|

市场调查报告书

商品编码

1959302

生物基聚酰胺市场机会、成长要素、产业趋势分析及2026年至2035年预测。Bio-Based Polyamide Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

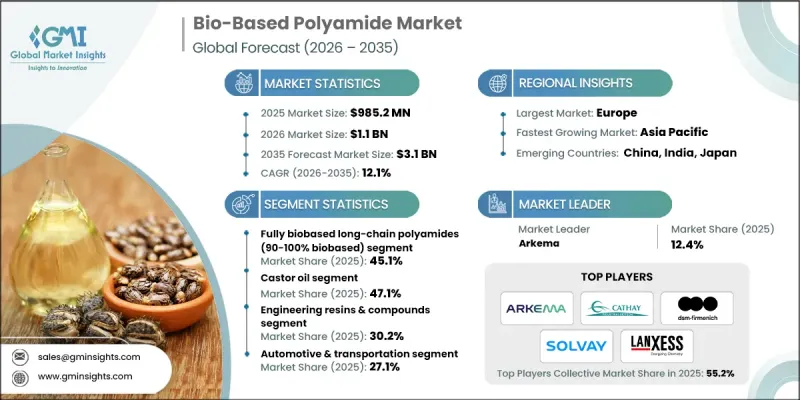

2025 年全球生物基聚酰胺市场价值为 9.852 亿美元,预计到 2035 年将达到 31 亿美元,年复合成长率为 12.1%。

市场成长的驱动力在于整个工业价值链对永续和环保材料日益增长的需求。生物基聚酰胺正日益被用作石油基聚合物的替代品,从而助力减少对石化燃料的依赖和整体碳排放。这些材料旨在提供与传统聚酰胺相当或更优的性能,例如高机械性能、耐化学性和热稳定性,以适应严苛的运作条件。透过减少温室气体排放和符合严格的法规结构,其更佳的环境效益使其成为製造商和环保意识的买家的理想选择。企业永续性目标、碳减排倡议以及对生态标籤和环境认证要求的遵守也推动了生物基聚酰胺的普及。因此,生物基聚酰胺在广泛的工业应用领域中日益受到青睐,从而巩固了其长期市场扩张的势头。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 9.852亿美元 |

| 预测金额 | 31亿美元 |

| 复合年增长率 | 12.1% |

预计到2025年,生物基含量为90%至100%的全生物基长链聚酰胺将占据45.1%的市场份额,并在2035年之前以12.2%的复合年增长率增长。这个细分市场受益于可再生原料采购和聚合物加工技术的进步,以及对兼具卓越环保性能和可靠功能性的材料日益增长的需求。这些聚酰胺在既需要永续性又需要耐久性的应用中越来越受欢迎。

预计到2025年,蓖麻油衍生聚酰胺的市占率将达到47.1%,并在2026年至2035年间以12.2%的复合年增长率成长。蓖麻油衍生聚酰胺因其原料的可再生性、稳定的供应以及优异的性能而广受认可。加工效率和聚合物设计的不断改进,正在提升其成本竞争力,并推动其在多个终端应用领域的应用。

预计到2025年,北美生物基聚酰胺市场占有率将达到21.1%,并持续维持加速成长。该地区受益于有利的环境政策、人们对永续材料日益增长的认识以及製造业的广泛应用。持续的研发投入以及创新主导的产品开发,进一步提升了区域市场的表现。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 考虑碳足迹

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依聚酰胺类型划分,2022-2035年

- 完全生物基长链聚酰胺(生物基含量90-100%)

- 高生物碱含量长链聚酰胺(生物碱含量60-89%)

- 具有中等生物基含量(生物基含量25-59%)的特殊聚酰胺

第六章 市场估计与预测:依原料来源划分,2022-2035年

- 蓖麻油衍生的生物基聚酰胺

- 玉米衍生生物基聚酰胺

- 由甘蔗和非食用生物质衍生的生物基聚酰胺。

- 其他的

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 工程树脂和化合物

- 纤维和丝状物

- 薄膜和软包装

- 挤出型材和管材

- 用于增材製造的粉末和丝材

- 其他的

第八章 市场估算与预测:依最终用途划分,2022-2035年

- 汽车/运输设备

- 纺织服装

- 电子电器设备

- 包装/消费品

- 建材

- 工业机械和水资源管理

- 医疗和药品

- 其他的

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十章:公司简介

- AKRO-PLASTIC GmbH

- Arkema

- Avient Corporation

- Cathay Biotech

- Domo Chemicals

- DSM-Firmenich

- Evonik Industries

- LANXESS

- NUREL

- Solvay

- Tekmar Group(TEKMA)

The Global Bio-Based Polyamide Market was valued at USD 985.2 million in 2025 and is estimated to grow at a CAGR of 12.1% to reach USD 3.1 billion by 2035.

Market growth is influenced by rising demand for sustainable, low-impact materials across industrial value chains. Bio-based polyamides are increasingly being adopted as alternatives to petroleum-derived polymers, supporting efforts to reduce fossil fuel dependence and lower overall carbon emissions. These materials are designed to deliver high-performance characteristics that meet or exceed those of conventional polyamides, including strong mechanical properties, chemical resistance, and thermal stability suitable for demanding operating conditions. Their reduced greenhouse gas emissions improved environmental profile, and alignment with strict regulatory frameworks makes them attractive to manufacturers and environmentally conscious buyers alike. Adoption is also being supported by corporate sustainability targets, carbon reduction initiatives, and compliance with eco-labeling and environmental certification requirements. As a result, bio-based polyamides are gaining traction across a wide range of industrial applications, reinforcing long-term market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $985.2 Million |

| Forecast Value | $3.1 Billion |

| CAGR | 12.1% |

The fully bio-based long-chain polyamides with a bio-based content of 90% to 100% accounted for 45.1% share in 2025 and are expected to grow at a CAGR of 12.2% through 2035. This segment is benefiting from advances in renewable feedstock sourcing and polymer processing technologies, combined with increasing preference for materials that offer both strong environmental credentials and reliable functional performance. These polyamides are increasingly favored in applications requiring durability alongside sustainability.

The castor oil segment held a 47.1% share in 2025 and is projected to grow at a CAGR of 12.2% from 2026 to 2035. Castor oil-based polyamides are gaining widespread acceptance due to the renewable nature of the feedstock, consistent supply availability, and favorable performance characteristics. Continuous improvements in processing efficiency and polymer design are enhancing cost competitiveness and expanding adoption across multiple end-use sectors.

North America Bio-Based Polyamide Market accounted for a 21.1% share in 2025 and continues to demonstrate accelerated growth. The region benefits from supportive environmental policies, rising awareness around sustainable materials, and strong adoption across manufacturing industries. Ongoing research activity and innovation-driven product development are further strengthening regional market performance.

Key companies operating in the Global Bio-Based Polyamide Market include Arkema, DSM, Firmenich, Evonik Industries, LANXESS, Solvay, Avient Corporation, Domo Chemicals, Cathay Biotech, AKRO PLASTIC GmbH, NUREL, and Tekmar Group (TEKMA). Companies in the bio-based polyamide market are reinforcing their market position through strategic investments in research and development to enhance material performance and expand application scope. Many players are prioritizing partnerships with downstream manufacturers to accelerate commercialization and adoption. Capacity expansions, supply chain optimization, and improved access to renewable feedstocks are helping firms meet rising demand. Sustainability certifications and compliance with environmental regulations are being leveraged to strengthen brand credibility. Geographic expansion into high-growth regions and diversification of product portfolios are also key strategies supporting long-term competitiveness and market foothold.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Polyamide type

- 2.2.3 Feedstock sources

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Polyamide Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Fully biobased long-chain polyamides (90-100% biobased)

- 5.3 High biobased content long-chain polyamides (60-89% biobased)

- 5.4 Moderate biobased content specialty polyamides (25-59% biobased)

Chapter 6 Market Estimates and Forecast, By Feedstock Source, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Castor oil-derived bio-based polyamides

- 6.3 Corn-derived bio-based polyamides

- 6.4 Sugarcane & inedible biomass-derived bio-based polyamides

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Engineering resins & compounds

- 7.3 Textile fibers & filaments

- 7.4 Films & flexible packaging

- 7.5 Extruded profiles & tubes

- 7.6 Additive manufacturing powders & filaments

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Automotive & transportation

- 8.3 Textiles & apparel

- 8.4 Electronics & electrical

- 8.5 Packaging & consumer goods

- 8.6 Construction & building materials

- 8.7 Industrial machinery & water management

- 8.8 Medical & pharmaceutical

- 8.9 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 AKRO-PLASTIC GmbH

- 10.2 Arkema

- 10.3 Avient Corporation

- 10.4 Cathay Biotech

- 10.5 Domo Chemicals

- 10.6 DSM-Firmenich

- 10.7 Evonik Industries

- 10.8 LANXESS

- 10.9 NUREL

- 10.10 Solvay

- 10.11 Tekmar Group (TEKMA)