|

市场调查报告书

商品编码

1936641

雷射切割机市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Laser Cutting Machines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

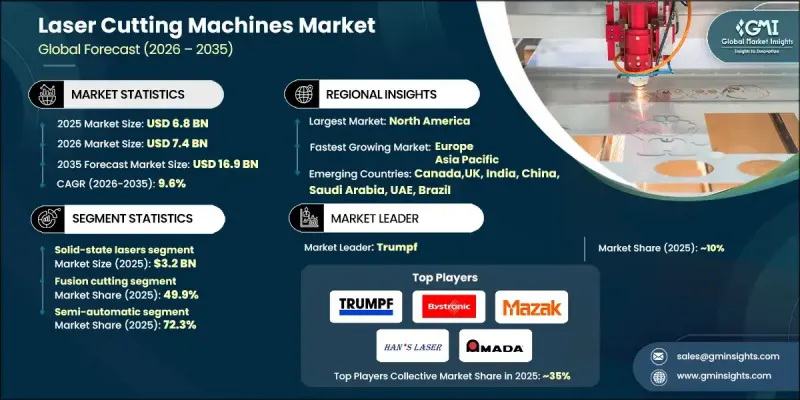

全球雷射切割机市场预计到 2025 年将达到 68 亿美元,到 2035 年将达到 169 亿美元,年复合成长率为 9.6%。

随着各行业製造商积极采用自动化技术和工业4.0实践,市场正在迅速扩张。雷射切割机正成为智慧工厂营运的核心,透过实现设备互联、即时监控和进阶分析,优化效率并透过预测性维护减少停机时间。这些机器能够无缝整合到自动化工作流程中,提供微米级精度、高品质且后处理极少的精确切割。汽车、航太、电子和工业机械等行业的需求不断增长,推动了市场成长。这些产业需要轻量化、复杂且精密的组装,而传统切割方法无法一致地实现这一目标。雷射系统能够实现干净俐落的边缘和卓越的几何精度,从而提高生产效率并减少材料浪费,使其成为现代製造业不可或缺的工具。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 68亿美元 |

| 预测金额 | 169亿美元 |

| 复合年增长率 | 9.6% |

预计到2025年,固体雷射器市场规模将达到32亿美元,并在2026年至2035年间以10%的复合年增长率成长。与传统的气体雷射系统相比,固体雷射器,尤其是光纤雷射和碟片雷射,因其卓越的光束品质、快速的切割速度、低营运成本和高能源效率而备受青睐。这些特性使其非常适合高精度工业应用和全自动生产线。固体雷射正被广泛应用于金属加工、汽车、航太和电子製造等众多产业,协助数位转型并提升工业效率。

预计到2025年,熔切市场份额将达到49.9%,并在2035年之前以9.9%的复合年增长率成长。熔切凭藉其多功能性、高速性、高精度、可加工多种金属以及切割边缘光滑(最大限度减少后处理)等优点,仍然是首选的加工方法。其高效性满足了汽车、航太、电子和工业製造等行业对减少材料废弃物、提高公差和简化生产流程的需求。

美国雷射切割机市场预计到2025年将达到19亿美元,2026年至2035年的复合年增长率(CAGR)为9.8%。汽车、航太、电子和金属加工等产业对精密切割零件和复杂设计的强劲需求是推动市场成长的主要动力。雷射光源、软体整合和自动化功能的持续技术创新,促进了雷射切割机的广泛应用,并鼓励製造商升级和扩展现有系统。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 产业影响因素

- 司机

- 自动化和工业4.0的日益普及

- 高精度加工的需求日益增长

- 向节能型光纤和固体雷射过渡

- 对减少材料废弃物和提高生产力的需求

- 产业潜在风险与挑战

- 高昂的营运和维护成本

- 材料限制与加工挑战

- 司机

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 透过技术

- 监管环境

- 标准和合规要求

- 区域法规结构

- 认证标准

- 贸易统计

- 主要进口国

- 主要出口国

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 按技术分類的市场估算与预测,2022-2035年

- 固体雷射

- 气体雷射

- 半导体雷射

第六章 依製造流程分類的市场估算与预测,2022-2035年

- 熔切

- 火焰切割

- 热昇华切割

第七章 依功能类型分類的市场估计与预测,2022-2035年

- 半自动

- 机器人技术

第八章 按应用领域分類的市场估算与预测,2022-2035年

- 车

- 家用电子电器

- 国防和航太

- 工业的

- 其他(医疗、能源/电力等)

第九章 按分销管道分類的市场估算与预测,2022-2035年

- 直销

- 间接销售

第十章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 印尼

- 马来西亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

第十一章:公司简介

- Amada

- Bystronic

- Coherent

- Epilog Laser

- Han's Laser

- IPG Photonics

- Jenoptik

- LVD Company

- Mazak Optonics

- Mitsubishi Electric Corporation

- Prima Power

- Tanaka

- Trotec Laser

- Trumpf

- Universal Laser Systems

The Global Laser Cutting Machines Market was valued at USD 6.8 billion in 2025 and is estimated to grow at a CAGR of 9.6% to reach USD 16.9 billion by 2035.

The market is experiencing rapid expansion as manufacturers across industries increasingly adopt automation technologies and Industry 4.0 practices. Laser cutting machines are becoming central to smart factory operations, enabling connected equipment, real-time monitoring, and advanced analytics to optimize efficiency and reduce downtime through predictive maintenance. These machines allow seamless integration into automated workflows, delivering precise, high-quality cuts with micron-level accuracy and minimal post-processing. Rising demand from automotive, aerospace, electronics, and industrial machinery sectors is driving growth, as these industries require lightweight, complex, and intricately assembled components that conventional cutting methods cannot achieve consistently. The ability of laser systems to produce clean edges and superior geometric accuracy enhances productivity while reducing material waste, making them indispensable for modern manufacturing.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.8 Billion |

| Forecast Value | $16.9 Billion |

| CAGR | 9.6% |

The solid-state lasers segment generated USD 3.2 billion in 2025 and is expected to grow at a CAGR of 10% from 2026 to 2035. The solid-state segment, particularly fiber and disk lasers, is favored due to superior beam quality, faster cutting speeds, lower operating costs, and enhanced energy efficiency compared with traditional gas-based systems. These characteristics make them highly suitable for high-precision industrial operations and fully automated production lines. Solid-state lasers are increasingly adopted across metal fabrication, automotive, aerospace, and electronics manufacturing, supporting digital transformation and industrial efficiency.

The fusion cutting segment held a 49.9% share in 2025 and is anticipated to grow at a CAGR of 9.9% through 2035. Fusion cutting remains the preferred method due to its versatility, high speed, precision, and ability to handle a wide range of metals while producing smooth edges that require minimal post-processing. Its efficiency aligns with industry needs for reduced material waste, tighter tolerances, and streamlined production in automotive, aerospace, electronics, and industrial manufacturing sectors.

U.S. Laser Cutting Machines Market reached USD 1.9 billion in 2025 and is expected to grow at a CAGR of 9.8% between 2026 and 2035. Strong demand from industries requiring precision-cut components and complex designs, such as automotive, aerospace, electronics, and metal fabrication, is driving growth. Continuous technological advancements in laser sources, software integration, and automation capabilities support widespread adoption and encourage manufacturers to upgrade or expand their existing systems.

Key players in the Global Laser Cutting Machines Market include Bystronic, Coherent, Mitsubishi Electric Corporation, IPG Photonics, Trumpf, Amada, Jenoptik, LVD Company, Tanaka, Mazak Optonics, Trotec Laser, Universal Laser Systems, Prima Power, Han's Laser, and Epilog Laser. Companies in the laser cutting machines market are employing multiple strategies to expand their market presence and maintain a competitive advantage. They are investing heavily in R&D to develop faster, more energy-efficient, and higher-precision laser systems that cater to diverse industrial applications. Strategic collaborations with OEMs and industrial integrators are being used to strengthen distribution networks and ensure seamless integration into smart factories. Manufacturers are expanding production capacity, introducing fiber and hybrid laser technologies, and enhancing software and automation compatibility to attract high-end clients.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Process

- 2.2.4 Function type

- 2.2.5 Application

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of automation & industry 4.0

- 3.2.1.2 Increasing demand for high-precision fabrication

- 3.2.1.3 Shift toward energy-efficient fiber & solid-state lasers

- 3.2.1.4 Demand for reduced material waste & higher productivity

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High operational & maintenance expenses

- 3.2.2.2 Material limitations & processing challenges

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By technology

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Solid-state lasers

- 5.3 Gas lasers

- 5.4 Semiconductor laser

Chapter 6 Market Estimates & Forecast, By Process, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Fusion cutting

- 6.3 Flame cutting

- 6.4 Sublimation cutting

Chapter 7 Market Estimates & Forecast, By Function Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Semi-automatic

- 7.3 Robotic

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Consumer electronics

- 8.4 Defense and aerospace

- 8.5 Industrial

- 8.6 Others (medical, energy & power etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Amada

- 11.2 Bystronic

- 11.3 Coherent

- 11.4 Epilog Laser

- 11.5 Han's Laser

- 11.6 IPG Photonics

- 11.7 Jenoptik

- 11.8 LVD Company

- 11.9 Mazak Optonics

- 11.10 Mitsubishi Electric Corporation

- 11.11 Prima Power

- 11.12 Tanaka

- 11.13 Trotec Laser

- 11.14 Trumpf

- 11.15 Universal Laser Systems

雷射切割机市场:2026-2032年全球市场预测(依雷射类型、加工材料、功率范围、控制方式及应用划分)二维雷射切割机市场:按雷射类型、功率输出、应用、最终用户和销售管道,全球预测,2026-2032年FROG超短脉衝测量仪器市场:按雷射类型、技术、测量模式、销售管道、应用和最终用户划分,全球预测,2026-2032年超短脉衝雷射材料加工市场:按雷射配置、雷射类型、波长、系统类型、功率范围、应用和最终用户分類的全球预测(2026-2032年)

雷射切割机市场:2026-2032年全球市场预测(依雷射类型、加工材料、功率范围、控制方式及应用划分)二维雷射切割机市场:按雷射类型、功率输出、应用、最终用户和销售管道,全球预测,2026-2032年FROG超短脉衝测量仪器市场:按雷射类型、技术、测量模式、销售管道、应用和最终用户划分,全球预测,2026-2032年超短脉衝雷射材料加工市场:按雷射配置、雷射类型、波长、系统类型、功率范围、应用和最终用户分類的全球预测(2026-2032年) 2026年全球雷射切割机市场报告

2026年全球雷射切割机市场报告 全球雷射切割机市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

全球雷射切割机市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 全球雷射切割机市场,2026-2030年雕刻笔市场:按技术、电源、应用、最终用户和分销管道划分,全球预测(2026-2032年)

全球雷射切割机市场,2026-2030年雕刻笔市场:按技术、电源、应用、最终用户和分销管道划分,全球预测(2026-2032年) 雷射切割机市场-全球产业规模、份额、趋势、机会及预测(依技术、製程、最终用户、地区及竞争格局划分,2021-2031年预测)

雷射切割机市场-全球产业规模、份额、趋势、机会及预测(依技术、製程、最终用户、地区及竞争格局划分,2021-2031年预测) 低功率和中功率雷射切割控制器:全球市场份额和排名、总收入和需求预测(2025-2031年)

低功率和中功率雷射切割控制器:全球市场份额和排名、总收入和需求预测(2025-2031年)