|

市场调查报告书

商品编码

1959322

Ultracruise 与城市自动驾驶市场机会、成长要素、产业趋势分析及 2026 年至 2035 年预测Ultra Cruise and City-Street Autonomous Driving Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

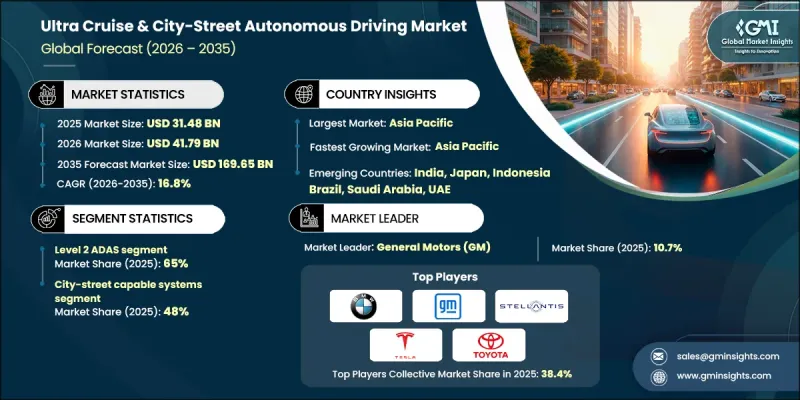

2025 年全球超巡航和城市自动驾驶市场价值为 314.8 亿美元,预计到 2035 年将以 16.8% 的复合年增长率增长至 1696.5 亿美元。

先进的免手驾驶和城市级自动化技术的融合正在重塑车辆设计、内建软体框架以及下一代出行解决方案。汽车製造商正从孤立的驾驶辅助功能转向自适应的软体定义驾驶平台,以支援逐步升级的自动驾驶,同时保持人工监控。都市区驾驶环境,包括拥塞、难以预测的道路使用者以及不完善的基础设施,对城市自动驾驶系统提出了更高的性能要求。这些解决方案依赖先进的感测器整合、持续的环境感知和高速运算来管理交叉路口、号誌灯、车道变换和复杂的交通流。由于车辆在特定的运行设计范围内运行,这些技术对于将自动驾驶从封闭道路扩展到日常城市使用至关重要。汽车製造商和技术供应商正在大力投资可扩展的自动驾驶技术栈,优先考虑透过软体更新和逐步扩展功能来保障安全性和可靠性,而不是立即部署完全自动驾驶。这种分阶段的方法有助于符合监管要求、赢得消费者信任并实现快速商业化。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 314.8亿美元 |

| 预测金额 | 1696.5亿美元 |

| 复合年增长率 | 16.8% |

预计到2025年,L2级高级驾驶辅助系统(ADAS)将占据65%的市场份额,并在2035年之前以16.5%的复合年增长率成长。这个细分市场占据主导地位,因为它在提供先进自动化功能的同时,仍保留了驾驶员的监督,这使得监管核准和市场部署在各个地区都更加现实可行。现有的安全标准、责任框架和认证流程都为监督式自动驾驶提供了强有力的支持,使其部署速度比更高级别的自动驾驶更快。

预计到2025年,城市道路适用型自动驾驶系统将占据48%的市场份额,并在2026年至2035年间维持17.8%的复合年增长率。这些系统逐渐成为主流,因为它们能够满足日常驾驶环境的需求,而这正是大多数车辆使用情境。都市区驾驶涉及频繁的停车、十字路口、弱势道路使用者以及复杂的交通状况,因此,针对都市区环境的自动驾驶解决方案比仅适用于高速公路的解决方案更有价值。消费者对减轻城市通勤、停车和短程出行压力的需求不断增长,也持续加速这些系统的普及。

预计到2025年,美国超高速巡航和都市区自动驾驶市场将占据85%的市场份额,市场规模将达到92亿美元。美国市场正保持强劲成长,这得益于高级驾驶辅助系统和监督式自动驾驶解决方案的持续创新,以及领先汽车製造商的大量投资。高度发展的软体定义车辆生态系统使製造商能够将免手驾驶功能从受控的高速公路环境扩展到复杂的城市环境。人工智慧感知系统、高精度数位地图和空中软体更新为这一进展提供了支持,从而能够持续改进功能、安全性和驾驶性能。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 对免持和便捷出行方式的需求日益增长

- 人工智慧、感测器融合和车载运算领域的进展

- OEM向软体定义汽车(SDV)转型

- 都市化加速与交通运输日益复杂化

- 监理支援监督式自动驾驶和ADAS演进

- 产业潜在风险与挑战

- 高成本和硬体复杂性

- 各区域监管体系碎片化

- 市场机会

- 拓展至中檔及大众市场汽车领域

- 订阅模式和按需功能模式

- 与电动车和智慧运输系统的融合

- 亚太地区都市区自动驾驶技术的发展

- 与人工智慧、地图绘製和云端服务供应商建立策略伙伴关係

- 促进因素

- 成长潜力分析

- 北美洲

- 美国:NHTSA自动驾驶系统(ADS)指南和自动驾驶汽车测试倡议

- 欧洲

- 欧盟:联合国欧洲经济委员会第R157号条例(自动车道维持系统 - ALKS)

- 德国:自动驾驶法

- 英国:互联自动驾驶(CAM)法规

- 法国:自动驾驶车辆测试框架

- 亚太地区

- 中国:智慧网联汽车(ICV)模拟标准

- 日本:国土交通省自动驾驶安全指南

- 韩国:自动驾驶汽车法

- 新加坡:自动驾驶车辆安全评估框架

- 拉丁美洲

- 巴西:国家智慧交通与物联网策略

- 墨西哥:智慧运输和自动驾驶汽车试点法规

- 智利:智慧型运输系统(ITS)政策

- 中东和非洲(MEA)

- 阿联酋:杜拜的自动驾驶交通战略

- 沙乌地阿拉伯:2030愿景智慧运输框架

- 南非:绿色交通与自动驾驶政策

- 北美洲

- 波特的分析

- PESTEL 分析

- 技术与创新展望

- 当前技术趋势

- 新兴技术

- 专利分析

- 永续性和环境影响分析

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

- 未来前景与机会

- 人机互动(HMI)与驾驶员监控系统(DMS)

- 自主系统的人机介面设计原则

- 驾驶员监控系统(DMS)技术

- DMS的监管要求

- 使用者体验 (UX) 挑战与解决方案

- 主要人机介面/桌面管理系统技术供应商

- 数据策略与软体堆迭经济学

- 资料撷取与管理架构

- 软体堆迭架构

- 软体开发经济学

- 数据商业化战略

- 仿真和检验基础设施

第四章 竞争情势

- 介绍

- 企业市占率分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估价与预测:依自动驾驶等级划分,2022-2035年

- 二级高级驾驶辅助系统

- 3级ADAS

第六章 市场估计与预测:依投资设计领域划分,2022-2035年

- 限高速公路系统

- 城市和道路相关係统

- 全面/到府服务系统

第七章 市场估计与预测:依感测器技术划分,2022-2035年

- 基于摄影机的系统

- 基于雷达的系统

- 配备光达的系统

- 多感测器融合系统

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 仅供个人/私人使用

- 叫车和共享出行

- 商用车辆车队

第九章 市场估价与预测:依车辆类型划分,2022-2035年

- 搭乘用车

- 轿车

- 掀背车

- SUV

- 商用车辆

- 轻型商用车(LCV)

- MCV

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 比利时

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 菲律宾

- 印尼

- 新加坡

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章:公司简介

- 世界公司

- BMW

- Continental

- DENSO

- General Motors(GM)

- Mercedes-Benz

- Mobileye

- Nissan Motor

- NVIDIA

- Robert Bosch

- Stellantis

- Tesla

- Toyota Motor

- 按地区分類的主要企业

- Baidu

- Honda Motor

- Huawei Technologies

- Hyundai Motor

- NIO

- Renesas Electronics

- StradVision

- Valeo

- Ghost Autonomy

- 新兴企业

- Ambarella

- Aptiv

- Innoviz Technologies

- Luminar Technologies

- Magna International

- NXP Semiconductors

- Qualcomm Technologies

- Sony Semiconductor Solutions

- ZF Friedrichshafen

The Global Ultra Cruise & City-Street Autonomous Driving Market was valued at USD 31.48 billion in 2025 and is estimated to grow at a CAGR of 16.8% to reach USD 169.65 billion by 2035.

The integration of advanced hands-free driving and city-level automation is reshaping vehicle design, embedded software frameworks, and next-generation mobility solutions. Automakers are moving away from isolated driver-assistance features toward adaptive, software-defined driving platforms that support progressively higher autonomy while retaining human supervision. Urban driving conditions, including congestion, unpredictable road users, and inconsistent infrastructure, are placing higher performance demands on city-street autonomous systems. These solutions rely on sophisticated sensor integration, continuous environment perception, and high-speed computing to manage intersections, traffic signals, lane changes, and complex traffic flows. Because vehicles operate within defined operational design domains, such technologies are essential for extending autonomy beyond limited-access roads into everyday urban use. Automakers and technology providers are heavily investing in scalable autonomy stacks that emphasize safety, reliability, and gradual feature expansion through software updates rather than full automation deployment. This step-by-step approach supports regulatory alignment, consumer trust, and faster commercialization.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $31.48 Billion |

| Forecast Value | $169.65 Billion |

| CAGR | 16.8% |

The Level 2 ADAS segment held a 65% share in 2025 and is projected to grow at a CAGR of 16.5% through 2035. This segment leads due to its ability to deliver advanced automated functionality while maintaining driver oversight, making regulatory approval and market rollout more practical across regions. Existing safety standards, liability frameworks, and certification processes strongly favor supervised autonomy, enabling faster adoption compared to higher autonomy levels.

The city-street capable systems segment held 48% share in 2025 and is expected to register a CAGR of 17.8% between 2026 and 2035. These systems dominate because they address everyday driving environments where most vehicle usage occurs. Urban operation involves frequent stops, intersections, vulnerable road users, and mixed traffic conditions, making city-focused automation more valuable than highway-only solutions. Growing consumer demand for stress reduction in urban commuting, parking, and short-distance travel continues to accelerate adoption.

United States Ultra Cruise & City-Street Autonomous Driving Market held an 85% share, generating USD 9.2 billion in 2025. Market expansion in the U.S. remains strong, driven by continuous innovation in advanced driver assistance and supervised autonomy solutions, along with substantial investment from major automakers. A well-developed software-defined vehicle ecosystem is enabling manufacturers to extend hands-free driving capabilities beyond controlled highway environments into complex urban settings. This progress is supported by artificial intelligence-based perception systems, high-precision digital mapping, and over-the-air software updates that allow ongoing improvements in functionality, safety, and driving performance.

Key participants active in the Global Ultra Cruise & City-Street Autonomous Driving Market include NVIDIA, Toyota Motor, Continental, Mobileye, General Motors, Stellantis, BMW, Nissan Motor, and Mercedes-Benz Group. Companies in the ultra cruise and city-street autonomous driving market are strengthening their foothold through sustained investment in software-centric vehicle architectures and artificial intelligence-driven perception systems. Automakers are prioritizing modular autonomy platforms that allow features to scale across vehicle models and price segments. Strategic partnerships with semiconductor firms and software developers help accelerate processing performance and algorithm refinement. Many players emphasize over-the-air update capabilities to enhance system reliability and functionality post-sale. Extensive real-world data collection is used to improve urban driving accuracy and safety validation.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Autonomy Level

- 2.2.3 Operational Design Domain

- 2.2.4 Vehicle

- 2.2.5 Sensor Technology

- 2.2.6 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Demand for Hands-Free & Convenience-Driven Mobility

- 3.2.1.2 Advancements in AI, Sensor Fusion & Onboard Compute

- 3.2.1.3 OEM Shift Toward Software-Defined Vehicles (SDVs)

- 3.2.1.4 Expanding Urbanization & Traffic Complexity

- 3.2.1.5 Regulatory Support for Supervised Autonomy & ADAS Evolution

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High System Cost & Hardware Complexity

- 3.2.2.2 Regulatory Fragmentation Across Regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into Mid-Range & Mass-Market Vehicles

- 3.2.3.2 Subscription-Based & Feature-on-Demand Models

- 3.2.3.3 Integration with EV & Smart Mobility Ecosystems

- 3.2.3.4 Asia-Pacific Urban Autonomy Growth

- 3.2.3.5 Strategic Partnerships with AI, Mapping & Cloud Providers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.3.1 North America

- 3.3.1.1 United States: NHTSA Automated Driving Systems (ADS) Guidance & AV TEST Initiative

- 3.3.2 Europe

- 3.3.2.1 European Union: UNECE Regulation R157 (Automated Lane Keeping Systems - ALKS)

- 3.3.2.2 Germany: Autonomous Driving Act

- 3.3.2.3 United Kingdom: Connected and Automated Mobility (CAM) Regulations

- 3.3.2.4 France: Autonomous Vehicle Experimentation Framework

- 3.3.3 Asia Pacific

- 3.3.3.1 China: Intelligent Connected Vehicle (ICV) Simulation Standards

- 3.3.3.2 Japan: MLIT Automated Driving Safety Guidelines

- 3.3.3.3 South Korea: Autonomous Vehicle Act

- 3.3.3.4 Singapore: Autonomous Vehicle Safety Assessment Framework

- 3.3.4 Latin America

- 3.3.4.1 Brazil: National Intelligent Mobility & IoT Strategy

- 3.3.4.2 Mexico: Smart Mobility & Autonomous Vehicle Pilot Regulations

- 3.3.4.3 Chile: Intelligent Transport Systems (ITS) Policy

- 3.3.5 Middle East & Africa (MEA)

- 3.3.5.1 United Arab Emirates: Dubai Autonomous Transport Strategy

- 3.3.5.2 Saudi Arabia: Vision 2030 Smart Mobility Framework

- 3.3.5.3 South Africa: Green Transport & Automated Mobility Policy

- 3.3.1 North America

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Sustainability and environmental impact analysis

- 3.8.1 Sustainable practices

- 3.8.2 Waste reduction strategies

- 3.8.3 Energy efficiency in production

- 3.8.4 Eco-friendly initiatives

- 3.8.5 Carbon footprint considerations

- 3.9 Future outlook & opportunities

- 3.10 Human-machine interaction (HMI) & driver monitoring systems (DMS)

- 3.10.1 HMI design principles for autonomous systems

- 3.10.2 Driver monitoring system (DMS) technologies

- 3.10.3 Regulatory requirements for dms

- 3.10.4 User experience (Ux) challenges & solutions

- 3.10.5 Leading HMI/DMS technology providers

- 3.11 Data strategy & software stack economics

- 3.11.1 Data collection & management architecture

- 3.11.2 Software stack architecture

- 3.11.3 Software development economics

- 3.11.4 Data monetization strategies

- 3.11.5 Simulation & validation infrastructure

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Autonomy Level, 2022 - 2035 ($Bn, units)

- 5.1 Key trends

- 5.2 Level 2 ADAS

- 5.3 Level 3 ADAS

Chapter 6 Market Estimates & Forecast, By Operational Design Domain, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Highway-Only Systems

- 6.3 City-Street Capable Systems

- 6.4 Comprehensive / Door-to-Door Systems

Chapter 7 Market Estimates & Forecast, By Sensor Technology, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Camera-Based Systems

- 7.3 Radar-Based Systems

- 7.4 LiDAR-Enabled Systems

- 7.5 Multi-Sensor Fusion Systems

Chapter 8 Market Estimates & Forecast, By End-Use, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Private / Personal Use

- 8.3 Ride-Hailing & Shared Mobility

- 8.4 Commercial Fleets

Chapter 9 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Passenger vehicle

- 9.2.1 Sedan

- 9.2.2 Hatchback

- 9.2.3 SUV

- 9.3 Commercial vehicle

- 9.3.1 LCV

- 9.3.2 MCV

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Belgium

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.4.8 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BMW

- 11.1.2 Continental

- 11.1.3 DENSO

- 11.1.4 General Motors (GM)

- 11.1.5 Mercedes-Benz

- 11.1.6 Mobileye

- 11.1.7 Nissan Motor

- 11.1.8 NVIDIA

- 11.1.9 Robert Bosch

- 11.1.10 Stellantis

- 11.1.11 Tesla

- 11.1.12 Toyota Motor

- 11.2 Regional Players

- 11.2.1 Baidu

- 11.2.2 Honda Motor

- 11.2.3 Huawei Technologies

- 11.2.4 Hyundai Motor

- 11.2.5 NIO

- 11.2.6 Renesas Electronics

- 11.2.7 StradVision

- 11.2.8 Valeo

- 11.2.9 Ghost Autonomy

- 11.3 Emerging Players

- 11.3.1 Ambarella

- 11.3.2 Aptiv

- 11.3.3 Innoviz Technologies

- 11.3.4 Luminar Technologies

- 11.3.5 Magna International

- 11.3.6 NXP Semiconductors

- 11.3.7 Qualcomm Technologies

- 11.3.8 Sony Semiconductor Solutions

- 11.3.9 ZF Friedrichshafen

2034年全球自动驾驶物流车辆市场预测-按车辆类型、组件、导航技术、自动驾驶等级、应用、最终用户和地区分類的全球分析2034年自主港口营运市场预测:按自动化程度、设备类型、技术、应用、最终用户和地区分類的全球分析

2034年全球自动驾驶物流车辆市场预测-按车辆类型、组件、导航技术、自动驾驶等级、应用、最终用户和地区分類的全球分析2034年自主港口营运市场预测:按自动化程度、设备类型、技术、应用、最终用户和地区分類的全球分析 自动驾驶汽车市场:按组件、自动驾驶等级、燃料类型、技术、应用、车辆类型和最终用户划分-2026-2032年全球市场预测

自动驾驶汽车市场:按组件、自动驾驶等级、燃料类型、技术、应用、车辆类型和最终用户划分-2026-2032年全球市场预测 2026年全球机器人车辆市场报告自动驾驶汽车处理器市场:按处理器类型、车辆类型、销售管道和应用划分-2026-2032年全球市场预测

2026年全球机器人车辆市场报告自动驾驶汽车处理器市场:按处理器类型、车辆类型、销售管道和应用划分-2026-2032年全球市场预测 全球自动驾驶汽车市场规模、份额、趋势和成长分析报告(2026-2034)全球自动驾驶汽车市场规模、份额、趋势和成长分析报告(2026-2034)

全球自动驾驶汽车市场规模、份额、趋势和成长分析报告(2026-2034)全球自动驾驶汽车市场规模、份额、趋势和成长分析报告(2026-2034) 2026-2030年全球L4级自动驾驶汽车市场按自主等级、推进方式、负载容量、车辆类型、应用和最终用户产业分類的全球自主物流车辆市场预测(2026-2032年)按营运模式、车辆类型、自动驾驶等级、所有权模式和应用程式分類的按需自动驾驶出行市场,全球预测,2026-2032年

2026-2030年全球L4级自动驾驶汽车市场按自主等级、推进方式、负载容量、车辆类型、应用和最终用户产业分類的全球自主物流车辆市场预测(2026-2032年)按营运模式、车辆类型、自动驾驶等级、所有权模式和应用程式分類的按需自动驾驶出行市场,全球预测,2026-2032年