes PESU highly suitable for water filtration, hemodialysis, and industrial separation membranes. Commercial powders of PESU, with molecular weights ranging from 45,000 to 68,000, are designed for ease of dissolution and membrane fabrication.

The electronics and electrical applications segment held 22% share in 2025, leveraging sulfone polymers' thermal stability, chemical resistance, and precise dimensional control. These materials are increasingly used in high-temperature electronic components, insulating modules, and assemblies where chemical exposure is high, but tolerances must be maintained. Transparent and UV-stable grades are also favored in lighting applications where long-term reliability and resistance to heat degradation are essential. The versatility of sulfone polymers, coupled with their performance in demanding operating environments, continues to reinforce their adoption across diverse industrial applications.

North America Sulfone Polymers Market represented 27% share in 2025. The strong regional demand is driven by advanced medical device manufacturing, strict healthcare quality standards, and a robust aerospace sector. Regulatory frameworks, including FDA recognition and ASTM standards for medical applications, support the use of sulfone polymers for critical devices. Emphasis on reusable medical devices to reduce waste and per-procedure costs further enhances the appeal of sterilization-resistant materials such as PSU and PPSU. The concentration of aerospace manufacturing in the U.S. and Canada, supported by extensive supply chains and large-scale industrial operations, also fuels demand for aerospace-grade sulfone polymers.

Key players operating in the Global Sulfone Polymers Market include Shandong Haoran Special Plastic, Mitsubishi Gas Chemical Company, RTP Company, Sumitomo Chemical, BASF SE, SABIC, Youju New Materials, Syensqo, Atul Ltd, and Solvay. To strengthen their presence, companies in the sulfone polymers industry are adopting multiple strategic initiatives. They are investing heavily in research and development to produce polymers with superior thermal, chemical, and sterilization performance, tailored for healthcare, aerospace, and membrane applications. Strategic collaborations, joint ventures, and mergers allow firms to expand their geographical footprint, access new customer segments, and improve supply chain efficiency. Many companies are optimizing production processes to reduce costs while enhancing material purity and performance. Firms are also focusing on regulatory compliance, obtaining medical and industrial certifications to improve credibility and customer trust. Advanced digital platforms for material testing, real-time quality monitoring, and customer support further enhance operational efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product

- 2.2.2 Performance grade

- 2.2.3 End use industry

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Product, 2022-2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Polysulfone (PSU)

- 5.3 Polyethersulfone (PESU)

- 5.4 Polyphenylsulfone (PPSU)

- 5.5 Polyetherimide (PEI)

- 5.6 Others

Chapter 6 Market Size and Forecast, By Performance Grade, 2022-2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Standard/commercial grade

- 6.3 Medical/healthcare grade

- 6.4 Food contact grade

- 6.5 Aerospace grade

- 6.6 Flame retardant grade

- 6.7 Others

Chapter 7 Market Size and Forecast, By End Use Industry , 2022-2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Medical & healthcare

- 7.2.1 Hospitals & dialysis centers

- 7.2.2 Medical device manufacturers

- 7.2.3 Pharmaceutical processing equipment

- 7.3 Aerospace

- 7.3.1 Commercial aviation

- 7.3.2 Military & defense aircraft

- 7.3.3 Space applications

- 7.4 Automotive

- 7.4.1 Internal combustion engine (ICE) vehicles

- 7.4.2 Electric vehicles (EVs)

- 7.4.3 Hybrid vehicles

- 7.5 Electrical & electronics

- 7.5.1 Consumer electronics

- 7.5.2 Semiconductor manufacturing

- 7.5.3 Data centers & servers

- 7.5.4 5g infrastructure

- 7.6 Water & wastewater treatment

- 7.6.1 Municipal utilities

- 7.6.2 Industrial water treatment

- 7.6.3 Desalination plants

- 7.7 Food & beverage processing

- 7.7.1 Food processing equipment manufacturers

- 7.7.2 Commercial kitchens & restaurants

- 7.7.3 Household appliances

- 7.8 Industrial & manufacturing

- 7.8.1 Plumbing & HVAC

- 7.8.2 Chemical processing equipment

- 7.8.3 Oil & gas applications

- 7.9 Energy & hydrogen economy

- 7.9.1 Fuel cell manufacturers

- 7.9.2 Electrolyzer manufacturers

- 7.9.3 Hydrogen infrastructure development

- 7.10 Others

Chapter 8 Market Size and Forecast, By Region, 2022-2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 RTP Company

- 9.2 Youju New Materials

- 9.3 BASF SE

- 9.4 SABIC

- 9.5 Solvay

- 9.6 Sumitomo Chemical

- 9.7 Shandong Haoran Special Plastic

- 9.8 Syensqo

- 9.9 Mitsubishi Gas Chemical Company

- 9.10 Atul Ltd

- 9.11 Avient Corporation

- 9.12 Ovation Polymers

- 9.13 ASEP Industries Sdn Bhd

- 9.14 Aurorium

- 9.15 3DXTech

- 9.16 Foshan Plolima Material

全球磺酸盐聚合物市场规模、份额、趋势及成长分析报告(2026-2034年)

全球磺酸盐聚合物市场规模、份额、趋势及成长分析报告(2026-2034年) 聚砜市场规模、份额和成长分析(按类型、等级、应用、最终用途产业和地区划分)-2026-2033年产业预测

聚砜市场规模、份额和成长分析(按类型、等级、应用、最终用途产业和地区划分)-2026-2033年产业预测 磺酸盐聚醚砜:全球市占率及排名、总营收及需求预测(2025-2031年)

磺酸盐聚醚砜:全球市占率及排名、总营收及需求预测(2025-2031年) 砜类聚合物市场按产品类型、最终用途产业、应用和形态划分-2025-2032年全球预测

砜类聚合物市场按产品类型、最终用途产业、应用和形态划分-2025-2032年全球预测 苯基三溴磺酸盐的全球市场聚砜的全球市场砜类聚合物市场(按类型、应用和地区划分),2026 年至 2032 年

苯基三溴磺酸盐的全球市场聚砜的全球市场砜类聚合物市场(按类型、应用和地区划分),2026 年至 2032 年 磺酸盐聚合物市场:依产品类型、应用和地区划分

磺酸盐聚合物市场:依产品类型、应用和地区划分 聚苯砜市场报告:趋势、预测和竞争分析(至 2031 年)聚醚砜市场报告:趋势、预测和竞争分析(至 2031 年)

聚苯砜市场报告:趋势、预测和竞争分析(至 2031 年)聚醚砜市场报告:趋势、预测和竞争分析(至 2031 年)