|

市场调查报告书

商品编码

1959313

人工智慧加速晶片市场机会、成长要素、产业趋势分析及预测(2026-2035年)AI Accelerator Chips Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

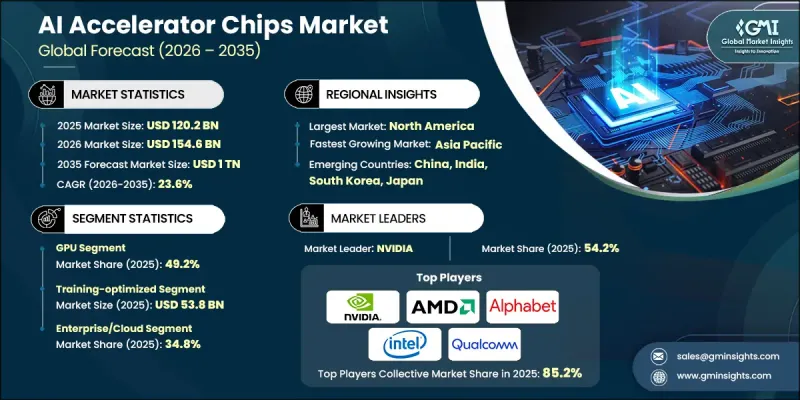

2025 年全球人工智慧加速器晶片市场价值 1,202 亿美元,预计到 2035 年将达到 1 兆美元,年复合成长率为 23.6%。

市场扩张的驱动力来自超大规模基础设施投资的增加、资料中心对高效能推理加速日益增长的需求,以及生成式人工智慧应用在企业中的快速商业化。企业越来越多地在云端原生、混合和本地环境中部署人工智慧工作负载,这就需要客製化设计的晶片,以实现更高的吞吐量、更低的延迟和更优异的能源效率。同时,边缘人工智慧用例的激增也增加了对紧凑、节能型加速器的需求,这些加速器能够实现更靠近资料来源的即时处理。随着模型架构的演进和运算复杂性的增加,企业正在优先考虑针对训练和推理任务最佳化的可扩展硬体解决方案。随着各产业对人工智慧驱动的自动化、预测分析和智慧决策系统的依赖性不断增强,对客製化加速器晶片的需求持续走强,从而创造了一个有望在2035年之前保持持续高速成长的市场环境。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 1202亿美元 |

| 预测金额 | 1兆美元 |

| 复合年增长率 | 23.6% |

人工智慧加速器晶片市场的主要成长要素之一是超大规模云端服务供应商对推理优化晶片的持续投入,这些晶片旨在管理大规模人工智慧服务交付。随着生成式人工智慧平台在全球的扩张,服务供应商必须平衡营运成本、运算效能和延迟。这加速了专为人工智慧推理工作负载量身定制的加速器的转变。同时,多个地区的政府正在大力投资其国家的半导体生态系统,以增强技术自主性并促进人工智慧晶片的创新。市场也正在经历从通用处理架构转向特定工作负载加速器设计的策略性转变。自2020年代初以来,模型架构的进步凸显了传统基于GPU的系统在性能和效率方面的局限性,促使人们转向更专业的晶片。随着人工智慧模型规模和复杂性的增加,预计这一演变将持续到2030年,这将推动每瓦效能效率的提升,并重塑整个软硬体协同设计生态系统的竞争格局。

到2025年,GPU市占率将达到49.2%。 GPU之所以能够持续占据主导地位,是因为它们能够灵活应对各种人工智慧工作负载,从大规模训练和推理到跨越超大规模资料中心和企业级人工智慧平台的混合运作模式。成熟的软体生态系统、与广泛采用的人工智慧开发框架的兼容性以及与现有运算基础设施的无缝集成,都极大地促进了GPU持续的市场领先地位。持续的架构改进和不断扩展的开发者工具链进一步巩固了GPU在大规模人工智慧部署中的竞争优势。

预计到2025年,训练优化领域的市场规模将达到538亿美元,主要得益于对大规模模型开发和基础人工智慧研究倡议的持续投入。超大规模超大规模资料中心业者、研究机构和企业都在大力投资建立日益复杂的模型,这些模型需要庞大的运算密度、高速互连和扩展的记忆体频宽。专注于训练的加速器旨在支援分散式运算环境和大规模资料集处理,从而加快高级人工智慧应用的收敛速度并提高其可扩展性。

预计到2025年,北美人工智慧加速器晶片市场份额将达到39.8%,这反映了该地区在人工智慧基础设施部署方面的领先地位。全部区域成长的驱动力包括大型资料中心的扩张、加速器与企业IT生态系统的融合,以及人工智慧在通讯和云端环境中的日益普及。推理优化和训练优化解决方案正被广泛部署,以支援生成式人工智慧服务、即时分析和高级自动化系统。该地区强大的技术生态系统、创业投资活动以及研发主导的创新,进一步巩固了其作为全球人工智慧加速器晶片产业主要成长中心的地位。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 对使用超大规模资料中心业者资料中心的人工智慧推理加速的需求

- 人工智慧加速器在通讯网路优化的应用日益广泛

- 政府对国内人工智慧半导体生态系统的投资

- 边缘人工智慧应用的发展需要低延迟处理

- 在企业范围内快速部署生成式人工智慧工作负载

- 产业潜在风险与挑战

- 高昂的开发成本和漫长的晶片设计週期

- 供应链对先进晶圆代工厂节点的依赖

- 市场机会

- 针对产业专用的工作负载的客製化人工智慧加速器

- 工业自动化中边缘人工智慧加速器的引入

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 地理位置比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 挑战者

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 主要进展

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张和投资策略

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估计与预测:依技术类型划分,2022-2035年

- NPU

- GPU

- ASIC

- FPGA

- 其他的

第六章 市场估算与预测:依工作量类型划分,2022-2035年

- 训练优化

- 推理优化

- 杂交种

第七章 市场估计与预测:依最终用途产业划分,2022-2035年

- 车

- 消费性电子产品

- 沟通

- 科学/高效能运算

- 企业/云端

- 其他(金融服务、工业、零售、媒体、医疗保健)

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第九章:公司简介

- 主要企业

- NVIDIA

- AMD(Advanced Micro Devices)

- Intel

- Google(Alphabet)

- Qualcomm

- Apple

- Huawei

- 按地区分類的主要企业

- 北美洲

- Cerebras Systems

- Groq

- SambaNova Systems

- Tenstorrent

- 亚太地区

- Cambricon Technologies

- Enflame Technology

- MetaX Integrated Circuits

- Iluvatar CoreX

- 欧洲

- Graphcore

- 北美洲

- 特殊玩家/干扰者

- Etched.ai

- Mythic AI

The Global AI Accelerator Chips Market was valued at USD 120.2 billion in 2025 and is estimated to grow at a CAGR of 23.6% to reach USD 1 trillion by 2035.

Market expansion is fueled by escalating hyperscale infrastructure investments, rising demand for high-performance inference acceleration in data centers, and the rapid commercialization of generative AI applications across enterprises. Organizations are increasingly deploying AI workloads across cloud-native, hybrid, and on-premise environments, requiring purpose-built silicon capable of delivering higher throughput, lower latency, and improved energy efficiency. Simultaneously, the proliferation of edge AI use cases is intensifying the need for compact, power-efficient accelerators that enable real-time processing closer to the data source. As model architectures evolve and computational complexity rises, enterprises are prioritizing scalable hardware solutions optimized for both training and inference tasks. The growing reliance on AI-driven automation, predictive analytics, and intelligent decision systems across industries continues to reinforce demand for specialized accelerator chips, positioning the market for sustained high-growth momentum through 2035.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $120.2 Billion |

| Forecast Value | $1 Trillion |

| CAGR | 23.6% |

A major growth catalyst for the AI accelerator chips market is the rising investment by hyperscale cloud providers in inference-optimized silicon designed to manage large-scale AI service delivery. As generative AI platforms expand globally, providers are under pressure to balance operational cost, computational performance, and latency. This has intensified the shift toward custom-designed accelerators tailored specifically for AI inference workloads. At the same time, governments across multiple regions are investing substantial funding in their domestic semiconductor ecosystems to strengthen technological sovereignty and accelerate AI chip innovation. The market has also witnessed a strategic pivot from general-purpose processing architectures toward workload-specific accelerator designs. Since the early 2020s, advancements in model architectures have highlighted performance and efficiency limitations in conventional GPU-based systems, prompting a transition to more specialized silicon. This evolution is expected to continue through 2030 as AI models increase in size and complexity, driving improvements in performance-per-watt efficiency and reshaping competition across both hardware and software co-design ecosystems.

In 2025, the GPU segment accounted for 49.2% share. GPUs continue to dominate due to their adaptability in handling diverse AI workloads, including large-scale training, inference, and mixed operational models across hyperscale data centers and enterprise AI platforms. Their mature software ecosystems, compatibility with widely adopted AI development frameworks, and seamless integration within existing computing infrastructure contribute significantly to their sustained market leadership. Continuous architectural enhancements and expanded developer toolchains further strengthen the competitive edge of GPUs in AI deployments at scale.

The training-optimized segment generated USD 53.8 billion in 2025, supported by ongoing investments in large model development and foundational AI research initiatives. Hyperscalers, research institutions, and enterprises are allocating substantial capital toward building increasingly complex models that require immense computational density, high-speed interconnectivity, and expanded memory bandwidth. Training-focused accelerators are engineered to support distributed computing environments and large dataset processing, enabling faster convergence times and improved scalability for advanced AI applications.

North America AI Accelerator Chips Market captured 39.8% share in 2025, reflecting strong regional leadership in AI infrastructure deployment. Growth across the region is driven by large-scale data center expansion, integration of accelerators into enterprise IT ecosystems, and increasing AI adoption within telecom and cloud environments. Both inference-optimized and training-optimized solutions are being deployed extensively to support generative AI services, real-time analytics, and advanced automation systems. The region's robust technology ecosystem, venture capital activity, and research-driven innovation further solidify its position as a key growth hub within the global AI accelerator chips industry.

Key companies operating in the Global AI Accelerator Chips Market include NVIDIA, AMD (Advanced Micro Devices), Intel, Qualcomm, Apple, Huawei, Google (Alphabet), Graphcore, Cerebras Systems, SambaNova Systems, Groq, Tenstorrent, Cambricon Technologies, Mythic AI, Enflame Technology, Etched.ai, Iluvatar CoreX, and MetaX Integrated Circuits. These industry participants compete through architectural innovation, proprietary software ecosystems, vertical integration strategies, and strategic partnerships aimed at capturing expanding demand across cloud, enterprise, and edge AI segments. Companies in the AI Accelerator Chips Market are strengthening their competitive positions through aggressive investment in research and development, focusing on workload-specific chip architectures and energy-efficient designs. Strategic collaborations with hyperscalers, cloud providers, and enterprise customers enable co-development of customized silicon tailored to targeted AI applications. Many firms are building vertically integrated ecosystems that combine hardware, software frameworks, and developer tools to enhance customer retention and platform stickiness. Geographic expansion and domestic manufacturing initiatives are also prioritized to mitigate supply chain risks and align with government semiconductor policies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Technology type trends

- 2.2.2 Workload type trends

- 2.2.3 End-use industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Hyperscaler demand for data-center AI inference acceleration

- 3.2.1.2 Expanding use of AI accelerators in telecom network optimization

- 3.2.1.3 Government investments in domestic AI semiconductor ecosystems

- 3.2.1.4 Growth of edge AI applications requiring low-latency processing

- 3.2.1.5 Rapid deployment of generative AI workloads across enterprises

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development costs and long chip design cycles

- 3.2.2.2 Supply chain dependence on advanced foundry nodes

- 3.2.3 Market opportunities

- 3.2.3.1 Custom AI accelerators for industry-specific workloads

- 3.2.3.2 Edge AI accelerator adoption in industrial automation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 NPU

- 5.3 GPU

- 5.4 ASIC

- 5.5 FPGA

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Workload Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Training-optimized

- 6.3 Inference-optimized

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Consumer electronics

- 7.4 Telecommunications

- 7.5 Scientific/HPC

- 7.6 Enterprise/cloud

- 7.7 Others (financial services, industrial, retail, media, healthcare)

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 NVIDIA

- 9.1.2 AMD (Advanced Micro Devices)

- 9.1.3 Intel

- 9.1.4 Google (Alphabet)

- 9.1.5 Qualcomm

- 9.1.6 Apple

- 9.1.7 Huawei

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 Cerebras Systems

- 9.2.1.2 Groq

- 9.2.1.3 SambaNova Systems

- 9.2.1.4 Tenstorrent

- 9.2.2 Asia Pacific

- 9.2.2.1 Cambricon Technologies

- 9.2.2.2 Enflame Technology

- 9.2.2.3 MetaX Integrated Circuits

- 9.2.2.4 Iluvatar CoreX

- 9.2.3 Europe

- 9.2.3.1 Graphcore

- 9.2.1 North America

- 9.3 Niche Players/Disruptors

- 9.3.1 Etched.ai

- 9.3.2 Mythic AI

人工智慧加速器晶片市场预测至2034年-全球分析(按晶片类型、处理类型、部署类型、记忆体类型、资料中心类型、技术、应用、产业、最终用户和地区划分)

人工智慧加速器晶片市场预测至2034年-全球分析(按晶片类型、处理类型、部署类型、记忆体类型、资料中心类型、技术、应用、产业、最终用户和地区划分) 人工智慧加速器市场分析及预测(至2035年):类型、产品、技术、组件、应用、部署、最终用户、功能、安装配置

人工智慧加速器市场分析及预测(至2035年):类型、产品、技术、组件、应用、部署、最终用户、功能、安装配置 2026年全球人工智慧加速器市场报告

2026年全球人工智慧加速器市场报告 人工智慧加速器市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

人工智慧加速器市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 人工智慧加速器市场:2026-2032年全球预测(按加速器类型、应用、最终用户产业、部署类型和组织规模划分)人工智慧加速晶片市场:按产品类型、架构、应用和最终用户划分,全球预测(2026-2032年)

人工智慧加速器市场:2026-2032年全球预测(按加速器类型、应用、最终用户产业、部署类型和组织规模划分)人工智慧加速晶片市场:按产品类型、架构、应用和最终用户划分,全球预测(2026-2032年) TPU vs. GPU:2025 年 AI 加速器市场惊人前景NVIDIA H200 在中国市场的策略展望(2026 年)Frost Radar:边缘人工智慧加速器,2025

TPU vs. GPU:2025 年 AI 加速器市场惊人前景NVIDIA H200 在中国市场的策略展望(2026 年)Frost Radar:边缘人工智慧加速器,2025 2025-2029年全球AI加速器市场

2025-2029年全球AI加速器市场