|

市场调查报告书

商品编码

1936648

生物过程分析仪器市场机会、成长要素、产业趋势分析及2026年至2035年预测Bioprocess Analyzers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

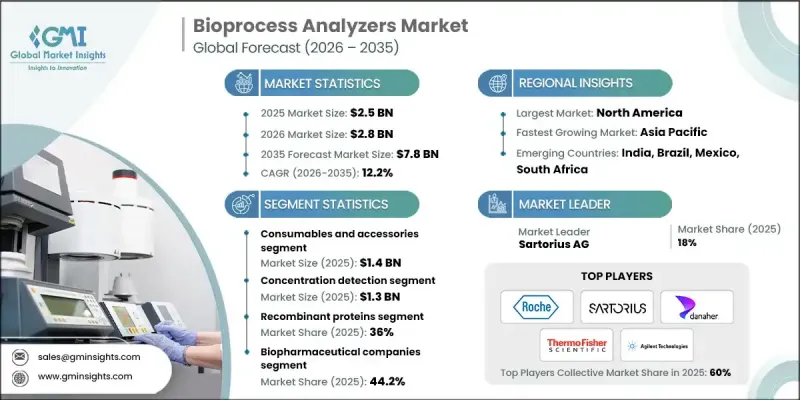

全球生物过程分析仪市场预计到 2025 年将达到 25 亿美元,到 2035 年将达到 78 亿美元,年复合成长率为 12.2%。

生物製药产业的强劲成长得益于市场对生物製药产品需求的不断增长、生物加工技术的进步、生物相似药生产的扩张以及政府的大力主导和资金投入。生物製程分析仪器是专门用于监测和测量整个生产过程中关键参数的仪器,确保符合监管标准,同时维持产品品质和疗效。随着癌症、糖尿病和心血管疾病等慢性疾病的日益普遍,对先进、标靶和个人化疗法的需求也随之飙升。这些治疗方法需要精确的製程控制,以确保安全性、有效性和符合监管要求,从而推动了即时分析仪器在监测基材、代谢物和产物浓度方面的广泛应用。此外,政府支持计画、研究经费以及公私合营也为高性能分析仪器的应用创造了有利环境,进一步加速了其在生物製药产业的市场渗透。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 25亿美元 |

| 预测金额 | 78亿美元 |

| 复合年增长率 | 12.2% |

预计到2025年,耗材及配件市场收入将达到14亿美元,并在2026年至2035年间以12.1%的复合年增长率成长。这些组件,例如一次性感测器、样品管、过滤器、校准试剂盒和分析试剂,对于确保操作顺畅、符合法规要求以及製程完整性至关重要。自动化和连续生物製程的兴起显着增加了对与先进分析设备相容的耗材的需求,从而实现了高通量工作流程,同时减少了人工干预和操作失误。

2025年,浓度检测领域的市场规模达到13亿美元,预计2035年将以12.2%的复合年增长率成长。浓度检测分析仪能够高精度地测量生产过程中蛋白质、抗体和其他生物製药等关键成分。紫外-可见光光谱、拉曼光谱和可变光程系统等技术无需繁琐的样品製备即可即时监测。生物製药和生物相似药生产中优化产量、减少批次废品率和提高整体效率的需求,正在推动这些技术的应用。

预计到2025年,美国生物製程分析设备市场规模将达到8.602亿美元。该地区引领北美市场,主要受慢性病发病率上升以及生物製药和个人化医疗需求成长的推动。这种不断增长的需求正促使企业加快对先进分析设备的投资,以确保生产效率、维持产品品质并满足严格的监管标准。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 产业影响因素

- 司机

- 生物製药产品需求不断成长

- 生物技术和生物加工的进展

- 生物相似药需求不断成长

- 政府加大主导和资金投入

- 产业潜在风险与挑战

- 设备高成本

- 复杂性和技术专长

- 市场机会

- 新兴市场的成长

- 高级数据分析和人工智慧集成

- 司机

- 成长潜力分析

- 监管环境

- 技术进步

- 当前技术趋势

- 新兴技术

- 供应链分析

- 救赎方案

- 2024年定价分析

- 未来市场趋势

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 合作伙伴关係和合资企业

- 新产品发布

- 扩张计划

第五章 2022-2035年按产品分類的市场估算与预测

- 装置

- 耗材和配件

第六章 依分析类型分類的市场估计与预测,2022-2035年

- 基材分析

- 代谢物分析

- 浓度检测

第七章 按应用领域分類的市场估算与预测,2022-2035年

- 抗生素

- 重组蛋白

- 生物相似药

- 其他用途

第八章 依最终用途分類的市场估算与预测,2022-2035年

- 生物製药公司

- 合约研究组织 (CRO) 和合约生产组织 (CMO)

- 研究和学术机构

- 其他最终用途

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第十章:公司简介

- 4BioCell GmbH &Co. KG

- Agilent Technologies, Inc.

- Beckman Coulter Life Sciences

- Danaher Corporation

- Endress+Hauser Group Services AG

- Eppendorf AG

- F. Hoffmann-La Roche Ltd.

- Nova Biomedical

- Randox Laboratories Ltd.

- Sartorius AG

- Solida Biotech GmbH

- SYSBIOTECH GmbH

- Thermo Fisher Scientific Inc.

- Waters Corporation

- Xylem Inc.

The Global Bioprocess Analyzers Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 12.2% to reach USD 7.8 billion by 2035.

The robust growth is fueled by rising demand for biopharmaceutical products, technological advancements in bioprocessing, increasing production of biosimilars, and strong governmental initiatives and funding. Bioprocess analyzers are specialized instruments that monitor and measure key parameters throughout the manufacturing process, ensuring compliance with regulatory standards while maintaining product quality and efficacy. As chronic diseases like cancer, diabetes, and cardiovascular disorders become more prevalent, the demand for advanced, targeted, and personalized therapies is surging. These therapies require precise process control to guarantee safety, effectiveness, and regulatory adherence, driving widespread adoption of real-time analyzers for monitoring substrates, metabolites, and product concentrations. Additionally, supportive government programs, funding for research, and public-private partnerships provide a favorable environment for integrating high-performance analyzers, further accelerating market adoption across the biopharmaceutical industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 12.2% |

The consumables and accessories segment generated USD 1.4 billion in 2025 and is anticipated to grow at a CAGR of 12.1% through 2026-2035. These components, including disposable sensors, sample tubes, filters, calibration kits, and analytical reagents, are crucial for smooth operation, regulatory compliance, and process integrity. The rise of automation and continuous bioprocessing has significantly increased the demand for consumables compatible with advanced analyzers, enabling high-throughput workflows while reducing manual interventions and operational errors.

The concentration detection segment accounted for USD 1.3 billion in 2025 and is expected to grow at a CAGR of 12.2% through 2035. Concentration detection analyzers measure critical components such as proteins, antibodies, and other biologics during production with high precision. Technologies such as UV-Vis spectroscopy, Raman spectroscopy, and variable pathlength systems allow real-time monitoring without extensive sample preparation. Increasing adoption is driven by the need to optimize yields, minimize batch failures, and improve overall efficiency in biologics and biosimilar production.

U.S. Bioprocess Analyzers Market reached USD 860.2 million in 2025. The region leads North America, supported by the growing prevalence of chronic illnesses and the rising demand for biologics and personalized medicine. This demand is prompting companies to invest in advanced analyzers that ensure production efficiency, maintain quality, and adhere to strict regulatory standards.

Key players operating in the Global Bioprocess Analyzers Market include Nova Biomedical, Thermo Fisher Scientific Inc., 4BioCell GmbH & Co. KG, Sartorius AG, Danaher Corporation, Waters Corporation, Beckman Coulter Life Sciences, F. Hoffmann-La Roche Ltd., Agilent Technologies, Inc., SYSBIOTECH GmbH, Endress+Hauser Group Services AG, Solida Biotech GmbH, Xylem Inc., Eppendorf AG, and Randox Laboratories Ltd. Companies in the bioprocess analyzers market are strengthening their position through multiple strategies. They are investing heavily in research and development to improve analyzer accuracy, integration, and automation compatibility. Strategic collaborations and partnerships with pharmaceutical and biotechnology firms allow access to emerging markets and specialized applications. Firms are also focusing on expanding their product portfolios, offering consumables and accessories to complement analyzers for complete process solutions. Geographic expansion, especially into emerging regions with growing biopharmaceutical sectors, is another key approach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Analysis type trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for biopharmaceutical products

- 3.2.1.2 Advancements in biotechnology and bioprocessing

- 3.2.1.3 Increasing demand for biosimilars

- 3.2.1.4 Rising government initiatives and funding

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of instruments

- 3.2.2.2 Complexity and technical expertise

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in emerging markets

- 3.2.3.2 Integration with advanced data analytics and AI

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.9 Future market trends

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Instruments

- 5.3 Consumables and accessories

Chapter 6 Market Estimates and Forecast, By Analysis Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Substrate analysis

- 6.3 Metabolite analysis

- 6.4 Concentration detection

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Antibiotics

- 7.3 Recombinant proteins

- 7.4 Biosimilars

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Biopharmaceutical companies

- 8.3 CROs and CMOs

- 8.4 Research and academic institutes

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 4BioCell GmbH & Co. KG

- 10.2 Agilent Technologies, Inc.

- 10.3 Beckman Coulter Life Sciences

- 10.4 Danaher Corporation

- 10.5 Endress+Hauser Group Services AG

- 10.6 Eppendorf AG

- 10.7 F. Hoffmann-La Roche Ltd.

- 10.8 Nova Biomedical

- 10.9 Randox Laboratories Ltd.

- 10.10 Sartorius AG

- 10.11 Solida Biotech GmbH

- 10.12 SYSBIOTECH GmbH

- 10.13 Thermo Fisher Scientific Inc.

- 10.14 Waters Corporation

- 10.15 Xylem Inc.