|

市场调查报告书

商品编码

1936678

医疗半导体市场机会、成长要素、产业趋势分析及2026年至2035年预测Healthcare Semiconductor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球医疗半导体市场预计到 2025 年将达到 609 亿美元,到 2035 年将达到 1,617 亿美元,年复合成长率为 10.4%。

市场成长主要受以下因素驱动:人工智慧 (AI) 和机器学习 (ML) 在医疗保健领域的快速应用、慢性病盛行率的上升以及医疗保健IT基础设施投资的不断增长。穿戴式健康设备、远端患者监护解决方案以及小型化、携带式医疗技术的需求也在激增。先进半导体在加速数据处理、提高诊断准确性以及建立智慧医疗系统方面发挥关键作用。特别是远距监护和穿戴式装置的广泛应用,正在推动半导体技术的发展,从而实现对患者的持续追踪、高效的慢性病管理以及改善治疗效果。随着医疗设备日益互联且功能强大,半导体技术作为人工智慧诊断、远端医疗解决方案和智慧医疗设备的基础,至关重要。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 起始值 | 609亿美元 |

| 预测金额 | 1617亿美元 |

| 复合年增长率 | 10.4% |

预计到2025年,积体电路(IC)市占率将达到35.4%。积体电路仍然是医疗半导体产业的核心,因为它们为医疗设备提供紧凑、高效能的解决方案,从而实现精准诊断、监控以及整个医疗保健系统的无缝连接。这些晶片对于驱动小型、节能的设备至关重要,这些设备可以与医疗物联网(IoMT)和其他互联医疗平台整合。

预计到2025年,医疗影像领域将占据31.9%的市场。半导体技术在医疗影像系统中至关重要,它能够确保高解析度影像、更快地获取诊断资讯并改善治疗方案的发展。半导体技术的进步推动了节能高效成像设备的研发,这些设备能够提供精准的诊断,使医疗机构能够提供更快捷、更可靠的医疗服务。

预计到2025年,北美医疗半导体市占率将达到35.2%。该地区的成长主要得益于政府的医疗保健政策、对医疗研究的大量投资以及对远端医疗和数位医疗解决方案的强劲需求。此外,不断涌现的创新、先进的医疗基础设施以及日益增长的老龄人口带来的医疗需求也为市场发展提供了支持。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 生态系分析

- 产业影响因素

- 司机

- 人工智慧 (AI) 和机器学习 (ML) 在医疗保健领域的兴起

- 慢性病发生率呈上升趋势

- 增加对医疗资讯科技的投资

- 对穿戴式健康设备和远端患者监护的需求不断增长

- 小型化和便携化的发展趋势

- 挑战与困难

- 科技快速过时

- 隐私和安全问题

- 市场机会

- 个人化医疗的进展

- 扩大远端医疗服务

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 永续性措施

- 消费者心理分析

- 专利和智慧财产权分析

- 地缘政治和贸易趋势

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 地理分布比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年主要发展动态

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张与投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/Start-Ups竞赛的趋势

第五章 按组件分類的市场估算与预测,2022-2035年

- 积体电路(IC)

- 记忆

- MPU

- 逻辑积体电路

- 类比IC

- 微型计算机

- 感应器

- 光学感测器

- 压力感测器

- 温度感测器

- 其他的

- 离散组件

- 光电器件

第六章 按应用领域分類的市场估算与预测,2022-2035年

- 医学影像诊断

- X射线系统

- 电脑断层扫描(CT)扫描仪

- 磁振造影(MRI)系统

- 其他的

- 病患监测

- 诊断设备

- 穿戴式装置

- 智慧型手錶和穿戴式监测器

- 连接式心电图监测仪

- 其他的

- 其他的

- 復健设备

- 远端医疗

- 植入式医疗设备

- 其他的

第七章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第八章 公司简介

- 主要企业

- Intel Corporation

- Texas Instruments Incorporated

- STMicroelectronics NV

- NXP Semiconductors NV

- Analog Devices, Inc.

- 按地区分類的主要企业

- 北美洲

- Qualcomm Incorporated

- Broadcom Inc.

- Micron Technology, Inc.

- 亚太地区

- ON Semiconductor

- Samsung Electronics Co., Ltd.

- Taiwan Semiconductor Manufacturing Company Limited

- 欧洲

- Infineon Technologies AG

- ams OSRAM AG

- Renesas Electronics Corporation

- 北美洲

- 小众玩家/颠覆者

- SK hynix Inc.

- NVIDIA Corporation

- Microchip Technology Incorporated

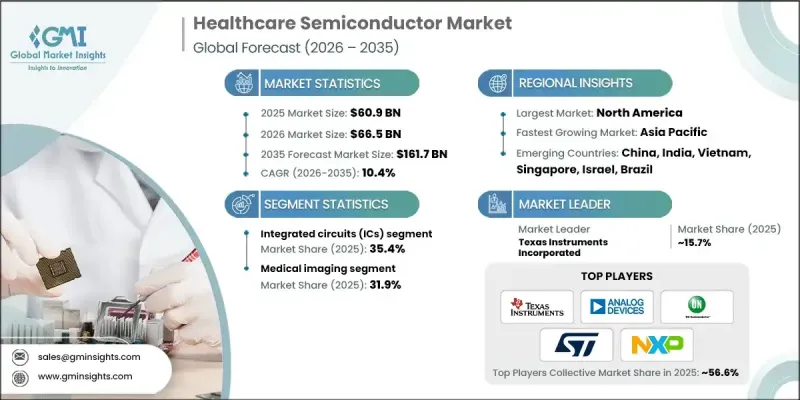

The Global Healthcare Semiconductor Market was valued at USD 60.9 billion in 2025 and is estimated to grow at a CAGR of 10.4% to reach USD 161.7 billion by 2035.

Growth in the market is fueled by the rapid adoption of artificial intelligence (AI) and machine learning (ML) in healthcare, the rising incidence of chronic diseases, and increasing investments in healthcare IT infrastructure. There is also surging demand for wearable health devices, remote patient monitoring solutions, and miniaturized, portable healthcare technology. Advanced semiconductors play a crucial role in enabling faster data processing, enhancing diagnostic accuracy, and supporting intelligent healthcare systems. The expansion of remote monitoring and wearable devices is particularly driving semiconductor adoption, allowing continuous patient tracking, efficient chronic disease management, and improved patient outcomes. As medical devices become more interconnected and high-performance, semiconductors are essential for powering AI-enabled diagnostics, telehealth solutions, and smart medical instrumentation.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $60.9 Billion |

| Forecast Value | $161.7 Billion |

| CAGR | 10.4% |

The integrated circuits (ICs) segment accounted for 35.4% share in 2025. Integrated circuits remain central to the healthcare semiconductor landscape as they provide compact, high-performance solutions for medical devices, enabling precise diagnostics, monitoring, and seamless connectivity across healthcare systems. These chips are crucial in supporting smaller, energy-efficient devices that can integrate with the Internet of Medical Things (IoMT) and other connected healthcare platforms.

The medical imaging segment held a 31.9% share in 2025. Semiconductor technologies are critical in medical imaging systems, ensuring high-resolution images, rapid access to diagnostic information, and improved treatment planning. Semiconductor advancements support the development of energy-efficient, high-performance imaging devices capable of accurate diagnostics, enabling healthcare providers to deliver faster and more reliable care.

North America Healthcare Semiconductor Market held a 35.2% share in 2025. The growth in this region is driven by government healthcare initiatives, substantial investments in medical research, and strong demand for telehealth and digital healthcare solutions. The market is further supported by rising innovation, advanced healthcare infrastructure, and the increasing needs of a growing aging population.

Key players operating in the Global Healthcare Semiconductor Market include Intel Corporation, Texas Instruments Incorporated, STMicroelectronics N.V., NXP Semiconductors N.V., Analog Devices, Inc., Qualcomm Incorporated, Infineon Technologies AG, onsemi, Renesas Electronics Corporation, Broadcom Inc., Microchip Technology Incorporated, ams OSRAM AG, NVIDIA Corporation, Samsung Electronics Co., Ltd., SK hynix Inc., Taiwan Semiconductor Manufacturing Company Limited, and Micron Technology, Inc. Companies in the healthcare semiconductor market strengthen their presence through multiple strategic approaches. They heavily invest in research and development to create high-performance, energy-efficient, and miniaturized semiconductors that address evolving healthcare needs. Collaborations with medical device manufacturers and healthcare providers enable seamless integration into advanced diagnostic, wearable, and remote monitoring technologies. Geographic expansion into emerging markets helps tap growing demand for connected healthcare solutions, while innovation in AI and IoT-enabled semiconductor applications enhances product differentiation.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Component trends

- 2.2.2 Application trends

- 2.2.3 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry ecosystem analysis

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Emergence of artificial intelligence (AI) and machine learning (ML) in healthcare

- 3.3.1.2 Rising prevalence of chronic diseases

- 3.3.1.3 Increased investments in healthcare IT

- 3.3.1.4 Rising demand for wearable health devices and remote patient monitoring

- 3.3.1.5 Growing trend toward miniaturization and portability

- 3.3.2 Pitfalls and challenges

- 3.3.2.1 Rapid technological obsolescence

- 3.3.2.2 Privacy and security concerns

- 3.3.3 Market opportunities

- 3.3.3.1 Advancements in personalized medicine

- 3.3.3.2 Expansion of telemedicine services

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Emerging Business Models

- 3.10 Compliance Requirements

- 3.11 Sustainability Measures

- 3.12 Consumer Sentiment Analysis

- 3.13 Patent and IP analysis

- 3.14 Geopolitical and trade dynamics

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Integrated circuits (ICs)

- 5.2.1 Memory

- 5.2.2 MPUs

- 5.2.3 Logic ICs

- 5.2.4 Analog ICs

- 5.2.5 MCUs

- 5.3 Sensors

- 5.3.1 Optical sensors

- 5.3.2 Pressure sensors

- 5.3.3 Temperature sensors

- 5.3.4 Others

- 5.4 Discrete components

- 5.5 Optoelectronics

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Medical imaging

- 6.2.1 X-ray systems

- 6.2.2 Computed tomography (CT) scanners

- 6.2.3 Magnetic resonance imaging (MRI) systems

- 6.2.4 Others

- 6.3 Patient monitoring

- 6.4 Diagnostic equipment

- 6.5 Wearables

- 6.5.1 Smartwatches and wearable monitors

- 6.5.2 Connected ECG monitors

- 6.5.3 Others

- 6.6 Others

- 6.6.1 Rehabilitation devices

- 6.6.2 Telemedicine

- 6.6.3 Implantable medical devices

- 6.6.4 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Global Key Players

- 8.1.1 Intel Corporation

- 8.1.2 Texas Instruments Incorporated

- 8.1.3 STMicroelectronics N.V.

- 8.1.4 NXP Semiconductors N.V.

- 8.1.5 Analog Devices, Inc.

- 8.2 Regional key players

- 8.2.1 North America

- 8.2.1.1 Qualcomm Incorporated

- 8.2.1.2 Broadcom Inc.

- 8.2.1.3 Micron Technology, Inc.

- 8.2.2 Asia Pacific

- 8.2.2.1 ON Semiconductor

- 8.2.2.2 Samsung Electronics Co., Ltd.

- 8.2.2.3 Taiwan Semiconductor Manufacturing Company Limited

- 8.2.3 Europe

- 8.2.3.1 Infineon Technologies AG

- 8.2.3.2 ams OSRAM AG

- 8.2.3.3 Renesas Electronics Corporation

- 8.2.1 North America

- 8.3 Niche Players/Disruptors

- 8.3.1 SK hynix Inc.

- 8.3.2 NVIDIA Corporation

- 8.3.3 Microchip Technology Incorporated

全球半导体数位双胞胎市场预测至2034年:按组件、数位双胞胎类型、部署模式、技术、应用、最终用户和地区划分全球半导体无尘室先进材料市场预测至2034年:按组件、材料类型、等级、应用、最终用户和地区划分

全球半导体数位双胞胎市场预测至2034年:按组件、数位双胞胎类型、部署模式、技术、应用、最终用户和地区划分全球半导体无尘室先进材料市场预测至2034年:按组件、材料类型、等级、应用、最终用户和地区划分 2026年全球半导体及其他电子元件市场报告2026年全球半导体及相关装置市场报告2026年全球半导体晶片生态系统市场报告2026年全球半导体玻璃市场报告2026年全球半导体电镀系统市场报告2026年物联网半导体全球市场报告全球电子与半导体支出分析市场报告(2026 年版)

2026年全球半导体及其他电子元件市场报告2026年全球半导体及相关装置市场报告2026年全球半导体晶片生态系统市场报告2026年全球半导体玻璃市场报告2026年全球半导体电镀系统市场报告2026年物联网半导体全球市场报告全球电子与半导体支出分析市场报告(2026 年版) 半导体产业物流解决方案市场:2026-2032年全球预测(依物流服务类型、运输方式、解决方案类型、应用程式和最终用户划分)

半导体产业物流解决方案市场:2026-2032年全球预测(依物流服务类型、运输方式、解决方案类型、应用程式和最终用户划分)