|

市场调查报告书

商品编码

1936632

败血症诊断市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Sepsis Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

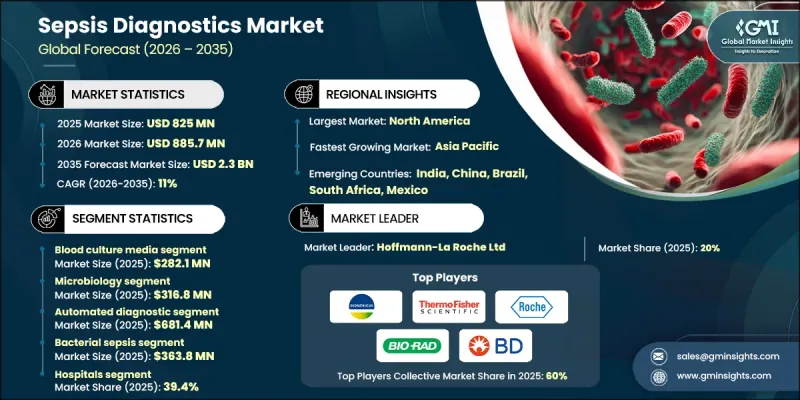

全球败血症诊断市场预计到 2025 年将达到 8.25 亿美元,到 2035 年将达到 23 亿美元,年复合成长率为 11%。

这一增长得益于感染疾病率的上升、公共部门对感染控制的日益重视以及诊断技术的不断进步。临床医师和患者对及时诊断重要性的认识不断提高,也进一步增强了市场需求。抗菌素抗药性、医院感染以及慢性病盛行率的不断上升等因素持续增加败血症的风险,尤其是在老年人和免疫免疫力缺乏低下患者中。医疗机构越来越重视快速且准确的诊断解决方案,以提高存活率并有效控制治疗成本。由于早期发现是改善临床结果的关键,对照护现场诊断和快速诊断工具日益增长的需求为创新和全球市场扩张创造了有利条件。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 8.25亿美元 |

| 预测金额 | 23亿美元 |

| 复合年增长率 | 11% |

政府主导的公共卫生基础设施投资持续推动市场成长。由于感染疾病的进展密切相关,早期检测已成为公共卫生工作的首要任务。各国医疗保健计画日益重视改善诊断系统、加强检测能力和加速临床决策。这些措施正在推动先进诊断平台的应用,从而增强医院和实验室的需求。

预计到2025年,血液培养基市场规模将达到2.821亿美元。这些产品旨在促进血液样本中微生物的生长,从而实现血液感染的检测。它们与自动化诊断系统的兼容性以及在临床检查室的持续应用确保了其稳定的市场需求。由于血液培养基在确诊感染疾病发挥着至关重要的作用,因此它仍然是败血症诊断的核心组成部分。

预计到2025年,基于微生物学的诊断市场规模将达到3.168亿美元。该技术专注于从患者检体中培养和鑑定病原体,并在临床实践中广泛应用。它支持详细的微生物鑑定和抗菌药物敏感性测试,这对于制定有效的治疗方案和改善患者管理至关重要。

预计到2025年,美国败血症诊断市场规模将达到2.837亿美元。不断上升的感染率以及老年人和免疫力缺乏低下人群日益增长的脆弱性,持续推动对快速诊断解决方案的需求。强大的医疗基础设施和先进诊断技术的广泛应用,为全美市场的持续成长提供了支撑。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 产业影响因素

- 司机

- 感染疾病率迅速上升

- 政府加大力度对抗感染疾病

- 感染疾病诊断的技术进步

- 人们对感染疾病及其诊断的认识不断提高

- 产业潜在风险与挑战

- 败血症诊断设备高成本

- 严格的法规结构

- 市场机会

- 与人工智慧和数位健康相结合

- 司机

- 成长潜力分析

- 监管环境

- 技术进步

- 当前技术趋势

- 新兴技术

- 2024年定价分析

- 未来市场趋势

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 合作伙伴关係和合资企业

- 新产品发布

- 扩张计划

5. 按测试类型分類的市场估算与预测,2022-2035 年

- 血液培养基

- 装置

- 检测试剂盒和试剂

- 软体

第六章 按技术分類的市场估计与预测,2022-2035年

- 微生物学

- 分子诊断

- 免疫检测

- 流式细胞技术

7. 依方法类型分類的市场估算与预测,2022-2035 年

- 常规诊断

- 自动化诊断

8. 依病原体类型分類的市场估算与预测,2022-2035 年

- 细菌性败血症

- 霉菌性败血症

- 其他病原体类型

9. 依最终用途分類的市场估计与预测,2022-2035 年

- 医院

- 诊断中心

- 诊所

- 其他最终用户

第十章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第十一章 公司简介

- F. Hoffmann-La Roche Ltd

- Thermo Fisher Scientific

- Abbott Laboratories

- Beckman Coulter Inc

- Siemens Healthineers

- Becton, Dickinson and Company

- bioMerieux SA

- Bio-Rad Laboratories

- Bruker Corporation

- T2 Biosystems, Inc

The Global Sepsis Diagnostics Market was valued at USD 825 million in 2025 and is estimated to grow at a CAGR of 11% to reach USD 2.3 billion by 2035.

Growth is supported by the rising incidence of infectious diseases, increasing public-sector focus on infection control, and continuous progress in diagnostic technologies. Greater awareness among clinicians and patients regarding the importance of timely diagnosis is further strengthening market demand. Factors such as antimicrobial resistance, hospital-acquired infections, and the expanding prevalence of chronic health conditions continue to elevate sepsis risk, especially among elderly and immunocompromised individuals. Healthcare providers are increasingly prioritizing rapid and accurate diagnostic solutions to improve survival rates and manage treatment costs more effectively. The growing need for point-of-care and faster diagnostic tools is creating favorable conditions for innovation and global market expansion, as early detection remains critical for improving clinical outcomes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $825 Million |

| Forecast Value | $2.3 Billion |

| CAGR | 11% |

Government-driven investments in public health infrastructure continue to accelerate market growth. Sepsis is closely linked to infectious disease progression, making early identification a public health priority. National healthcare programs increasingly emphasize improved diagnostic readiness, enhanced laboratory capacity, and faster clinical decision-making. These initiatives support wider adoption of advanced diagnostic platforms and strengthen demand across hospital and laboratory settings.

The blood culture media segment generated USD 282.1 million in 2025. These products are formulated to promote the growth of microorganisms from blood samples, enabling the detection of bloodstream infections. Their compatibility with automated diagnostic systems and consistent usage across clinical laboratories ensures stable demand. Blood culture media remain a core component of sepsis diagnostics due to their essential role in confirming infections.

The microbiology-based diagnostics segment accounted for USD 316.8 million in 2025. This approach focuses on cultivating and identifying pathogens from patient samples and remains widely accepted in clinical practice. It supports detailed organism identification and antimicrobial sensitivity analysis, which are essential for guiding effective treatment decisions and improving patient management.

U.S. Sepsis Diagnostics Market was valued at USD 283.7 million in 2025. Rising infection rates and increased vulnerability among aging and immunocompromised populations continue to drive demand for rapid diagnostic solutions. Strong healthcare infrastructure and high adoption of advanced diagnostic technologies support sustained market growth across the country.

Key companies active in the Global Sepsis Diagnostics Market include Abbott Laboratories, Thermo Fisher Scientific, Inc., bioMerieux SA, F. Hoffmann-La Roche Ltd, Siemens Healthineers, Becton, Dickinson and Company, Beckman Coulter Inc (Danaher Corporation), Bio-Rad Laboratories, Bruker Corporation, and T2 Biosystems, Inc. Companies operating in the sepsis diagnostics market focus on multiple strategies to strengthen market position and expand global reach. Continuous investment in research and development enables faster, more sensitive, and more accurate diagnostic solutions. Strategic collaborations with hospitals and research institutions support clinical validation and adoption. Many players expand product portfolios to include rapid and point-of-care testing platforms. Geographic expansion into emerging healthcare markets enhances revenue opportunities. Automation, digital integration, and workflow optimization are prioritized to improve laboratory efficiency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Test type trends

- 2.2.3 Product trends

- 2.2.4 Method trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in prevalence of infectious diseases

- 3.2.1.2 Increasing government initiatives towards infectious diseases

- 3.2.1.3 Technological advancements in infectious diseases diagnosis

- 3.2.1.4 Rising awareness regarding infectious diseases and its diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of sepsis diagnostics devices

- 3.2.2.2 Stringent regulatory framework

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with AI & digital health

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Test type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Blood culture media

- 5.3 Instruments

- 5.4 Assay kits & reagents

- 5.5 Software

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Microbiology

- 6.3 Molecular diagnostics

- 6.4 Immunoassays

- 6.5 Flow cytometry

Chapter 7 Market Estimates and Forecast, By Method type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Conventional diagnostics

- 7.3 Automated diagnostics

Chapter 8 Market Estimates and Forecast, By Pathogen type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Bacterial sepsis

- 8.3 Fungal sepsis

- 8.4 Other pathogen types

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Diagnostic centers

- 9.4 Clinics

- 9.5 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 F. Hoffmann-La Roche Ltd

- 11.2 Thermo Fisher Scientific

- 11.3 Abbott Laboratories

- 11.4 Beckman Coulter Inc

- 11.5 Siemens Healthineers

- 11.6 Becton, Dickinson and Company

- 11.7 bioMerieux SA

- 11.8 Bio-Rad Laboratories

- 11.9 Bruker Corporation

- 11.10 T2 Biosystems, Inc

全球脓毒症诊断市场规模、份额、趋势和成长分析报告(2026-2034年)败血症诊断市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034年)

全球脓毒症诊断市场规模、份额、趋势和成长分析报告(2026-2034年)败血症诊断市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034年) PCT快速检测套组市场按产品类型、疾病类型、技术、检体类型、最终用户和分销管道划分-全球预测(2026-2032年)

PCT快速检测套组市场按产品类型、疾病类型、技术、检体类型、最终用户和分销管道划分-全球预测(2026-2032年) 日本败血症诊断市场报告(按诊断、产品、检测方式、技术、病原体、最终用户和地区划分,2026-2034年)

日本败血症诊断市场报告(按诊断、产品、检测方式、技术、病原体、最终用户和地区划分,2026-2034年) 败血症诊断市场规模、份额和成长分析(按技术、应用、产品、方法、病原体类型、检测类型、最终用户和地区划分)—2026-2033年产业预测

败血症诊断市场规模、份额和成长分析(按技术、应用、产品、方法、病原体类型、检测类型、最终用户和地区划分)—2026-2033年产业预测 败血症诊断市场按产品类型、方法、病原体、技术、最终用户和地区划分

败血症诊断市场按产品类型、方法、病原体、技术、最终用户和地区划分 2025年全球败血症诊断市场报告

2025年全球败血症诊断市场报告 败血症诊断市场-全球产业规模、份额、趋势、机会和预测,按技术、产品、诊断方法、病原体、地区和竞争细分,2020 年至 2030 年

败血症诊断市场-全球产业规模、份额、趋势、机会和预测,按技术、产品、诊断方法、病原体、地区和竞争细分,2020 年至 2030 年 北美和欧洲败血症诊断市场:市场规模、份额、趋势分析(按产品、技术、病原体、测试方法、诊断方法、最终用途和国家)、细分市场预测(2025-2030 年)败血症诊断市场规模、份额、趋势分析报告:按产品、技术、病原体、测试、方法、最终用途、地区、细分预测,2025-2030 年

北美和欧洲败血症诊断市场:市场规模、份额、趋势分析(按产品、技术、病原体、测试方法、诊断方法、最终用途和国家)、细分市场预测(2025-2030 年)败血症诊断市场规模、份额、趋势分析报告:按产品、技术、病原体、测试、方法、最终用途、地区、细分预测,2025-2030 年