|

市场调查报告书

商品编码

1959319

云端合规市场机会、成长要素、产业趋势分析及2026年至2035年预测Cloud Compliance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

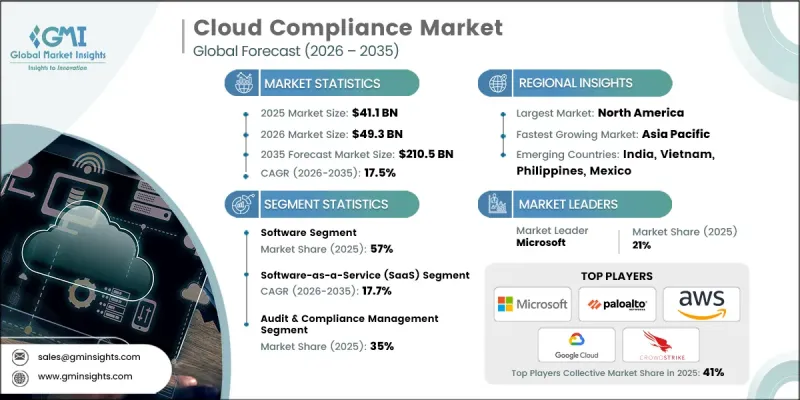

2025 年全球云端合规市场价值为 411 亿美元,预计到 2035 年将达到 2,105 亿美元,年复合成长率为 17.5%。

随着企业加速向公有云、私有云和混合云端环境迁移,工作负载、身分、配置和资料资产等方面的合规复杂性急剧增加。随着企业将应用程式分布在多个云端基础架构上,维护一致的管治和策略执行变得更加具有挑战性。对不同云端服务供应商和私人基础设施的依赖性日益增强,容易导致可见性分散,从而对集中式合规编配和自动化监控平台产生了强烈的需求。企业正在优先采用持续监控框架,以大规模地满足内部管治标准和不断变化的监管要求。通讯业正在加速采用整合安全态势管理和应用程式保护功能的统一安全合规架构。此外,不断扩展的资料保护条例和特定产业义务增加了合规风险,因此需要投资于自动化证据收集和报告系统。即时合规追踪正在逐步取代传统的定期审核,推动了基于 SaaS 的合规解决方案的普及,这些解决方案提供敏捷性、扩充性和主动风险缓解功能。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 411亿美元 |

| 预测金额 | 2105亿美元 |

| 复合年增长率 | 17.5% |

预计到2025年,软体领域将占据57%的市场份额,并在2026年至2035年间以16.6%的复合年增长率成长。合规平台正从独立的姿态管理工具演变为整合身分管治、工作负载保护、组态管理和资料安全控制的生态系统。这种转变正在推动企业内部工具的集成,以期提高跨云端可见度和营运效率。软体供应商正在将合规性检验功能直接整合到开发平臺和基础设施自动化工作流程中,从而在配置生命週期的早期阶段检测违规行为。将合规性检查整合到DevOps和平台工程流程中,能够帮助企业降低补救成本、加速云端部署,并增强整个技术团队的课责。这些进展进一步强化了软体主导的合规框架在复杂的多重云端环境中的优势。

软体即服务(SaaS) 预计到 2025 年将占据 52% 的市场份额,并在 2026 年至 2035 年期间以 17.7% 的复合年增长率增长。基于 SaaS 的合规解决方案能够持续监控外部託管应用程式的资料存取控制、使用者行为和设定一致性。随着企业快速采用云端原生平台,维护第三方系统的可见性和管治变得日益重要。 SaaS 合规工具提供集中式管理仪表板、自动化报告功能和可用于审核的文檔,协助组织保护敏感资料、执行身分管理标准并维持合规性。 SaaS 交付模式的柔软性和扩充性持续推动着各种规模的企业采用此模式。

预计2025年,美国云端合规市场规模将达141亿美元。美国企业正在将多种安全和合规解决方案整合到整合的云端原生保护平台中,以简化监管合规流程并降低营运复杂性。这种整合减少了工具重复,增强了审核应对力,并实现了对混合云和多重云端工作负载的持续监控。人工智慧 (AI) 驱动的风险优先排序技术正在被广泛采用,使企业能够识别高影响力的合规问题,并自动执行跨职能、协调一致的纠正工作流程。 AI 驱动的分析技术透过最大限度地减少误报并促进 IT 营运团队和安全团队之间的更紧密协作,提高了营运效率。这些发展正在使美国成为先进云端合规创新领域的领先中心。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 加速云端迁移

- 多重云端和混合环境的复杂性

- 日益增长的资料隐私和安全义务

- 向持续合规自动化过渡

- 产业潜在风险与挑战

- 高昂的实施和整合成本

- 熟练的云端合规专家短缺

- 市场机会

- 中小企业的合规自动化

- 託管云端合规服务

- 与 DevSecOps 和 CI/CD 流水线集成

- 公共部门和政府机构的云端采用情况

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国国家标准与技术研究院(NIST)

- 联邦风险授权管理计划 (FedRAMP)

- 欧洲

- 欧洲资料保护委员会(EDPB)

- 欧洲网路安全局 (ENISA)

- 亚太地区

- 新加坡个人资料保护委员会(PDPC)

- 资讯科技促进机构(IPA)

- 拉丁美洲

- 巴西国家资料保护局(ANPD)

- 墨西哥国家资讯自由与个人资料保护委员会(INAI)

- 中东和非洲

- 阿联酋资料管理局/人工智慧部/联邦身分和公民权办公室

- 南非资讯监理局(SAIR)

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

- 用例

- 投资与资金筹措分析

- 风险与网路安全暴露分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估计与预测:依组件划分,2022-2035年

- 软体

- 服务

第六章 市场估算与预测:依部署模式划分,2022-2035年

- 软体即服务(SaaS)

- 基础设施即服务 (IaaS)

- 平台即服务 (PaaS)

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 审核和合规管理

- 威胁侦测与补救

- 活动监测与分析

- 可见性和风险评估

- 其他的

第八章 市场估计与预测:依公司规模划分,2022-2035年

- 大公司

- 中小企业

第九章 市场估计与预测:依最终用途划分,2022-2035年

- BFSI

- 资讯科技/通讯

- 卫生保健

- 政府/公共部门

- 零售和消费品

- 製造业

- 能源与公共产业

- 其他的

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 俄罗斯

- 波兰

- 罗马尼亚

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ANZ

- 越南

- 印尼

- 菲律宾

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章:公司简介

- 世界公司

- Amazon Web Services(AWS)

- Check Point Software Technologies

- CrowdStrike

- Fortinet

- Google Cloud(Alphabet Inc.)

- IBM

- Microsoft

- Palo Alto Networks

- Qualys

- Trend Micro

- 本地球员

- Aqua Security

- Lacework(Fortinet)

- Orca Security

- Rapid7

- SentinelOne

- Snyk

- Sysdig

- Tenable

- Wiz

- Zscaler

- 新兴企业

- Horangi Cyber Security

- Scrut Automation

- Secureframe

- Vanta

The Global Cloud Compliance Market was valued at USD 41.1 billion in 2025 and is estimated to grow at a CAGR of 17.5% to reach USD 210.5 billion by 2035.

Accelerated enterprise migration toward public, private, and hybrid cloud environments is significantly increasing compliance complexity across workloads, identities, configurations, and data assets. As organizations distribute applications across multiple cloud infrastructures, maintaining consistent governance and policy enforcement has become more challenging. The growing reliance on diverse cloud service providers alongside private infrastructure often results in fragmented visibility, creating a strong demand for centralized compliance orchestration and automated oversight platforms. Enterprises are prioritizing continuous monitoring frameworks to satisfy both internal governance standards and evolving regulatory requirements at scale. Industries such as financial services and telecommunications are increasingly deploying unified security and compliance architectures that consolidate posture management and application protection capabilities. Additionally, expanding data protection regulations and sector-specific mandates are intensifying compliance exposure, compelling businesses to invest in automated evidence collection and reporting systems. Real-time compliance tracking is gradually replacing traditional periodic audits, driving widespread adoption of SaaS-based compliance solutions that offer agility, scalability, and proactive risk mitigation.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $41.1 Billion |

| Forecast Value | $210.5 Billion |

| CAGR | 17.5% |

The software segment accounted for 57% share in 2025 and is anticipated to grow at a CAGR of 16.6% from 2026 to 2035. Compliance platforms are evolving from standalone posture management tools into integrated ecosystems that unify identity governance, workload protection, configuration management, and data security controls. This transition is encouraging tool consolidation within enterprises seeking improved cross-cloud visibility and operational efficiency. Software providers are embedding compliance validation directly into development pipelines and infrastructure automation workflows to detect violations earlier in the deployment lifecycle. By incorporating compliance checks within DevOps and platform engineering processes, organizations can reduce remediation expenses, accelerate cloud rollouts, and strengthen accountability across technical teams. These advancements are reinforcing the dominance of software-driven compliance frameworks in complex multi-cloud environments.

The Software-as-a-Service segment held a 52% share in 2025 and is forecast to grow at a CAGR of 17.7% between 2026 and 2035. SaaS-based compliance solutions deliver continuous monitoring of data access controls, user behavior, and configuration integrity across externally hosted applications. As enterprises rapidly deploy cloud-native platforms, maintaining visibility and governance across third-party systems becomes increasingly critical. SaaS compliance tools provide centralized dashboards, automated reporting capabilities, and audit-ready documentation that help organizations safeguard sensitive data, enforce identity management standards, and maintain regulatory readiness. The flexibility and scalability of SaaS delivery models continue to drive adoption across enterprises of all sizes.

United States Cloud Compliance Market reached USD 14.1 billion in 2025. Across the country, enterprises are consolidating multiple security and compliance solutions into unified cloud-native protection platforms to streamline regulatory adherence and reduce operational complexity. This consolidation reduces redundant tooling, enhances audit preparedness, and enables continuous oversight of hybrid and multi-cloud workloads. Adoption of artificial intelligence-driven risk prioritization is expanding, allowing organizations to identify high-impact compliance gaps and automate coordinated remediation workflows across departments. AI-powered analytics are improving operational efficiency by minimizing false alerts and fostering closer collaboration between IT operations and security teams. These developments are positioning the United States as a leading hub for advanced cloud compliance innovation.

Major companies operating in the Global Cloud Compliance Market include Palo Alto Networks, Microsoft, Google Cloud, Amazon Web Services (AWS), Check Point Software, CrowdStrike, Fortinet, Trend Micro, Qualys, and Wiz. These providers compete by delivering integrated compliance, security, and risk management platforms designed to address evolving regulatory landscapes and multi-cloud operational demands. Companies in the Global Cloud Compliance Market are reinforcing their competitive standing through platform consolidation, AI-driven automation, and expanded multi-cloud interoperability. Vendors are investing in advanced analytics and machine learning models to deliver predictive compliance insights and automated remediation capabilities. Strategic partnerships with cloud providers and enterprise clients enable deeper integration across hybrid infrastructures. Many firms are enhancing developer-focused tools that embed compliance validation within CI/CD pipelines to promote proactive governance. In addition, providers are expanding global data center footprints and compliance certifications to meet regional regulatory standards.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment model

- 2.2.4 Application

- 2.2.5 Enterprise size

- 2.2.6 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Accelerated cloud migration

- 3.2.1.2 Multi-cloud and hybrid complexity

- 3.2.1.3 Rising data privacy and security obligations

- 3.2.1.4 Shift to continuous compliance automation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and integration costs

- 3.2.2.2 Shortage of skilled cloud compliance professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Compliance automation for SMBs

- 3.2.3.2 Managed cloud compliance services

- 3.2.3.3 Integration with DevSecOps and CI/CD pipelines

- 3.2.3.4 Public sector and government cloud adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Institute of Standards and Technology (NIST)

- 3.4.1.2 Federal Risk and Authorization Management Program (FedRAMP)

- 3.4.2 Europe

- 3.4.2.1 European Data Protection Board (EDPB)

- 3.4.2.2 ENISA (European Union Agency for Cybersecurity)

- 3.4.3 Asia Pacific

- 3.4.3.1 Singapore Personal Data Protection Commission (PDPC)

- 3.4.3.2 Japan Information-technology Promotion Agency (IPA)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Data Protection Authority (ANPD)

- 3.4.4.2 Mexico National Institute for Transparency, Access to Information and Personal Data Protection (INAI)

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Data Office / Ministry of Artificial Intelligence & Federal Authority for Identity and Citizenship

- 3.4.5.2 South Africa Information Regulator (SAIR)

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Investment & funding analysis

- 3.13 Risk & cybersecurity exposure analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

Chapter 6 Market Estimates & Forecast, By Deployment model, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Software-as-a-Service (SaaS)

- 6.3 Infrastructure-as-a-Service (IaaS)

- 6.4 Platform-as-a-Service (PaaS)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Audit & compliance management

- 7.3 Threat detection & remediation

- 7.4 Activity monitoring & analytics

- 7.5 Visibility & risk assessment

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Enterprise size, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Large enterprises

- 8.3 Small & medium enterprises (SMEs)

Chapter 9 Market Estimates & Forecast, By End use, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 IT & telecommunications

- 9.4 Healthcare

- 9.5 Government & public sector

- 9.6 Retail & consumer goods

- 9.7 Manufacturing

- 9.8 Energy & utilities

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.4.8 Philippines

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 Amazon Web Services (AWS)

- 11.1.2 Check Point Software Technologies

- 11.1.3 CrowdStrike

- 11.1.4 Fortinet

- 11.1.5 Google Cloud (Alphabet Inc.)

- 11.1.6 IBM

- 11.1.7 Microsoft

- 11.1.8 Palo Alto Networks

- 11.1.9 Qualys

- 11.1.10 Trend Micro

- 11.2 Regional players

- 11.2.1 Aqua Security

- 11.2.2 Lacework (Fortinet)

- 11.2.3 Orca Security

- 11.2.4 Rapid7

- 11.2.5 SentinelOne

- 11.2.6 Snyk

- 11.2.7 Sysdig

- 11.2.8 Tenable

- 11.2.9 Wiz

- 11.2.10 Zscaler

- 11.3 Emerging players

- 11.3.1 Horangi Cyber Security

- 11.3.2 Scrut Automation

- 11.3.3 Secureframe

- 11.3.4 Vanta