|

市场调查报告书

商品编码

1936629

电线电缆聚合物市场机会、成长要素、产业趋势分析及2026年至2035年预测Wire and Cable Polymer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

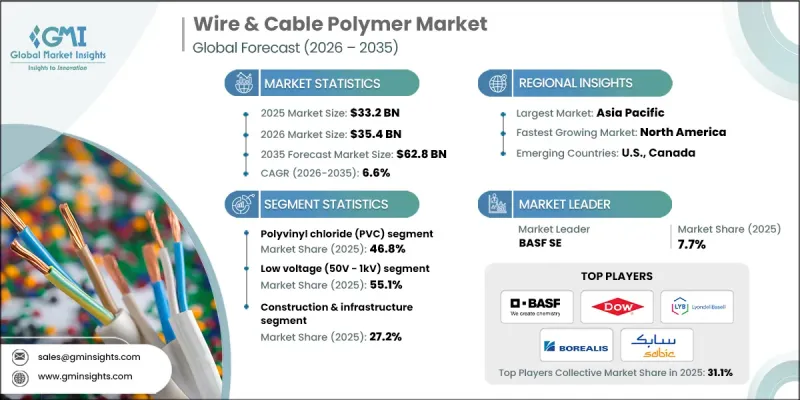

全球电线电缆聚合物市场预计到 2025 年将达到 332 亿美元,到 2035 年将达到 628 亿美元,年复合成长率为 6.6%。

由于建筑、汽车、通讯和能源等行业的需求不断增长,市场正经历强劲增长。市场的一个关键趋势是从传统聚合物材料转向先进的高性能聚合物,例如交联聚乙烯 (XLPE)、热可塑性橡胶(TPE) 和阻燃塑料,这些聚合物具有卓越的耐久性、柔软性和安全性。这些现代聚合物因其优异的电绝缘性能、承受环境压力的能力以及防止短路和功率损耗的能力而日益受到青睐。其应用领域十分广泛:在建筑领域用于电力和布线系统;在汽车领域用于线束和电子元件;在通讯领域用于光纤电缆;在可再生能源领域用于太阳能和风能电缆。耐化学腐蚀性、轻量化设计、易于加工和长期可靠性等关键优势持续推动聚合物在全球电线电缆应用中的普及。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 332亿美元 |

| 预测金额 | 628亿美元 |

| 复合年增长率 | 6.6% |

低压电缆(50V-1kV)市占率占比达55.1%,预计2026年至2035年将以6.8%的复合年增长率成长。此细分市场广泛应用于住宅和商业领域,其成长主要得益于都市化、智慧建筑发展以及节能电缆解决方案的日益普及。政府和私人企业对智慧电网现代化和可再生能源併网的投资,尤其註重安全性、可靠性和环境永续性,进一步推动了对用于低压电缆的耐用、高性能聚合物的需求。

预计到2025年,建筑和基础设施产业将占据27.2%的市场份额,并在2035年之前以6.9%的复合年增长率成长。都市化、智慧城市计划和大型基础设施建设持续推动着对坚固耐用、使用寿命长的电缆系统的需求。此外,太阳能和风能发电等可再生能源计划的扩张也增加了对具有更高热稳定性、优异绝缘性和增强耐久性的聚合物电缆的需求,以应对恶劣的环境条件并确保可靠的电力传输。

预计到2025年,北美电线电缆聚合物市场将占据15.1%的份额。该地区市场扩张的驱动力主要来自基础设施现代化、可再生能源投资以及通讯产业的成长。电动车的日益普及和智慧电网计画的推进,正在推动对具有优异绝缘性能、阻燃性和柔软性的高性能聚合物的需求。该地区严格的安全和环境法规促使製造商开发环保阻燃聚合物电缆,从而将产品创新与永续性和法规遵循相结合。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 依聚合物类型分類的市场估算与预测,2022-2035年

- 聚乙烯

- 低密度聚乙烯(LDPE)

- 高密度聚苯乙烯(HDPE)

- 线型低密度聚乙烯(LLDPE)

- 聚丙烯

- 聚氯乙烯(PVC)

- 软氯乙烯树脂

- 硬质氯乙烯树脂

- 弹性体

- 乙丙橡胶(EPR)

- 乙丙橡胶 (EPDM)

- 硅橡胶

- 热可塑性橡胶(TPE)

- 热塑性聚氨酯(TPU)

- 氟树脂

- 聚四氟乙烯(PTFE)

- 氟化乙烯丙烯(FEP)

- 全氟烷氧基(PFA)

- 乙烯-四氟乙烯(ETFE)

- 高性能聚合物

- 聚醚醚酮(PEEK)

- 聚醚酰亚胺(PEI)

- 聚亚苯硫醚(PPS)

- 无卤阻燃剂(HFFR)化合物

- 其他的

第六章 按电压分類的市场估算与预测,2022-2035年

- 低电压(50V 至 1kV)

- 中压(1kV至35kV)

- 高压(35kV至150kV)

7. 2022-2035年按最终用户产业分類的市场估算与预测

- 发电

- 电讯

- 汽车/运输设备

- 建筑和基础设施

- 工业製造

- 石油和天然气

- 采矿和资源

- 可再生能源

- 资料中心和IT

- 航太/国防

- 卫生保健

第八章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- Arkema SA

- BASF SE

- Borealis AG

- Dow Inc.

- Eastman Chemical Company

- ExxonMobil Corporation

- LG Chem Ltd

- LyondellBasell Industries NV

- Mitsui Chemicals, Inc.

- SABIC

- Solvay SA

- Sumitomo Chemical Co., Ltd.

The Global Wire and Cable Polymer Market was valued at USD 33.2 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 62.8 billion by 2035.

The market is experiencing robust growth due to rising demand across sectors such as construction, automotive, telecommunications, and energy. A key trend in the market is the shift from conventional polymer materials to advanced high-performance polymers, including cross-linked polyethylene (XLPE), thermoplastic elastomers (TPE), and flame-retardant plastics, which offer superior durability, flexibility, and safety. These modern polymers are increasingly preferred because of their excellent electrical insulation, resistance to environmental stress, and capacity to prevent short circuits and power loss. Their applications are widespread: in construction for power and wiring systems, in automotive for wiring harnesses and electronic components, in telecommunications for fiber optic cables, and in renewable energy for solar and wind power cabling. Key benefits such as chemical resistance, lightweight design, ease of processing, and long-term reliability continue to drive polymer adoption in wire and cable applications worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $33.2 Billion |

| Forecast Value | $62.8 Billion |

| CAGR | 6.6% |

The low voltage cables (50V-1kV) segment held 55.1% share and is expected to grow at a CAGR of 6.8% from 2026 to 2035. This segment is widely used in residential and commercial applications and has been propelled by urbanization, smart building developments, and the increasing integration of energy-efficient wiring solutions. Investments by governments and private enterprises in smart grid modernization and renewable energy integration have further accelerated demand for durable, high-performance polymers in low-voltage cabling while emphasizing safety, reliability, and environmental sustainability.

The construction and infrastructure sector accounted for 27.2% share in 2025 and is anticipated to grow at a CAGR of 6.9% through 2035. Urbanization, smart city projects, and large-scale infrastructure development continue to drive the need for robust, long-lasting wiring systems. Additionally, the growth of renewable energy projects, such as solar and wind power, has increased demand for polymer cables with higher thermal stability, superior insulation, and enhanced durability to withstand harsh environmental conditions and ensure reliable power transmission.

North America Wire and Cable Polymer Market accounted for 15.1% share in 2025. The region's expansion is fueled by infrastructural modernization, renewable energy investments, and the growth of the telecommunications sector. Rising adoption of electric vehicles and smart grid initiatives has created increasing demand for high-performance polymers that combine excellent insulation, fire resistance, and flexibility. Strict safety and environmental regulations in the region are encouraging manufacturers to develop eco-friendly, flame-retardant polymer cables, aligning product innovation with sustainability and regulatory compliance.

Major companies in the Global Wire and Cable Polymer Market include Dow Inc., Arkema SA, LG Chem Ltd, ExxonMobil Corporation, Borealis AG, LyondellBasell Industries N.V., Solvay SA, Mitsui Chemicals, Inc., Eastman Chemical Company, BASF SE, Sumitomo Chemical Co., Ltd., and SABIC. Leading players in the wire and cable polymer market are adopting several strategies to strengthen their presence and expand market share. They are investing heavily in research and development to create high-performance, eco-friendly polymers with superior insulation, fire resistance, and mechanical properties. Strategic partnerships with manufacturers, construction companies, and energy providers help ensure a consistent supply and market penetration. Companies are also focusing on product diversification to meet the needs of low-, medium-, and high-voltage applications across various industries. Expansion into emerging markets and regional production facilities reduces lead times and cost, while sustainability initiatives, such as biodegradable and flame-retardant polymers, help align with regulatory standards and growing consumer demand for safe, environmentally responsible materials.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Polymer type

- 2.2.3 Voltage

- 2.2.4 End-user industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Polymer Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene

- 5.2.1 Low Density Polyethylene (LDPE)

- 5.2.2 High Density Polyethylene (HDPE)

- 5.2.3 Linear Low Density Polyethylene (LLDPE)

- 5.3 Polypropylene

- 5.4 Polyvinyl Chloride (PVC)

- 5.4.1 Flexible PVC

- 5.4.2 Rigid PVC

- 5.5 Elastomers

- 5.5.1 Ethylene Propylene Rubber (EPR)

- 5.5.2 Ethylene Propylene Diene Monomer (EPDM)

- 5.5.3 Silicone Rubber

- 5.5.4 Thermoplastic Elastomers (TPE)

- 5.5.5 Thermoplastic Polyurethane (TPU)

- 5.6 Fluoropolymers

- 5.6.1 Polytetrafluoroethylene (PTFE)

- 5.6.2 Fluorinated Ethylene Propylene (FEP)

- 5.6.3 Perfluoroalkoxy (PFA)

- 5.6.4 Ethylene Tetrafluoroethylene (ETFE)

- 5.7 High-Performance Polymers

- 5.7.1 Polyether Ether Ketone (PEEK)

- 5.7.2 Polyetherimide (PEI)

- 5.7.3 Polyphenylene Sulfide (PPS)

- 5.8 Halogen-Free Flame Retardant (HFFR) Compounds

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Voltage, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Low voltage (50V - 1kV)

- 6.3 Medium voltage (1kV - 35kV)

- 6.4 High voltage (35kV - 150kV)

Chapter 7 Market Estimates and Forecast, By End-User Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Power generation

- 7.3 Telecommunications

- 7.4 Automotive & transportation

- 7.5 Construction & infrastructure

- 7.6 Industrial manufacturing

- 7.7 Oil & gas

- 7.8 Mining & resources

- 7.9 Renewable energy

- 7.10 Data centers & IT

- 7.11 Aerospace & defense

- 7.12 Healthcare

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Arkema SA

- 9.2 BASF SE

- 9.3 Borealis AG

- 9.4 Dow Inc.

- 9.5 Eastman Chemical Company

- 9.6 ExxonMobil Corporation

- 9.7 LG Chem Ltd

- 9.8 LyondellBasell Industries N.V.

- 9.9 Mitsui Chemicals, Inc.

- 9.10 SABIC

- 9.11 Solvay SA

- 9.12 Sumitomo Chemical Co., Ltd.