|

市场调查报告书

商品编码

1959318

2026 年至 2035 年航太高性能热塑性塑胶市场的市场机会、成长要素、产业趋势分析与预测。High-Performance Thermoplastics in Aerospace Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

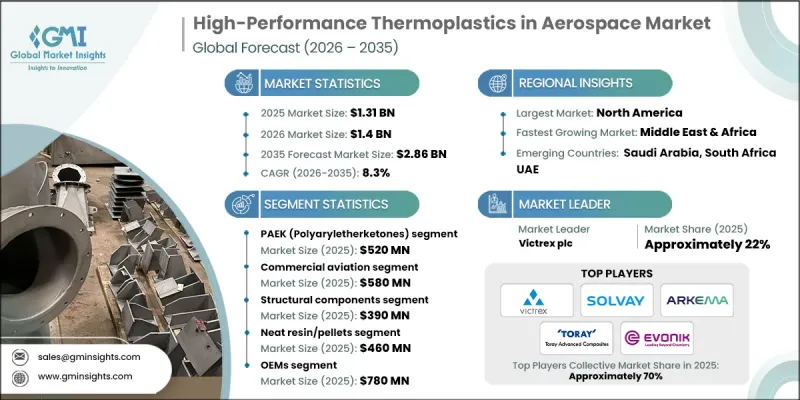

2025 年全球航太领域高性能热塑性塑胶市场价值为 13.1 亿美元,预计到 2035 年将达到 28.6 亿美元,年复合成长率为 8.3%。

航太业对轻质高强度材料的需求不断增长,推动了市场成长。这些材料有助于提高燃油效率并降低营运成本。航太製造商正推动从传统金属和热固性树脂转向高性能热塑性塑胶。这些聚合物具有卓越的热稳定性、机械强度和耐腐蚀性,同时也能减轻飞机的整体重量。先进聚合物科学的进步提高了这些材料的耐久性和性能,使其适用于关键结构部件。此外,人们对永续性关注以及更严格的排放法规,也推动了对环境影响较小的可再生热塑性塑胶的采用。这些材料能够承受极端温度和恶劣的化学环境,从而延长民用航空、国防和公务航空领域的使用寿命,减少维护週期,并提高可靠性。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 13.1亿美元 |

| 预测金额 | 28.6亿美元 |

| 复合年增长率 | 8.3% |

预计到2025年,聚芳醚酮(PAEK)市场规模将达到5.2亿美元,并在2026年至2035年间以7.8%的复合年增长率成长。 PAEK材料因其优异的耐热性和严苛的机械性能,在航太领域日益受到青睐。其耐化学性和耐热性使其成为结构件和半结构件的理想选择。同样,聚酰亚胺也因其出色的尺寸稳定性和耐热性而备受关注,尤其是在引擎周围和其他高温区域等极端温度环境下。这些材料的独特性能使航太工程师能够设计出更轻、更有效率且能承受严苛运作条件的飞机。

预计到2025年,民用航空市场规模将达到5.8亿美元,并在2026年至2035年间以7.9%的复合年增长率成长。飞机製造量的增加、机身现代化改造以及对效率提升的追求,推动了对用于机身结构、内饰和机载系统的高性能热塑性塑料的需求。军用和国防航空领域也为市场成长做出了贡献,需要能够承受严苛运作环境并具有长使用寿命的材料。在公务航空和通用航空领域,先进热塑性塑胶的应用日益广泛,旨在应对传统航太材料的复杂性和成本挑战,从而提升性能并简化製造流程。

预计到2025年,北美航太高性能热塑性塑胶市场规模将达到4.9亿美元。该地区市场扩张的驱动力包括先进的飞机製造技术、研发带来的持续材料创新以及自动化製造技术的早期应用。北美受益于成熟的航太供应链和对下一代飞机项目的持续投资。美国正透过增加民航机交付、推进军事现代化项目以及将轻质高性能热塑性塑胶整合到结构和系统部件中,推动区域市场成长。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监理情势

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 副产品

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依材料类型划分,2022-2035年

- PAEK(聚芳醚酮)

- PEEK(聚醚醚酮)

- PEKK(聚醚酮酮)

- LM-PAEK(低熔点PAEK)

- 聚酰亚胺

- PEI(聚醚酰亚胺/Artem)

- PAI(聚酰胺-酰亚胺)

- 聚砜

- 聚亚苯硫醚(PPS)

- 其他高性能热塑性树脂

第六章 市场估算与预测:依飞机平台划分,2022-2035年

- 商业航空

- 窄体飞机

- 宽体飞机

- 军事/国防航空

- 战斗机

- 军用运输机

- 军用直升机

- 商务及通用航空

- 空间应用

- 其他的

第七章 市场估计与预测:依组件类型划分,2022-2035年

- 结构部件

- 主体结构

- 二级结构

- 内部零件

- 座椅和座椅框架

- 厨房和卫生间

- 头顶置物箱

- 侧墙和天花板麵板

- 窗框和装饰条

- 引擎和推进系统部件

- 引擎室和引擎罩

- 反推装置

- 管道和空气管理系统

- 风扇叶片和隔音衬里

- 电气和电子设备机壳

- 雷达罩和天线外壳

- 航空电子设备机壳

- 线缆管理系统

- 电磁干扰/射频干扰屏蔽要求

- 透明部件和窗户

- 飞机舷窗和挡风玻璃

- (军用)座舱罩

- 聚碳酸酯和丙烯酸树脂的比较分析

- 前缘和气动表面

- 主翼前缘

- 控制面

- 空气力学整流罩

第八章 市场估算与预测:依产品类型划分,2022-2035年

- 纯树脂/颗粒

- 预孕

- 单向(UD)胶带

- 纺织预浸料

- 半成品

- 板材和层压板

- 薄膜和膜

- 型材和挤压产品

- 成品零件/组件

第九章 市场估价与预测:依製造流程划分,2022-2035年

- 自动光纤铺放(AFP)和自动胶带铺放(ATP)

- 压缩成型和压製成型

- 热成型

- 射出成型

- 积层製造(AM)

- 焊接和连接技术

- 电阻焊接

- 感应焊接

- 超音波焊接

- 雷射焊接

- 连续压缩成型(CCM)

第十章 市场估价与预测:依最终用户划分,2022-2035年

- OEM(原始设备製造商)

- MRO(维修、修理和大修)服务供应商

- 研究机构和学术机构

- 其他的

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十二章:公司简介

- Victrex plc

- Solvay Special Chemicals

- Arkema SA

- Evonik Industries AG

- SABIC

- BASF SE

- Envalior

- Toray Advanced Composites

- Teijin Limited

- Celanese Corporation

- Mitsubishi Chemical Group

- Rochling Group

- Syensqo

- Ensinger GmbH

The Global High-Performance Thermoplastics in Aerospace Market was valued at USD 1.31 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 2.86 billion by 2035.

Market growth is driven by the aerospace industry's increasing need for lightweight, high-strength materials that can improve fuel efficiency and reduce operational costs. Aerospace manufacturers are progressively replacing traditional metals and thermosets with high-performance thermoplastics, as these polymers offer superior thermal stability, mechanical strength, and corrosion resistance while reducing overall aircraft weight. The development of advanced polymer science has enhanced the durability and performance of these materials, making them suitable for critical structural components. Sustainability concerns and stricter emissions regulations are also pushing the adoption of recyclable thermoplastics with lower environmental impact. Their ability to endure extreme temperatures and harsh chemical environments ensures longer service life, fewer maintenance cycles, and increased reliability across commercial, defense, and business aviation applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.31 Billion |

| Forecast Value | $2.86 Billion |

| CAGR | 8.3% |

The PAEK (Polyaryletherketones) segment generated USD 0.52 billion in 2025 and is estimated to grow at a CAGR of 7.8% between 2026 and 2035. PAEK materials are increasingly preferred for aerospace applications requiring high thermal tolerance and demanding mechanical performance. Their chemical and thermal resilience make them ideal for structural and semi-structural components. Similarly, polyimides are gaining traction in regions exposed to extreme heat, such as areas near engines or other high-temperature zones, due to their exceptional dimensional stability and heat resistance. The unique properties of these materials enable aerospace engineers to design lighter and more efficient aircraft capable of withstanding rigorous operating conditions.

The commercial aviation segment reached USD 0.58 billion in 2025 and is expected to grow at a CAGR of 7.9% from 2026 to 2035. The rise in aircraft manufacturing, fleet modernization, and the push for improved efficiency are driving demand for high-performance thermoplastics in airframes, interiors, and onboard systems. Military and defense aviation is also contributing to growth, as these sectors demand materials capable of enduring harsh operational conditions while offering long service life. Business and general aviation platforms are increasingly utilizing advanced thermoplastics to enhance performance and simplify manufacturing processes, addressing the complexity and cost of traditional aerospace materials.

North America High-Performance Thermoplastics in Aerospace Market accounted for USD 0.49 billion in 2025. Market expansion in the region is fueled by advanced aircraft production, continuous material innovation through research and development, and early adoption of automated manufacturing technologies. North America benefits from a well-established aerospace supply chain and ongoing investment in next-generation aircraft programs. The U.S. is leading regional growth due to rising commercial aircraft deliveries, military modernization programs, and the integration of lightweight, high-performance thermoplastics in both structural and system components.

Key players operating in the Global High-Performance Thermoplastics in Aerospace Market include Solvay Special Chemicals, Victrex plc, Toray Advanced Composites, Evonik Industries AG, Arkema S.A., and several others. Companies in the high-performance thermoplastics in the aerospace market are focusing on strategic growth initiatives to strengthen their market foothold. They are investing heavily in research and development to create advanced thermoplastic materials with higher thermal tolerance, mechanical strength, and chemical resistance to meet evolving aerospace demands. Expanding production capabilities and forming partnerships with aerospace OEMs allow companies to integrate their solutions into cutting-edge aircraft designs. Firms are also emphasizing sustainability by developing recyclable materials with lower environmental impact, improving lifecycle performance, and reducing maintenance needs.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Aircraft Platform

- 2.2.4 Component Type

- 2.2.5 Product Type

- 2.2.6 Manufacturing Process

- 2.2.7 End-User

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 PAEK (Polyaryletherketones)

- 5.2.1 PEEK (Polyetheretherketone)

- 5.2.2 PEKK (Polyetherketoneketone)

- 5.2.3 LM-PAEK (Low-Melt PAEK)

- 5.3 Polyimides

- 5.3.1 PEI (Polyetherimide/Ultem)

- 5.3.2 PAI (Polyamideimide)

- 5.4 Polysulfones

- 5.5 PPS (Polyphenylene Sulfide)

- 5.6 Other High-Performance Thermoplastics

Chapter 6 Market Estimates and Forecast, By Aircraft Platform, 2022 - 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Commercial Aviation

- 6.2.1 Narrow-Body Aircraft

- 6.2.2 Wide-Body Aircraft

- 6.3 Military & Defense Aviation

- 6.3.1 Fighter Aircraft

- 6.3.2 Military Transport Aircraft

- 6.3.3 Military Helicopters

- 6.4 Business & General Aviation

- 6.5 Space Applications

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Component Type, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Structural Components

- 7.2.1 Primary Structures

- 7.2.2 Secondary Structures

- 7.3 Interior Components

- 7.3.1 Seats & Seat Frames

- 7.3.2 Galleys & Lavatories

- 7.3.3 Overhead Stow Bins

- 7.3.4 Sidewall & Ceiling Panels

- 7.3.5 Window Reveals & Trim

- 7.4 Engine & Propulsion Components

- 7.4.1 Nacelles & Engine Cowlings

- 7.4.2 Thrust Reversers

- 7.4.3 Ducts & Air Management Systems

- 7.4.4 Fan Blades & Acoustic Liners

- 7.5 Electrical & Electronic Housings

- 7.5.1 Radomes & Antenna Housings

- 7.5.2 Avionics Enclosures

- 7.5.3 Cable Management Systems

- 7.5.4 EMI/RFI Shielding Requirements

- 7.6 Transparencies & Windows

- 7.6.1 Aircraft Windows & Windshields

- 7.6.2 Canopies (Military Applications)

- 7.6.3 Polycarbonate vs. Acrylic Analysis

- 7.7 Leading Edges & Aerodynamic Surfaces

- 7.7.1 Wing Leading Edges

- 7.7.2 Control Surfaces

- 7.7.3 Aerodynamic Fairings

Chapter 8 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Neat Resin/Pellets

- 8.3 Prepregs

- 8.3.1 Unidirectional (UD) Tape

- 8.3.2 Woven Fabric Prepregs

- 8.4 Semi-Finished Products

- 8.4.1 Sheets & Laminates

- 8.4.2 Films & Membranes

- 8.4.3 Profiles & Extruded Shapes

- 8.5 Finished Parts/Components

Chapter 9 Market Estimates and Forecast, By Manufacturing Process, 2022 - 2035 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 Automated Fiber Placement (AFP) & Automated Tape Placement (ATP)

- 9.3 Compression Molding & Stamp Forming

- 9.4 Thermoforming

- 9.5 Injection Molding

- 9.6 Additive Manufacturing (AM)

- 9.7 Welding & Joining Technologies

- 9.7.1 Resistance Welding

- 9.7.2 Induction Welding

- 9.7.3 Ultrasonic Welding

- 9.7.4 Laser Welding

- 9.8 Continuous Compression Molding (CCM)

Chapter 10 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Billion, Kilo Tons)

- 10.1 Key trends

- 10.2 OEMs (Original Equipment Manufacturers)

- 10.3 MRO (Maintenance, Repair & Overhaul) Providers

- 10.4 Research Institutions & Academia

- 10.5 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East & Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East & Africa

Chapter 12 Company Profiles

- 12.1 Victrex plc

- 12.2 Solvay Special Chemicals

- 12.3 Arkema S.A.

- 12.4 Evonik Industries AG

- 12.5 SABIC

- 12.6 BASF SE

- 12.7 Envalior

- 12.8 Toray Advanced Composites

- 12.9 Teijin Limited

- 12.10 Celanese Corporation

- 12.11 Mitsubishi Chemical Group

- 12.12 Rochling Group

- 12.13 Syensqo

- 12.14 Ensinger GmbH

航太热塑性塑胶市场-全球产业规模、份额、趋势、机会及预测,依平台类型、应用类型、形态类型、地区及竞争格局划分,2020-2030年预测

航太热塑性塑胶市场-全球产业规模、份额、趋势、机会及预测,依平台类型、应用类型、形态类型、地区及竞争格局划分,2020-2030年预测 航太用热塑性塑胶复合材料市场:全球产业分析,规模,占有率,成长,趋势,2024~2031年预测

航太用热塑性塑胶复合材料市场:全球产业分析,规模,占有率,成长,趋势,2024~2031年预测