|

市场调查报告书

商品编码

1959304

醋基保鲜系统市场机会、成长要素、产业趋势分析及预测(2026-2035年)Vinegar-based Preservation Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

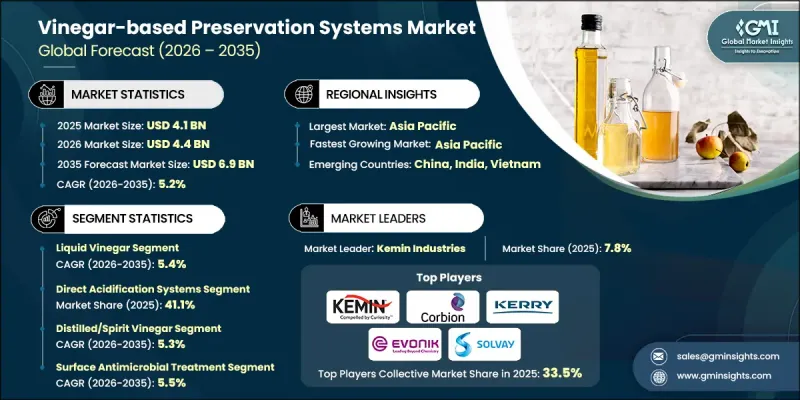

2025 年全球醋基保鲜系统市场价值为 41 亿美元,预计到 2035 年将达到 69 亿美元,年复合成长率为 5.2%。

该市场涵盖多种解决方案,例如液态醋、粉状醋和干醋、浓缩型醋、缓衝醋混合物以及有机醋技术。这些系统采用先进的製造流程开发,包括复合保藏系统、氯化钙和醋酸组合系统、过氧乙酸 (PAA) 基溶液、缓衝系统和直接酸化技术。应用范围涵盖蒸馏食品、饮料、调味酱料、肉类和家禽产品以及烘焙产品。市场成长的驱动力在于消费者对天然和洁净标示保藏方法的需求不断增长,以及食品安全和永续加工方法监管支援的加强。世界各国政府正透过资助和支持政策,促进采用环境友善且对消费者友善的保藏技术,用于天然抗菌解决方案的研究。目前,亚太地区在醋基保藏系统市场中处于领先地位,这主要得益于中国、印度和日本等国家对生产能力和基础设施的大力投资。同时,北美市场正迅速崛起,这得益于技术创新、洁净标示成分支出的增加以及消费者对加工最少和天然保藏食品日益增长的偏好。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 41亿美元 |

| 预测金额 | 69亿美元 |

| 复合年增长率 | 5.2% |

预计到2025年,液态醋的市占率将达到53.4%,并在2035年之前以5.4%的复合年增长率成长。液态醋在众多食品类别中的广泛应用,反映了其强大的抗菌性能和对不同配方的适应性。液态醋符合洁净标示的趋势,满足了消费者对透明成分标籤的需求。由于液态醋的高效性、可靠性以及无需依赖合成添加剂即可延长保质期的特性,食品生产商正将其应用于各种保鲜製程。

预计到2025年,直接酸化系统市占率将达到41.1%,到2035年将以5.2%的复合年增长率成长。这些系统因其能够快速且有效率地控制微生物,并能无缝整合到大规模食品生产环境中而备受认可。食品安全标准的提高和产品品质的维持能力正在推动商业加工设施对该系统的应用。对低加工食品需求的成长以及对食品安全合规性的日益关注,持续加速醋基保鲜系统市场对直接酸化技术的应用。

预计2026年至2035年,北美醋基防腐剂市场将以5.2%的复合年增长率成长。市场扩张的驱动力主要来自永续加工技术的创新以及缓衝醋配方作为洁净标示防腐剂的日益普及。该地区的企业正致力于开发符合食品安全法规和循环经济倡议的天然解决方案。消费者对人工防腐剂潜在健康风险的日益关注,促使製造商转向使用GRAS认证的醋基防腐剂,从而推动市场持续成长。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 考虑碳足迹

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 液体醋

- 浓缩醋

- 醋粉

- 缓衝醋 - 液体

- 缓衝醋 - 干粉状

- 有机醋

- 其他的

第六章 市场估计与预测:依技术类型划分,2022-2035年

- 直接酸化系统

- 缓衝醋系统

- 钠基

- 钾基

- 钙基

- 氯化钙+醋酸体系

- 复合储能係统

- 基于过氧乙酸(PAA)的体系

- 其他的

第七章 市场估价与预测:依原料分類的醋市场,2022-2035年

- 蒸馏醋/烈酒醋

- 苹果醋

- 葡萄酒醋

- 红酒醋

- 白葡萄酒醋

- 香醋

- 米醋

- 其他的

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 腌菜和咸味食品

- 表面抗菌处理

- 腌製和浸泡系统

- 调味料和调味料的混合

- 散装/工业储存系统

- 发酵助剂和保肝剂

- 其他的

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十章:公司简介

- Kemin Industries

- Corbion NV

- Kerry Group

- Evonik Industries

- Solvay SA

- IFF

- Novonesis

- Galactic SA

- Henan Weichuang

- YOTA BIO

- Hydrite Chemical

- BioSafe Systems

- Sunson Biotech

- Handary SA

- AmTech Ingredients

The Global Vinegar-based Preservation Systems Market was valued at USD 4.1 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 6.9 billion by 2035.

The market includes a wide range of solutions such as liquid vinegar, powdered and dry vinegar formats, concentrated variants, buffered vinegar blends, and organic vinegar technologies. These systems are developed using advanced production approaches, including combination preservation systems, calcium chloride with acetic acid systems, peroxyacetic acid (PAA)-based solutions, buffered systems, and direct acidification technologies. Applications span ready-to-eat meals, beverages, sauces and dressings, meat and poultry, and bakery products. Growth is being fueled by rising demand for natural and clean-label preservation methods, along with increasing regulatory support for food safety and sustainable processing practices. Governments worldwide are encouraging the adoption of environmentally responsible and consumer-friendly preservation technologies by funding research into natural antimicrobial solutions and implementing supportive policies. Asia Pacific currently leads the vinegar-based preservation systems market, driven by strong investments in production capacity and infrastructure across countries such as China, India, and Japan. Meanwhile, North America is emerging rapidly due to technological innovation, higher spending on clean-label ingredients, and a growing consumer preference for minimally processed and naturally preserved food products.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.1 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 5.2% |

The liquid vinegar segment accounted for 53.4% share in 2025 and is anticipated to grow at a CAGR of 5.4% through 2035. Its widespread adoption across multiple food categories reflects its strong antimicrobial performance and compatibility with diverse formulations. Liquid vinegar aligns with clean label trends and meets consumer demand for transparent ingredient declarations. Food manufacturers are incorporating liquid vinegar into various preservation processes due to its effectiveness, reliability, and ability to support extended shelf life without relying on synthetic additives.

The direct acidification systems segment held 41.1% share in 2025 and is forecast to grow at a CAGR of 5.2% by 2035. These systems are recognized for delivering fast and efficient microbial control while integrating seamlessly into large-scale food production environments. Their ability to enhance food safety standards and maintain product integrity has strengthened their adoption across commercial processing facilities. Rising demand for minimally processed food options and heightened attention to food safety compliance continue to accelerate the deployment of direct acidification technologies within the vinegar-based preservation systems market.

North America Vinegar-based Preservation Systems Market is expected to grow at a CAGR of 5.2% between 2026 and 2035. Market expansion is being supported by innovation in sustainable processing techniques and increasing use of buffered vinegar formulations as clean-label preservation ingredients. Companies across the region are focusing on developing natural solutions that align with food safety regulations and circular economy initiatives. Growing consumer awareness regarding the potential health concerns associated with artificial preservatives has encouraged manufacturers to shift toward GRAS-designated, vinegar-based preservation ingredients, thereby driving sustained market growth.

Key companies operating in the Global Vinegar-based Preservation Systems Market include Kerry Group, Kemin Industries, Corbion N.V., Solvay S.A., IFF, Evonik Industries, Galactic S.A., Novonesis, Hydrite Chemical, Henan Weichuang, BioSafe Systems, YOTA BIO, Handary S.A., Sunson Biotech, and AmTech Ingredients. Companies in the Global Vinegar-based Preservation Systems Market are strengthening their competitive position through strategic product innovation, expansion of clean label portfolios, and investment in sustainable production technologies. Many players are enhancing research and development capabilities to create advanced antimicrobial blends that meet evolving regulatory and consumer standards. Strategic partnerships, capacity expansions, and regional manufacturing investments are also being used to improve supply chain resilience and global reach. Firms are focusing on certifications, GRAS compliance, and transparent sourcing practices to build brand credibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Technology type

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Liquid vinegar

- 5.3 Concentrated vinegar

- 5.4 Dry / powder vinegar

- 5.5 Buffered vinegar - liquid

- 5.6 Buffered vinegar - dry / powder

- 5.7 Organic vinegar

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Technology Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Direct acidification systems

- 6.3 Buffered vinegar systems

- 6.3.1 Sodium-based

- 6.3.2 Potassium-based

- 6.3.3 Calcium-based

- 6.4 Calcium chloride + acetic acid systems

- 6.5 Combination preservation systems

- 6.6 Peroxyacetic acid (PAA)-based systems

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Vinegar Source, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Distilled / spirit vinegar

- 7.3 Apple cider vinegar

- 7.3.1 Wine vinegar

- 7.3.2 Red wine vinegar

- 7.4 White wine vinegar

- 7.5 Balsamic vinegar

- 7.6 Rice vinegar

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Pickling & brining

- 8.3 Surface antimicrobial treatment

- 8.4 Marinade & injection systems

- 8.5 Dressing & condiment formulation

- 8.6 Bulk / industrial preservation systems

- 8.7 Fermentation aid & pH control

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Kemin Industries

- 10.2 Corbion N.V.

- 10.3 Kerry Group

- 10.4 Evonik Industries

- 10.5 Solvay S.A.

- 10.6 IFF

- 10.7 Novonesis

- 10.8 Galactic S.A.

- 10.9 Henan Weichuang

- 10.10 YOTA BIO

- 10.11 Hydrite Chemical

- 10.12 BioSafe Systems

- 10.13 Sunson Biotech

- 10.14 Handary S.A.

- 10.15 AmTech Ingredients

冷冻保存设备市场:按设备类型、储存方法、容量、应用和最终用户划分,全球预测,2026-2032年

冷冻保存设备市场:按设备类型、储存方法、容量、应用和最终用户划分,全球预测,2026-2032年 2026年全球冷冻保存设备市场报告

2026年全球冷冻保存设备市场报告 细胞冷冻保存市场-全球产业规模、份额、趋势、机会、预测:按产品、应用、地区和竞争对手划分,2021-2031年HPV子宫颈细胞保存液市场:按保存技术、应用和分销管道分類的全球预测(2026-2032年)液态氮冷冻治疗舱市场(按舱体类型、应用、最终用户和分销管道划分)—2026-2032年全球预测2025年全球干细胞冷冻保存市场报告

细胞冷冻保存市场-全球产业规模、份额、趋势、机会、预测:按产品、应用、地区和竞争对手划分,2021-2031年HPV子宫颈细胞保存液市场:按保存技术、应用和分销管道分類的全球预测(2026-2032年)液态氮冷冻治疗舱市场(按舱体类型、应用、最终用户和分销管道划分)—2026-2032年全球预测2025年全球干细胞冷冻保存市场报告 细胞冷冻保存市场规模、份额及成长分析(按产品、应用、最终用途及地区划分)-2026-2033年产业预测

细胞冷冻保存市场规模、份额及成长分析(按产品、应用、最终用途及地区划分)-2026-2033年产业预测 细胞冷冻保存设备市场规模、份额和趋势分析报告:按产品、应用、最终用途、地区和细分市场预测(2025-2033 年)生物保存市场-全球产业规模、份额、趋势、机会和预测,依产品、应用、地区和竞争格局划分,2020-2030年预测全球细胞冷冻保存市场:市场规模、份额、趋势分析(按产品、应用、最终用途和地区)、细分市场预测(2025-2033)

细胞冷冻保存设备市场规模、份额和趋势分析报告:按产品、应用、最终用途、地区和细分市场预测(2025-2033 年)生物保存市场-全球产业规模、份额、趋势、机会和预测,依产品、应用、地区和竞争格局划分,2020-2030年预测全球细胞冷冻保存市场:市场规模、份额、趋势分析(按产品、应用、最终用途和地区)、细分市场预测(2025-2033)