|

市场调查报告书

商品编码

1936647

电动出行设备市场机会、成长要素、产业趋势分析及2026年至2035年预测Powered Mobility Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

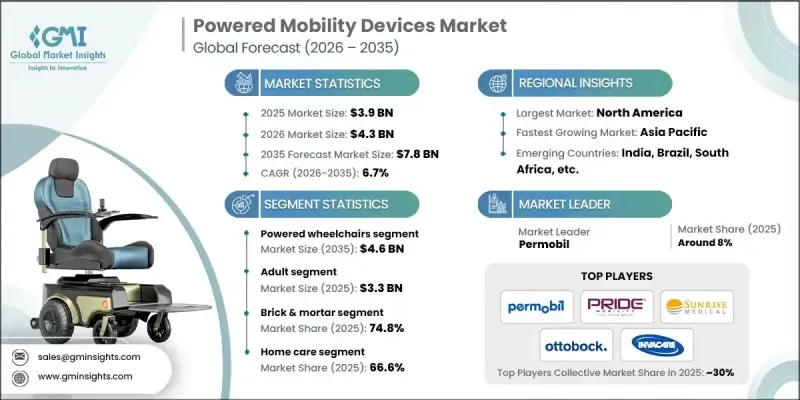

全球电动旅游设备市场预计到 2025 年将达到 39 亿美元,到 2035 年将达到 78 亿美元,年复合成长率为 6.7%。

市场成长的驱动因素包括行动不便疾病的日益增多以及老年人口的不断扩大,老年人越来越依赖电动代步设备来维持独立的日常生活。与基础型代步工具不同,电动代步设备正迅速迈向智慧医疗设备领域,製造商不断整合长续航电池系统、高效率马达、符合人体工学的座椅系统以及可程式设计控制设备等功能,从而提升舒适度并减轻看护者的负担。居家照护的普及也推动了市场的发展。患者及其家人越来越倾向于选择实用且便利的代步解决方案,帮助老年人继续在熟悉的环境中生活,减少往返养老机构的次数,并确保室内外活动的安全性。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 39亿美元 |

| 预测金额 | 78亿美元 |

| 复合年增长率 | 6.7% |

从产品和市场接受度来看,市场受益于各种严重程度的需求,从需要持续电力支援的使用者到寻求辅助设备的使用者。与关节炎、中风后遗症、脊髓损伤和神经退化性疾病通常需要长期可靠的行动辅助,而非短期復健支持。技术进步也是推动需求成长的因素。现代设备越来越注重轻量化材料、更高的操控性和安全性,例如智慧煞车、座椅个人化调节、防跌倒和稳定性控制,从而推动电动代步设备不仅在医疗机构中,而且在日常生活中广泛应用。

预计到2025年,电动轮椅市场规模将达到46亿美元。对于行动严重受限或进行性行动能力的使用者而言,电动轮椅仍然是他们的首选解决方案。这些用户需要先进的操控功能、强大的姿势支撑以及在室内外环境中可靠的性能。随着照护模式逐渐转向家庭,舒适性、可靠性和个人化与临床规格同等重要,电动轮椅产品在驱动机制、座椅模组和安全系统等方面的差异化程度日益提高,并受到越来越多的关注。

到2025年,居家照护市占率将达到66.6%,这主要得益于老年人倾向于留在熟悉的住宅环境中、慢性病盛行率不断上升,以及住宅生活便利性(对日常生活、安全和独立性至关重要)的需求。此外,设备易用性的提升也推动了居家照护需求的成长,例如设备面积小巧、室内转弯半径更小、操作智慧以及充电便利等。同时,送货上门、安装和维护等服务模式也有助于减少老年人和看护者使用设备的障碍,为他们提供轻鬆便捷的使用体验。

预计到2025年,北美电动出行设备市占率将达到41.3%,主要得益于更完善的医疗基础设施、更高的行动障碍疾病诊断和治疗率,以及相对良好的报销途径和成熟的復健/居家照护体系。此外,该地区市场实力的增强也得益于技术先进设备的快速普及,这些设备强调安全性、互联性和舒适性。医疗专业人员和消费者都非常重视这些特性,他们期望这些设备能够实际改善日常生活功能和生活品质。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 产业影响因素

- 司机

- 神经系统疾病呈上升趋势

- 动力移动产品的技术进步

- 老年人口比例不断增加

- 全球残障人数呈上升趋势

- 产业潜在风险与挑战

- 电动轮椅高成本

- 严格的法规结构

- 机会

- 专注于轻量折迭式电动轮椅

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价值链分析

- 救赎方案

- 消费行为与趋势

- 2025年产品类型价格分析

- 波特五力分析

- PESTEL 分析

- 差距分析

- 未来市场趋势

第四章 竞争情势

- 介绍

- 企业矩阵分析

- 公司市占率分析

- 世界

- 北美洲

- 欧洲

- 亚太地区

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 依产品类型分類的市场估算与预测,2022-2035年

- 电动轮椅

- 后轮驱动轮椅

- 中轮驱动轮椅

- 前轮驱动轮椅

- 组合式驱动轮椅

- 电动代步Scooter

- 三轮行动装置

- 四轮行动装置

- 动力附加元件或辅助推进装置

第六章 依病患类型分類的市场估计与预测,2022-2035年

- 成人版

- 儿童

7. 2022-2035年按分销管道分類的市场估算与预测

- 实体店面

- 线上管道

第八章 依最终用途分類的市场估算与预测,2022-2035年

- 居家照护

- 復健中心

- 医院

- 其他最终用户

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- Airwheel

- Callidai Motor Works

- Decon

- DriveDeVilbiss Healthcare

- Frido

- Golden Technologies

- INVACARE

- Karman Healthcare

- LEVO

- Merits Health Products

- MEYRA

- Ostrich Mobility Instruments

- Ottobock

- Permobil

- Pride Mobility

- Sunrise medical

The Global Powered Mobility Devices Market was valued at USD 3.9 billion in 2025 and is estimated to grow at a 6.7% CAGR to reach USD 7.8 billion by 2035.

Market growth is supported by the rising prevalence of mobility-impairing conditions and the expanding elderly population that increasingly depends on powered assistance to preserve independence and day-to-day function. Unlike basic mobility aids, powered mobility devices are moving quickly into the smart medical device lane, as manufacturers integrate longer-range battery systems, more efficient motors, ergonomic seating systems, and programmable controls that improve comfort and reduce caregiver strain. The market's momentum is also reinforced by the broader shift toward home-based care, where patients and families prefer practical mobility solutions that support aging-in-place, reduce repeated facility visits, and enable safer indoor/outdoor navigation.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.9 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 6.7% |

From a product and adoption perspective, the market is benefiting from demand across a wide severity range, from users who need full-time powered support to those who want a boost through add-on units. Clinical need is rising with chronic conditions such as arthritis, post-stroke impairments, spinal cord injuries, and neurodegenerative disorders, which often require long-term, reliable mobility assistance rather than short-duration rehabilitation support. Technology is also helping unlock demand: modern devices increasingly emphasize lightweight materials, better maneuverability, intelligent braking, improved seating customization, and safety-oriented features that reduce falls and enhance stability, making powered mobility devices more acceptable for everyday use, not only in institutional settings.

The powered wheelchairs segment generated USD 4.6 billion in 2025, as it remains the preferred solution for users with severe or progressive mobility limitations who need advanced control options, stronger postural support, and consistent performance across indoor and outdoor environments. These products are increasingly differentiated by drive options, seating modules, and safety systems, and they are gaining further traction as more care pathways move into the home, where comfort, reliability, and customization matter as much as clinical specifications.

The home care segment held 66.6% share in 2025, driven by aging-in-place preferences, growing chronic disease prevalence, and the need for convenient mobility within residential environments where daily routine, safety, and independence are the non-negotiables. Home care demand is also supported by improvements in device usability, such as compact footprints, improved turning radius for indoor navigation, smarter controls, and easier charging, while service models (delivery, installation, maintenance) help reduce barriers for older adults and caregivers who want a low-friction ownership experience.

North America Powered Mobility Devices Market held 41.3% share in 2025, anchored by stronger healthcare infrastructure, higher diagnosis and treatment rates for mobility-impairing conditions, and relatively better access through reimbursement pathways and established rehabilitation/home-care ecosystems. The region's market strength is also reinforced by faster adoption of technology-forward devices that emphasize safety, connectivity, and comfort features that resonate strongly with both clinicians and consumers who expect measurable improvements in daily functioning and quality of life.

Key players involved in the Global Powered Mobility Devices Market include Airwheel, Callidai Motor Works, Decon, Drive DeVilbiss Healthcare, Frido, Golden Technologies, INVACARE, Karman Healthcare, LEVO, Merits Health Products, MEYRA, Ostrich Mobility Instruments, Ottobock, Permobil, Pride Mobility, Sunrise Medical. Companies are strengthening their market foothold by accelerating product innovation, lightweight/foldable designs, improved battery performance, and smarter controls that enhance safety and comfort for home use. They are also widening access through multi-channel distribution, combining clinician-led brick-and-mortar fitting and service with faster-growing online models that improve reach into underserved geographies. To improve conversion and retention, leading players bundle devices with after-sales maintenance, training, and customization (seating, controls, accessories), reducing user anxiety and improving long-term satisfaction.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Patient trends

- 2.2.4 Distribution channel trends

- 2.2.5 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of neurological diseases

- 3.2.1.2 Technological advancements in powered mobility products

- 3.2.1.3 Rising percentage of geriatric population

- 3.2.1.4 Increasing prevalence of disabilities worldwide

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of powered wheelchairs

- 3.2.2.2 Stringent regulatory framework

- 3.2.3 Opportunities

- 3.2.3.1 Focus on lightweight and foldable electric wheelchairs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Value chain analysis

- 3.7 Reimbursement scenario

- 3.8 Consumer behavior and trends

- 3.9 Pricing analysis, by product type, 2025

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Powered wheelchairs

- 5.2.1 Rear-wheel drive wheelchairs

- 5.2.2 Mid-wheel drive wheelchairs

- 5.2.3 Front-wheel drive wheelchairs

- 5.2.4 Combination-drive wheelchairs

- 5.3 Power mobility scooters

- 5.3.1 3-wheel devices

- 5.3.2 4-wheel devices

- 5.4 Power add-on or propulsion-assist units

Chapter 6 Market Estimates and Forecast, By Patient, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Brick & mortar

- 7.3 Online channel

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Home care

- 8.3 Rehabilitation centers

- 8.4 Hospitals

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Airwheel

- 10.2 Callidai Motor Works

- 10.3 Decon

- 10.4 DriveDeVilbiss Healthcare

- 10.5 Frido

- 10.6 Golden Technologies

- 10.7 INVACARE

- 10.8 Karman Healthcare

- 10.9 LEVO

- 10.10 Merits Health Products

- 10.11 MEYRA

- 10.12 Ostrich Mobility Instruments

- 10.13 Ottobock

- 10.14 Permobil

- 10.15 Pride Mobility

- 10.16 Sunrise medical

第二类电动旅游设备市场:依产品类型、电池类型、应用、最终用户和通路划分-2026-2032年全球市场预测电动出行设备市场:2026-2032年全球市场预测(依设备类型、推进方式、应用、最终用户及通路划分)

第二类电动旅游设备市场:依产品类型、电池类型、应用、最终用户和通路划分-2026-2032年全球市场预测电动出行设备市场:2026-2032年全球市场预测(依设备类型、推进方式、应用、最终用户及通路划分) 亚太地区「未来工厂」行动解决方案市场:按最终用户产业、车辆类型、解决方案类型、部署模式和国家分類的分析和预测(2025-2035 年)

亚太地区「未来工厂」行动解决方案市场:按最终用户产业、车辆类型、解决方案类型、部署模式和国家分類的分析和预测(2025-2035 年) 欧洲「未来工厂」出行解决方案市场:按最终用户产业、车辆类型、解决方案类型、部署模式和国家划分-分析与预测(2025-2035 年)

欧洲「未来工厂」出行解决方案市场:按最终用户产业、车辆类型、解决方案类型、部署模式和国家划分-分析与预测(2025-2035 年) 新兴市场出行创新:2034 年市场预测-按交通方式、服务模式、技术和区域分類的全球分析互联出行安全与网路安全市场预测至2034年:依解决方案类型、车辆类型、部署模式、安全层级与区域分類的全球分析全自主互联轨道运输系统市场:系统元件、车辆类型、通讯技术、运行模式和应用划分-全球预测,2026-2032年

新兴市场出行创新:2034 年市场预测-按交通方式、服务模式、技术和区域分類的全球分析互联出行安全与网路安全市场预测至2034年:依解决方案类型、车辆类型、部署模式、安全层级与区域分類的全球分析全自主互联轨道运输系统市场:系统元件、车辆类型、通讯技术、运行模式和应用划分-全球预测,2026-2032年 2026年全球电动出行设备市场报告2026年全球连网自动驾驶汽车市场报告

2026年全球电动出行设备市场报告2026年全球连网自动驾驶汽车市场报告 面向未来工厂的行动解决方案市场—全球及区域分析(按最终用户产业、车辆类型、解决方案类型、部署模式和国家划分)—分析与预测(2025-2035 年)

面向未来工厂的行动解决方案市场—全球及区域分析(按最终用户产业、车辆类型、解决方案类型、部署模式和国家划分)—分析与预测(2025-2035 年)