|

市场调查报告书

商品编码

1959305

生物基溶剂市场(油漆和清洁):机会、成长要素、产业趋势分析与预测(2026-2035年)Bio-Based Solvents for Coatings and Cleaning Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

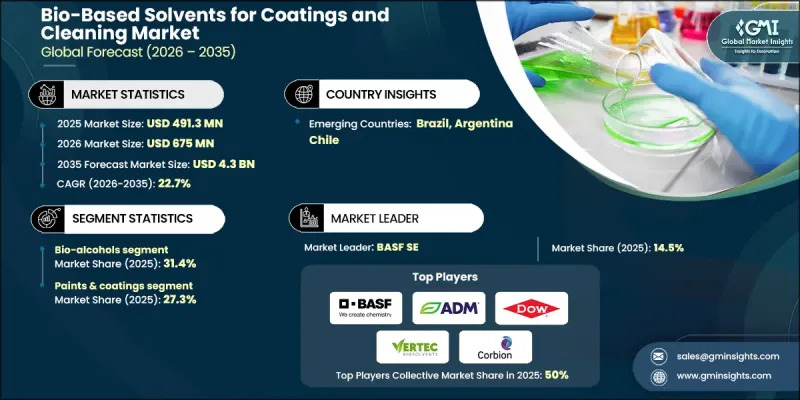

2025 年全球用于油漆和清洁的生物基溶剂市场价值为 4.913 亿美元,预计到 2035 年将达到 43 亿美元,年复合成长率为 22.7%。

随着各行业向永续、低毒性、低VOC的化学替代品转型,市场正经历快速变化。消费者对环境影响和职场安全的日益关注,加速了从传统石油化学溶剂转向可再生替代品的过渡。主要经济体的监管机构正在加强化学品安全框架,并限制在生产和维护作业中使用高VOC物质。基于既定环境和化学品管理政策的合规要求,迫使製造商采用更安全的配方。因此,对生物基溶剂(例如乳酸酯、可再生醇、萜烯溶剂和甘油衍生物)的需求显着增长。这些替代品具有溶解性能强、挥发性可控、与多种基材相容性好等优点,同时也能降低对环境的影响。工业涂料、表面处理、汽车喷漆、航太维护和高性能建筑应用等领域对高效、高纯度溶剂系统的需求不断增长,进一步推动了市场成长,因为这些领域需要符合严格技术标准的溶剂系统。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 4.913亿美元 |

| 预测金额 | 43亿美元 |

| 复合年增长率 | 22.7% |

预计到2025年,生物醇类溶剂的市占率将达到31.4%,并在2035年之前以21.3%的复合年增长率成长。其强大的市场地位得益于其多功能性、广泛的工业应用以及与传统石油基溶剂相比的成本竞争力。可再生醇类溶剂具有良好的溶解性和均衡的蒸发速率,因此适用于涂料、表面处理剂和工业清洁剂的配方。凭藉其完善的大规模生产基础设施和可靠的可再生原材料供应,该领域在全球市场确保了供应的稳定性和商业性扩充性。

预计到2025年,涂料製造业将占据27.3%的市场份额,并在2026年至2035年间以21.7%的复合年增长率成长。该行业高度依赖溶剂来实现配方均匀性、分散效率、黏度控制和固化性能,因此也是生物基替代品的主要消费群体。製造商正在加速将可再生溶剂整合到其产品线中,以满足严格的环境法规并减少挥发性排放。环保涂料技术的转变正在推动以植物来源醇、酯类溶液和甘油基化学品取代传统溶剂,从而加强整个价值链的永续性发展。

预计到2025年,北美生物基溶剂在涂料和清洁应用领域的市占率将达到31.2%,反映出该地区强劲的发展动能。成熟的产业生态系统、积极的环境政策以及严格的空气品质标准是支撑这个市场的重要因素。限制在生产和维护活动中使用高挥发性有机化合物(VOC)溶剂的监管措施正在推动可再生替代品的采用。此外,成熟的生物炼製技术已为醇基和甘油基溶剂建立了本地化的供应链,进一步增强了市场实力。持续推进的洁净科技项目和绿色化学倡议正在进一步推动涂料、特种化学品和工业流程领域的市场渗透。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 考虑碳足迹

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依类型划分,2022-2035年

- 生物醇

- 乳酸酯

- 甘油衍生物

- D-柠檬烯

- 2-甲基四氢呋喃(2-MeTHF)

- 脂肪酸衍生物

- 其他的

第六章 市场估计与预测:依最终用途产业划分,2022-2035年

- 油漆和涂料製造

- 建筑涂料製造商

- 工业涂料製造商

- 特种和功能性涂层製造商

- 汽车和运输设备

- OEM

- 一级和二级供应商

- 售后及翻新服务

- 工业製造

- 金属加工/金属製品製造

- 机械设备製造

- 一般製造和组装工作

- 建筑/施工

- 住宅

- 商业和公共设施的建设

- 基础设施和土木工程

- 航太/国防

- 民航机製造

- 军事和国防系统

- 维护、修理和大修 (MRO)

- 电子设备和电气装置

- 消费性电子产品製造

- 工业电子设备及控制装置

- 半导体和印刷基板製造

- 製药

- 药品原料药(API)生产

- 医疗设备及诊断设备

- 契约製造组织(CMO)

- 印刷/包装

- 商业印刷

- 软包装

- 硬质包装和标籤

- 化妆品和个人护理

- 护肤和护髮产品

- 彩妆品和香水

- 天然有机美容产品

- 其他的

第七章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第八章:公司简介

- BASF SE

- Archer Daniels Midland Company(ADM)

- Ashland Global Holdings Inc.

- Bio Brands LLC

- Circa Group

- Clariant AG

- Corbion NV

- Dow Inc.

- DuPont de Nemours, Inc.

- Eastman Chemical Company

- Evonik Industries AG

- Florachem Corporation

- LyondellBasell Industries NV

- Solvay SA

- Vertec BioSolvents, Inc.

- Others

The Global Bio-Based Solvents for Coatings and Cleaning Market was valued at USD 491.3 million in 2025 and is estimated to grow at a CAGR of 22.7% to reach USD 4.3 billion by 2035.

The market is undergoing rapid transformation as industries shift toward sustainable, low-toxicity, and low-VOC chemical alternatives. Growing consumer awareness regarding environmental impact and workplace safety is accelerating the replacement of conventional petrochemical solvents with renewable substitutes. Regulatory authorities across major economies are tightening chemical safety frameworks and limiting the use of high-VOC substances in manufacturing and maintenance operations. Compliance requirements under established environmental and chemical control policies are pushing manufacturers to adopt safer formulations. As a result, demand for bio-based solvents, including lactate esters, renewable alcohols, terpene-based solvents, and glycerol-derived compounds, is rising significantly. These alternatives deliver strong solvency performance, controlled evaporation profiles, and compatibility with diverse substrates while reducing environmental footprint. Expanding use in industrial coatings, surface treatment, automotive refinishing, aerospace maintenance, and high-performance architectural applications is further strengthening market growth, as these sectors require efficient, high-purity solvent systems capable of meeting strict technical standards.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $491.3 Million |

| Forecast Value | $4.3 Billion |

| CAGR | 22.7% |

The bio-alcohols segment accounted for 31.4% share in 2025 and is expected to grow at a CAGR of 21.3% through 2035. Their strong market position is supported by versatility, wide industrial applicability, and cost competitiveness compared to traditional petroleum-based solvents. Renewable alcohol-based solvents provide effective dissolution properties and balanced evaporation rates, making them suitable for coatings, surface preparation, and industrial cleaning formulations. The segment benefits from established large-scale production infrastructure and reliable renewable feedstock availability, ensuring supply stability and commercial scalability across global markets.

The paints and coatings manufacturing segment held 27.3% share in 2025 and is projected to grow at a CAGR of 21.7% between 2026 and 2035. The industry's heavy reliance on solvents for formulation consistency, dispersion efficiency, viscosity adjustment, and curing performance positions it as a key consumer of bio-based alternatives. Manufacturers are increasingly integrating renewable solvents into product lines to meet stringent environmental regulations and reduce total VOC emissions. The transition toward eco-conscious coating technologies has accelerated the substitution of conventional solvents with plant-derived alcohols, ester-based solutions, and glycerol-based chemistries, strengthening sustainability initiatives across the value chain.

North America Bio-Based Solvents for Coatings and Cleaning Market held a 31.2% share in 2025, reflecting strong regional momentum. The market is supported by a mature industrial ecosystem, proactive environmental policies, and rigorous enforcement of air quality standards. Regulatory measures restricting high-VOC solvent usage in production and maintenance activities are encouraging the adoption of renewable alternatives. The region also benefits from established bio-refining capabilities, supporting localized supply chains for alcohol-based and glycerol-derived solvents. Ongoing clean technology programs and green chemistry initiatives are further driving market penetration across coatings, specialty chemicals, and industrial processing sectors.

Key companies operating in the Global Bio-Based Solvents for Coatings and Cleaning Market include BASF SE, Dow Inc., Archer Daniels Midland Company (ADM), Eastman Chemical Company, DuPont de Nemours, Inc., Evonik Industries AG, Clariant AG, Solvay S.A., LyondellBasell Industries N.V., Corbion N.V., Ashland Global Holdings Inc., Vertec BioSolvents, Inc., Circa Group, Florachem Corporation, and Bio Brands LLC. These industry leaders are actively competing through product innovation, sustainable sourcing strategies, and global expansion initiatives. Companies in the Bio-Based Solvents for Coatings and Cleaning Market are strengthening their competitive position by investing heavily in research and development to enhance solvent performance, purity levels, and application versatility. Strategic collaborations with coatings manufacturers and industrial formulators enable tailored product development and long-term supply agreements. Many firms are expanding bio-refining capacity to secure renewable feedstock supply and improve cost efficiency. Portfolio diversification into specialty and high-performance solvent grades supports differentiation in a competitive environment.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 End use industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Bio-Alcohols

- 5.3 Lactate Esters

- 5.4 Glycerol Derivatives

- 5.5 D-Limonene

- 5.6 2-Methyltetrahydrofuran (2-MeTHF)

- 5.7 Fatty Acid Derivatives

- 5.8 Other Bio-Based Solvents

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Paints & Coatings Manufacturing

- 6.2.1 Architectural Coatings Manufacturers

- 6.2.2 Industrial Coatings Manufacturers

- 6.2.3 Specialty & Functional Coatings Manufacturers

- 6.3 Automotive & Transportation

- 6.3.1 Original Equipment Manufacturers (OEMs)

- 6.3.2 Tier-1 & Tier-2 Suppliers

- 6.3.3 Aftermarket & Refinishing Services

- 6.4 Industrial Manufacturing

- 6.4.1 Metal Fabrication & Metalworking

- 6.4.2 Machinery & Equipment Manufacturing

- 6.4.3 General Manufacturing & Assembly Operations

- 6.5 Building & Construction

- 6.5.1 Residential Construction

- 6.5.2 Commercial & Institutional Construction

- 6.5.3 Infrastructure & Civil Engineering

- 6.6 Aerospace & Defense

- 6.6.1 Commercial Aircraft Manufacturing

- 6.6.2 Military & Defense Systems

- 6.6.3 Maintenance, Repair & Overhaul (MRO)

- 6.7 Electronics & Electrical Equipment

- 6.7.1 Consumer Electronics Manufacturing

- 6.7.2 Industrial Electronics & Controls

- 6.7.3 Semiconductor & PCB Manufacturing

- 6.8 Pharmaceuticals

- 6.8.1 Active Pharmaceutical Ingredient (API) Manufacturing

- 6.8.2 Medical Devices & Diagnostics

- 6.8.3 Contract Manufacturing Organizations (CMOs)

- 6.9 Printing & Packaging

- 6.9.1 Commercial Printing

- 6.9.2 Flexible Packaging

- 6.9.3 Rigid Packaging & Labels

- 6.10 Cosmetics & Personal Care

- 6.10.1 Skincare & Haircare Products

- 6.10.2 Color Cosmetics & Fragrances

- 6.10.3 Natural & Organic Beauty Products

- 6.11 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 BASF SE

- 8.2 Archer Daniels Midland Company (ADM)

- 8.3 Ashland Global Holdings Inc.

- 8.4 Bio Brands LLC

- 8.5 Circa Group

- 8.6 Clariant AG

- 8.7 Corbion N.V.

- 8.8 Dow Inc.

- 8.9 DuPont de Nemours, Inc.

- 8.10 Eastman Chemical Company

- 8.11 Evonik Industries AG

- 8.12 Florachem Corporation

- 8.13 LyondellBasell Industries N.V.

- 8.14 Solvay S.A.

- 8.15 Vertec BioSolvents, Inc.

- 8.16 Others

排水管溶剂市场:依产品类型、最终用户、通路及应用划分-2026-2032年全球市场预测溶剂市场:按类型、极性、产品类型和应用划分-2026-2032年全球预测二氧化碳捕集溶剂市场:依溶剂类型、製程、技术及终端用户产业划分-2026-2032年全球预测

排水管溶剂市场:依产品类型、最终用户、通路及应用划分-2026-2032年全球市场预测溶剂市场:按类型、极性、产品类型和应用划分-2026-2032年全球预测二氧化碳捕集溶剂市场:依溶剂类型、製程、技术及终端用户产业划分-2026-2032年全球预测 残余溶剂市场分析及预测(至2035年):依类型、产品类型、服务、技术、应用、形态、最终用户、製程、设备划分

残余溶剂市场分析及预测(至2035年):依类型、产品类型、服务、技术、应用、形态、最终用户、製程、设备划分 半导体溶剂市场:依类型、溶剂类别、应用、国家及地区划分-全球产业分析、市场规模、市场占有率及2025年至2032年预测

半导体溶剂市场:依类型、溶剂类别、应用、国家及地区划分-全球产业分析、市场规模、市场占有率及2025年至2032年预测 日本溶剂市场规模、份额、趋势和预测:按产品、原材料、应用和地区划分,2026-2034年溶剂市场规模、份额、趋势及预测(依产品、原料、应用及地区划分),2026-2034年

日本溶剂市场规模、份额、趋势和预测:按产品、原材料、应用和地区划分,2026-2034年溶剂市场规模、份额、趋势及预测(依产品、原料、应用及地区划分),2026-2034年 2026年全球溶剂市场报告2026年全球生物基溶剂市场报告2026年超临界二氧化碳(CO2)干粉化学品全球市场报告

2026年全球溶剂市场报告2026年全球生物基溶剂市场报告2026年超临界二氧化碳(CO2)干粉化学品全球市场报告