|

市场调查报告书

商品编码

1959306

个人护理生物基界面活性剂市场机会、成长要素、产业趋势分析及预测(2026-2035年)Bio-based Surfactants for Personal Care Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

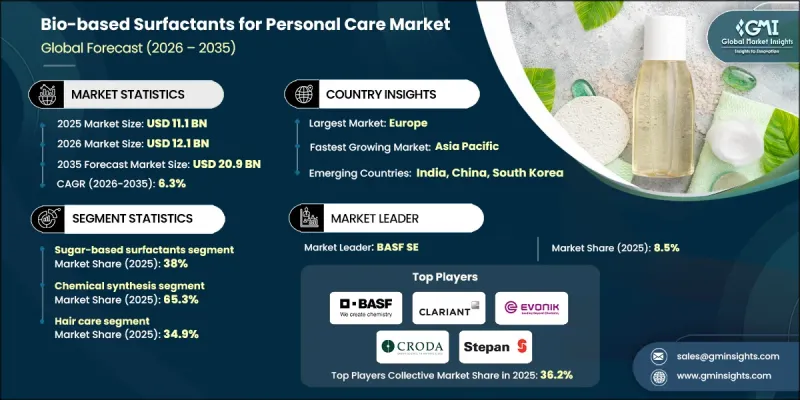

2025 年全球个人护理用生物基界面活性剂市场价值为 111 亿美元,预计到 2035 年将达到 209 亿美元,年复合成长率为 6.3%。

市场扩张反映了美容和个人护理行业加速向永续和可生物降解原材料转型。用于个人保健产品的生物基界面活性剂涵盖了广泛的可再生技术,包括微生物生物界面活性剂、氨基酸基界面活性剂、糖基表面活性剂、生物基乙氧基化物以及其他透过发酵、酵素处理和可再生原料合成等方法开发的植物来源替代品。这些原料在护髮、护肤、口腔护理、婴儿护理和特色美容产品中的可再生日益广泛。意识提升对环境永续性和原材料透明度的日益关注正在显着影响他们的购买决策。世界各国政府都在积极推广绿色化学框架,支持可再生配方创新,并实施鼓励环保个人照护生产体系转型的监管政策。目前,欧洲在世界范围内处于领先地位,这得益于其主要经济体强有力的监管支持和对生产基础设施的大量投资。同时,亚太地区正在崛起为一个高成长地区,这得益于快速的工业发展、人们对天然美容解决方案日益增长的兴趣,以及消费者对洁净标示和环保型个人保健产品的偏好不断增强。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 111亿美元 |

| 预测金额 | 209亿美元 |

| 复合年增长率 | 6.3% |

预计到2025年,糖基界面活性剂的市占率将达到38%,并在2035年之前以6.7%的复合年增长率成长。其市场份额的不断增长归功于其温和的性能、高生物降解性和对敏感肌肤配方的适用性。由于与天然和有机产品相容,这些表面活性剂被广泛应用于各种个人护理领域。製造商更倾向于使用糖基界面活性剂,因为它们既能提供有效的清洁力,又能满足清洁美容的标准。对温和的植物来源成分日益增长的需求,正在加速糖基界面活性剂在新一代化妆品配方中的应用。

预计到2025年,以可再生原料为基础的化学合成製程将占65.3%的市场份额,并在2035年以6.2%的复合年增长率成长。此生产製程在多种生物基界面活性剂的生产中发挥至关重要的作用,包括胺基酸衍生物、糖基界面活性剂和生物基乙氧基化物。该方法利用可再生原料,并透过成熟的化学技术进行加工,这些技术以其扩充性、营运效率和稳定的产品品质而闻名。与新兴的生物技术平台相比,该方法具有更高的商业性可行性和成本优势,使其在大规模生产中极具吸引力。对可再生原料供应链投资的不断增加以及对可靠的生物基界面活性剂生产日益增长的需求,进一步巩固了该技术平台的优势。

预计2026年至2035年,北美个人护理领域生物基界面活性剂市场将以6.7%的复合年增长率成长。这一区域成长主要得益于永续原料开发的创新以及符合绿色化学原则的发酵技术的日益普及。随着消费者对传统界面活性剂环境影响的日益关注,各大品牌正在重新设计产品,采用可生物降解的植物来源替代品。不断壮大的清洁美容运动,以及鼓励环保生产的法规,进一步刺激了护髮、护肤和专业个人护理领域的需求。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监理情势

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 考虑碳足迹

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 微生物生物生物界面活性剂

- 醣脂

- 槐醣脂

- 鼠李醣脂

- 赤藻糖醇醇脂质(MEL)

- 海藻醣脂质

- 脂肽

- 表面活性素

- 伊特林

- 理研新

- 醣脂

- 糖基界面活性剂

- 烷基聚葡萄糖苷(APGs)

- 葡糖酰胺

- 蔗糖酯

- 山梨糖醇酯

- 胺基酸衍生的表面活性剂

- 麸胺酸

- 甘胺酸

- 异硫氰酸酯

- 肌氨酸

- 牛

- 生物基乙氧基化物

- 生物基醇醚

- 生物基聚山梨醇酯

- 生物基PEG衍生物

- 生物基蓖麻油乙氧基化物

- 其他的

第六章 市场估计与预测:依技术类型划分,2022-2035年

- 微生物发酵技术

- 利用可再生原料进行化学合成

- 酵素合成

- 其他的

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 护髮

- 护肤

- 口腔护理

- 婴儿护理

- 专业个人护理

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- BASF SE

- Clariant AG

- Evonik Industries AG

- Croda International Plc

- Kao Corporation

- Stepan Company

- Sino Lion

- Galaxy Surfactants Ltd

- Ajinomoto Co., Inc.

- Seppic

- Lonza

- Innospec

- Holiferm Ltd

- Solvay/Syensqo

- Miwon Commercial

The Global Bio-based Surfactants for Personal Care Market was valued at USD 11.1 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 20.9 billion by 2035.

Market expansion reflects the accelerating shift toward sustainable and biodegradable ingredients within the beauty and personal care industry. Bio-based surfactants used in personal care formulations include a broad portfolio of renewable technologies such as microbial-derived biosurfactants, amino acid-based surfactants, sugar-derived surfactants, bio-based ethoxylates, and other plant-origin alternatives developed through fermentation, enzymatic processing, and renewable feedstock synthesis. These ingredients are increasingly incorporated into hair care, skin care, oral hygiene, baby care, and specialty beauty products. Rising consumer awareness of environmental sustainability and ingredient transparency is significantly influencing purchasing decisions. Governments worldwide are promoting green chemistry frameworks, funding innovation in renewable formulations, and introducing regulatory policies that encourage the transition toward eco-conscious personal care manufacturing systems. Europe currently leads the global landscape, supported by strong regulatory backing and substantial investment in production infrastructure across major economies. Meanwhile, Asia Pacific is emerging as a high-growth region, driven by rapid industrial advancement, increased focus on natural beauty solutions, and expanding consumer preference for clean-label and environmentally responsible personal care products.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.1 Billion |

| Forecast Value | $20.9 Billion |

| CAGR | 6.3% |

The sugar-based surfactants segment accounted for 38% share in 2025 and is forecast to grow at a CAGR of 6.7% through 2035. Their growing prominence is attributed to their mild performance profile, high biodegradability, and suitability for sensitive skin formulations. These surfactants are widely adopted across diverse personal care categories due to their compatibility with natural and organic product positioning. Manufacturers favor sugar-derived solutions for their ability to deliver effective cleansing while aligning with clean beauty standards. The increasing demand for gentle, plant-based ingredients is accelerating the integration of sugar-based surfactants into next-generation cosmetic formulations.

The chemical synthesis from renewable feedstocks segment held 65.3% share in 2025 and is anticipated to grow at a CAGR of 6.2% by 2035. This production pathway plays a critical role in manufacturing a wide array of bio-based surfactants, including amino acid-derived variants, sugar-based surfactants, and bio-based ethoxylates. The approach leverages renewable raw materials processed through established chemical technologies known for scalability, operational efficiency, and consistent output quality. Compared to emerging biotechnology platforms, this method offers strong commercial viability and cost advantages, making it attractive for large-scale production. Rising investments in renewable feedstock supply chains and growing demand for dependable bio-based surfactant manufacturing are reinforcing the dominance of this technology platform.

North America Bio-based Surfactants for Personal Care Market is expected to register a CAGR of 6.7% between 2026 and 2035. Growth in the region is fueled by innovation in sustainable ingredient development and increased adoption of fermentation-based technologies aligned with green chemistry principles. Consumer concern regarding the ecological footprint of conventional surfactants is prompting brands to reformulate products with biodegradable and plant-derived alternatives. Expanding clean beauty movements, combined with regulatory encouragement for environmentally responsible manufacturing, are further stimulating demand across hair care, skin care, and specialty personal care segments.

Key companies operating in the Global Bio-based Surfactants for Personal Care Market include BASF SE, Croda International Plc, Clariant AG, Evonik Industries AG, Solvay / Syensqo, Galaxy Surfactants Ltd, Kao Corporation, Ajinomoto Co., Inc., Stepan Company, Innospec, Seppic, Lonza, Sino Lion, Miwon Commercial, and Holiferm Ltd. These companies are actively shaping competitive dynamics through innovation, sustainability commitments, and strategic expansion initiatives. Companies in the bio-based surfactants for personal care market are strengthening their market position by investing in advanced research and development focused on high-performance, biodegradable formulations. Strategic collaborations with beauty brands enable the co-creation of customized ingredients tailored to clean-label demands. Many firms are expanding manufacturing capacity for renewable feedstocks while improving supply chain transparency to meet sustainability benchmarks. Portfolio diversification into specialty and premium-grade surfactants supports differentiation in a competitive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Technology type

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Microbial biosurfactants

- 5.2.1 Glycolipids

- 5.2.1.1 Sophorolipids

- 5.2.1.2 Rhamnolipids

- 5.2.1.3 Mannosylerythritol lipids (MELs)

- 5.2.1.4 Trehalolipids

- 5.2.2 Lipopeptides

- 5.2.2.1 Surfactin

- 5.2.2.2 Iturin

- 5.2.2.3 Lichenysin

- 5.2.1 Glycolipids

- 5.3 Sugar-based surfactants

- 5.3.1 Alkyl polyglucosides (APGs)

- 5.3.2 Glucamides

- 5.3.3 Sucrose esters

- 5.3.4 Sorbitan esters

- 5.4 Amino acid-derived surfactants

- 5.4.1 Glutamates

- 5.4.2 Glycinates

- 5.4.3 Isethionates

- 5.4.4 Sarcosinates

- 5.4.5 Taurates

- 5.5 Bio-based ethoxylates

- 5.5.1 Bio-based alcohol ethoxylates

- 5.5.2 Bio-based polysorbates

- 5.5.3 Bio-based PEG derivatives

- 5.5.4 Bio-based castor oil ethoxylates

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Technology Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Microbial fermentation technology

- 6.3 Chemical synthesis from renewable feedstocks

- 6.4 Enzymatic synthesis

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Hair care

- 7.3 Skin care

- 7.4 Oral care

- 7.5 Baby care

- 7.6 Specialty personal care

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Clariant AG

- 9.3 Evonik Industries AG

- 9.4 Croda International Plc

- 9.5 Kao Corporation

- 9.6 Stepan Company

- 9.7 Sino Lion

- 9.8 Galaxy Surfactants Ltd

- 9.9 Ajinomoto Co., Inc.

- 9.10 Seppic

- 9.11 Lonza

- 9.12 Innospec

- 9.13 Holiferm Ltd

- 9.14 Solvay / Syensqo

- 9.15 Miwon Commercial

2026年全球生物基界面活性剂市场报告

2026年全球生物基界面活性剂市场报告 环保溶剂和生物溶剂市场规模、份额、趋势和预测:按类型、应用和地区划分,2026-2034年

环保溶剂和生物溶剂市场规模、份额、趋势和预测:按类型、应用和地区划分,2026-2034年 全球生物基界面活性剂市场2026年全球绿色溶剂市场报告

全球生物基界面活性剂市场2026年全球绿色溶剂市场报告 生物溶剂市场-全球产业规模、份额、趋势、机会及按类型、应用、地区和竞争格局分類的预测(2021-2031年)

生物溶剂市场-全球产业规模、份额、趋势、机会及按类型、应用、地区和竞争格局分類的预测(2021-2031年) 深共熔溶剂市场:按类型、成分、製造流程、形态、应用和最终用户划分 - 全球预测(2026-2032年)

深共熔溶剂市场:按类型、成分、製造流程、形态、应用和最终用户划分 - 全球预测(2026-2032年) 绿色溶剂和低VOC组合药物市场,全球预测至2032年:按溶剂类型、应用、最终用户和地区划分绿色溶剂和界面活性剂市场预测至2032年:按溶剂类型、界面活性剂类型、原料、应用和地区分類的全球分析

绿色溶剂和低VOC组合药物市场,全球预测至2032年:按溶剂类型、应用、最终用户和地区划分绿色溶剂和界面活性剂市场预测至2032年:按溶剂类型、界面活性剂类型、原料、应用和地区分類的全球分析 绿色溶剂市场规模、份额和成长分析(按类型、溶剂类型、纯度、应用、最终用途产业和地区划分)-产业预测,2026-2033年

绿色溶剂市场规模、份额和成长分析(按类型、溶剂类型、纯度、应用、最终用途产业和地区划分)-产业预测,2026-2033年 2025-2029年全球绿色与生物溶剂市场

2025-2029年全球绿色与生物溶剂市场