|

市场调查报告书

商品编码

1959271

2026-2035年半导体製造领域含氟聚合物的市场机会、成长要素、产业趋势分析及预测Fluoropolymers in Semiconductor Manufacturing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

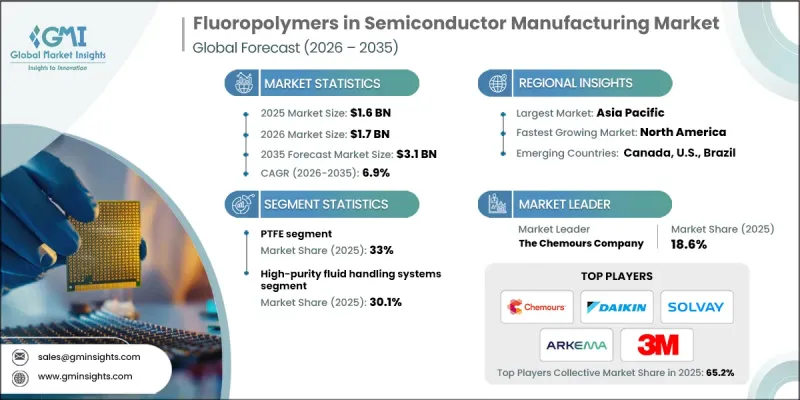

2025 年,半导体製造中使用的氟聚合物的全球市场价值为 16 亿美元,预计到 2035 年将达到 31 亿美元,年复合成长率为 6.9%。

半导体产业高度依赖具有优异耐化学性、热稳定性和电绝缘性能的含氟聚合物,这些性能对于製造先进装置至关重要。对更小、更快、更有效率的半导体的需求不断增长,进一步提升了对能够承受严苛製造环境的材料的需求。亚太地区目前主导市场,这得益于中国、韩国和台湾地区庞大的半导体製造能力以及对製造基础设施的持续投资。 5G、人工智慧和物联网 (IoT) 等技术的广泛应用,进一步推动了对先进半导体元件的需求。北美市场也正经历快速成长,这主要得益于极紫外线 (EUV) 和高数值孔径 (NA)微影术技术的日益普及。这些技术需要高性能的含氟聚合物材料,以在奈米尺度上提供化学保护和可靠的性能,从而确保更高的产量比率和装置效率。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 16亿美元 |

| 预测金额 | 31亿美元 |

| 复合年增长率 | 6.9% |

预计到2025年,聚四氟乙烯(PTFE)市占率将达到33%,并在2035年之前以7.6%的复合年增长率成长。半导体製造商青睐PTFE,是因为它具有无与伦比的耐化学性、耐高温性和优异的介电性。 PTFE在绝缘层、垫片和密封应用中发挥着至关重要的作用,它能够保护半导体装置免受严苛製造流程的影响,同时在关键应用中保持稳定的性能。

预计到2025年,高纯度流体处理系统市占率将达到30.1%。这些系统在半导体生产中至关重要,因为超洁净和精确的环境对于製造无缺陷晶片至关重要。基于氟聚合物的流体处理系统可确保高纯度、精确测量和耐化学腐蚀性,使其在日益小型化的半导体技术和高性能晶片製造中发挥关键作用。

预计2026年至2035年,北美半导体製造用含氟聚合物市场将以7.8%的复合年增长率成长。这项市场扩张主要得益于新一代生产工具的普及应用,这些工具依赖先进的含氟聚合物材料来实现热保护、污染控制和製程效率的提升。半导体製造工厂正面临晶片设计小型化的挑战,这要求材料即使在严苛的条件下也能保持优异的化学和热性能。最终,这将提高产量比率和装置的整体可靠性。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 积极扩张生产能力

- EUV和高数值孔径微影技术实施现状

- 先进包装技术的普及

- 产业潜在风险与挑战

- PFAS监管限制和合规成本

- 材料认证週期延长

- 市场机会

- 扩大中国基础设施节点的容量

- 先进包装材料的创新

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 不同类型的氟树脂

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 考虑碳足迹

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依氟聚合物类型划分,2022-2035年

- PTFE

- PFA

- FEP

- PVDF

- ETFE

- PCTFE

- 其他的

第六章 市场估计与预测:依应用领域划分,2022-2035年

- HTML纯度流体处理系统

- 大宗化学品经销

- 化学品储存和运输

- 过滤系统

- 其他的

- 化学品供应系统

- 自动分配系统

- 混合搅拌系统

- 其他的

- 晶圆处理和运输

- 晶圆载体盒

- 直接晶圆接触组件

- 机器人搬运夹具

- 其他的

- 湿式製程设备

- 电浆处理组件

- 其他的

第七章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第八章:公司简介

- The Chemours Company

- Daikin Industries, Ltd

- Solvay SA

- Arkema SA

- 3M Company

- Saint-Gobain

- Parker Hannifin Corporation

- Pexco LLC

- Holscot Advanced Polymers Ltd

The Global Fluoropolymers in Semiconductor Manufacturing Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 3.1 billion by 2035.

The semiconductor industry relies heavily on fluoropolymers due to their exceptional chemical resistance, thermal stability, and electrical insulation properties, which are critical for advanced device fabrication. Increasing demand for smaller, faster, and more efficient semiconductors has intensified the need for materials that can endure extreme processing environments. Asia-Pacific currently dominates the market, driven by the extensive semiconductor manufacturing capacities of China, South Korea, and Taiwan, supported by ongoing investments in fabrication infrastructure. The growing adoption of technologies such as 5G, artificial intelligence, and the Internet of Things is further increasing the requirement for advanced semiconductor components. North America is also witnessing rapid growth as manufacturers implement EUV and high-NA lithography technologies, which demand high-performance fluoropolymer materials capable of providing chemical protection and reliable performance at nanometer scales, ensuring enhanced yield and device efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $3.1 Billion |

| CAGR | 6.9% |

The PTFE (Polytetrafluoroethylene) segment held 33% share in 2025 and is expected to grow at a CAGR of 7.6% through 2035. Semiconductor manufacturers prefer PTFE because of its unmatched chemical resistance, high-temperature tolerance, and excellent dielectric properties. PTFE plays a crucial role in insulating layers, gaskets, and sealing applications, protecting semiconductor devices from harsh processing conditions while maintaining consistent performance across critical applications.

The high-purity fluid handling systems segment accounted for 30.1% share in 2025. These systems are essential in semiconductor production, where ultra-clean and precise environments are necessary to fabricate defect-free chips. Fluoropolymer-based fluid handling systems ensure high purity, precise measurement, and chemical resistance, which are critical for smaller node semiconductor technology and high-performance chip manufacturing.

North America Fluoropolymers in Semiconductor Manufacturing Market is expected to grow at a CAGR of 7.8% between 2026 and 2035. Market expansion is driven by the adoption of next-generation production tools that rely on advanced fluoropolymer materials to enhance thermal protection, contamination control, and process efficiency. Semiconductor fabrication facilities are increasingly miniaturizing chip designs, requiring materials that maintain chemical and thermal performance under extreme conditions, ultimately improving yield and overall device reliability.

Key players operating in the Global Fluoropolymers in Semiconductor Manufacturing Market include 3M Company, Arkema S.A., Daikin Industries, Ltd, Holscot Advanced Polymers Ltd, Pexco LLC, Parker Hannifin Corporation, Saint-Gobain, Solvay S.A., and The Chemours Company. Companies in the fluoropolymers in semiconductor manufacturing market are strengthening their position through innovation and strategic collaborations. Many are investing in research and development to create next-generation fluoropolymer materials with enhanced chemical, thermal, and electrical properties to meet the demands of advanced semiconductor nodes. Firms are expanding production capacities to support growing global semiconductor fabrication, particularly in high-demand regions such as Asia-Pacific and North America. Partnerships with semiconductor equipment manufacturers and strategic alliances with chip makers help integrate fluoropolymer solutions into critical fabrication processes.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fluoropolymer type

- 2.2.3 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Aggressive fab capacity expansion

- 3.2.1.2 EUV & high-NA lithography adoption

- 3.2.1.3 Advanced packaging proliferation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 PFAS regulatory restrictions & compliance costs

- 3.2.2.2 Long material qualification cycles

- 3.2.3 Market opportunities

- 3.2.3.1 China foundational node capacity expansion

- 3.2.3.2 Advanced packaging material innovation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Fluoropolymer type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Fluoropolymer Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 PTFE

- 5.3 PFA

- 5.4 FEP

- 5.5 PVDF

- 5.6 ETFE

- 5.7 PCTFE

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 High-purity fluid handling systems

- 6.2.1 Bulk chemical distribution

- 6.2.2 Chemical storage & transport

- 6.2.3 Filtration systems

- 6.2.4 Others

- 6.3 Chemical delivery systems

- 6.3.1 Automated dispensing systems

- 6.3.2 Mix & blend systems

- 6.3.3 Others

- 6.4 Wafer handling & transport

- 6.4.1 Wafer carriers & cassettes

- 6.4.2 Direct wafer contact components

- 6.4.3 Robotic handling fixtures

- 6.4.4 Others

- 6.5 Wet processing equipment

- 6.6 Plasma processing components

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 The Chemours Company

- 8.2 Daikin Industries, Ltd

- 8.3 Solvay S.A.

- 8.4 Arkema S.A.

- 8.5 3M Company

- 8.6 Saint-Gobain

- 8.7 Parker Hannifin Corporation

- 8.8 Pexco LLC

- 8.9 Holscot Advanced Polymers Ltd

半导体製造设备市场分析及预测(至2035年):依类型、产品、技术、组件、应用、材料类型、装置、製程、最终用户及製造阶段划分

半导体製造设备市场分析及预测(至2035年):依类型、产品、技术、组件、应用、材料类型、装置、製程、最终用户及製造阶段划分 扫描电子显微镜维修服务市场:按服务类型、应用和最终用户划分,全球预测(2026-2032年)显微镜目镜筒市场:按类型、材料、分销管道、应用和最终用户划分,全球预测,2026-2032年等离子切割系统市场:按设备类型、晶圆尺寸、晶圆厚度、最终用户和应用划分,全球预测,2026-2032年生物洁净作业台市场按产品类型、应用和最终用户划分,全球预测(2026-2032年)冷冻肉切丁机市场按机器类型、自动化程度、产能、终端用户产业、应用和销售管道划分,全球预测(2026-2032年)人工智慧市场分析及产量比率(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和设备划分以半导体产量比率预测为导向的人工智慧市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、製程、部署、最终用户和解决方案划分半导体产业的AI节水市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、製程、最终用户及解决方案划分半导体供应预测及2035年展望的AI市场分析:依类型、产品类型、服务、技术、组件、应用、最终用户、部署类型、功能及解决方案划分

扫描电子显微镜维修服务市场:按服务类型、应用和最终用户划分,全球预测(2026-2032年)显微镜目镜筒市场:按类型、材料、分销管道、应用和最终用户划分,全球预测,2026-2032年等离子切割系统市场:按设备类型、晶圆尺寸、晶圆厚度、最终用户和应用划分,全球预测,2026-2032年生物洁净作业台市场按产品类型、应用和最终用户划分,全球预测(2026-2032年)冷冻肉切丁机市场按机器类型、自动化程度、产能、终端用户产业、应用和销售管道划分,全球预测(2026-2032年)人工智慧市场分析及产量比率(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和设备划分以半导体产量比率预测为导向的人工智慧市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、製程、部署、最终用户和解决方案划分半导体产业的AI节水市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、製程、最终用户及解决方案划分半导体供应预测及2035年展望的AI市场分析:依类型、产品类型、服务、技术、组件、应用、最终用户、部署类型、功能及解决方案划分