|

市场调查报告书

商品编码

1959335

移动式汽车破碎拖车市场:机会、成长要素、产业趋势分析及2026年至2035年预测Mobile Car Crusher Trailer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

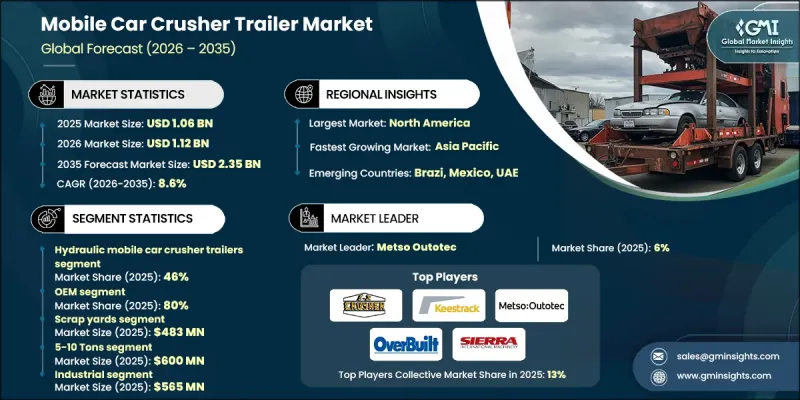

2025年全球移动式汽车破碎拖车市场价值为10.6亿美元,预计2035年将达23.5亿美元,年复合成长率为8.6%。

随着全球汽车废弃物数量的成长,在对更快、更有效率的回收流程日益增长的需求推动下,市场持续保持成长动能。更严格的环境政策和报废车辆(ELV)法规合规要求促使回收商对其破碎设备进行现代化改造。废品回收场、汽车拆解厂和工业回收设施越来越注重提高生产效率、减少排放气体和履行安全义务,加速了对先进移动式破碎拖车的需求。现场破碎的普及也降低了运输成本和工期延误。拥有多个回收点的大型回收设施和废品营运商正积极投资移动式、高容量和模组化破碎拖车,以保持营运的柔软性和便利性。能够处理各种车辆类型并在各种运作环境下提供稳定性能的液压、电力和柴油系统的日益普及,进一步推动了市场成长。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 10.6亿美元 |

| 预测金额 | 23.5亿美元 |

| 复合年增长率 | 8.6% |

持续的技术创新正透过智慧製程控制、数位化性能监控、自动化安全机制和先进的动力系统,重塑移动式电动破碎拖车的运作方式。这些改进提高了破碎精度、处理能力和物料回收率,同时确保符合环境和职场标准。模组化拖车结构和预测性维护工具的整合延长了设备使用寿命并减少了停机时间。节能的电动和混合动力破碎系统也有助于降低操作人员对燃料的依赖和排放,从而提高营运效率并实现长期成本节约,同时符合不断发展的永续性目标。

预计到2025年,液压式移动汽车破碎拖车将占据约46%的市场份额,并在2026年至2035年间以超过8.4%的复合年增长率增长。该细分市场之所以能够保持主导地位,是因为它能够以最小的人工干预实现可控的高强度破碎。操作人员之所以青睐液压系统,是因为其可靠性高、能够适应各种尺寸的车辆,并且安全性能更佳,尤其是在大批量废料处理环境和多站点管理运营中。

预计到2025年,OEM(原始设备製造商)市占率将达到80%,并在2035年之前以8.8%的复合年增长率成长。 OEM的领先地位得益于其能够直接获得设计完整、经过认证的破碎机拖车,这些拖车具有耐用性、客製化选项和整合合规功能等优势。终端用户更倾向于选择OEM解决方案,因为其提供保固服务、技术支持,并且能够满足严格的营运和监管标准,这使其成为大型回收网路中的首选采购方案。

预计2025年,美国移动式汽车破碎拖车市场规模将达3.146亿美元,市占率高达83%。该地区受益于完善的汽车回收基础设施和先进移动破碎技术的广泛应用。持续增加对自动化、数位监控和高容量拖车解决方案的投资,使北美在高效、技术主导的汽车回收领域处于领先地位。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 汽车报废和回收需求日益增长

- 技术进步

- 环境与监理合规

- 工业废弃物处理厂及废料堆场扩建

- 产业潜在风险与挑战

- 较高的初始投资和维护成本

- 市场分散且标准化程度低

- 市场机会

- 对现场和携带式回收设备的需求增加

- 新兴市场和未开发地区

- 电动和混合动力破碎机拖车

- 专注永续性和循环经济

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国:EPA、OSHA 和 RCRA 合规指南

- 加拿大税务局 (CRA) 和加拿大环境与气候变迁部的指导方针。

- 欧洲

- 德国:联邦环境部和报废车辆法规

- 法国:生态系统转型部和报废车辆指南

- 英国:环境署和废弃物管理条例

- 义大利:环境部和报废车辆合规性

- 亚太地区

- 中国:生态环境部标准

- 日本:经济产业省及废弃电子电气设备回收法

- 韩国:环境部及报废车辆法规

- 印度:环境、森林及气候变迁部及汽车报废政策

- 拉丁美洲

- 巴西:国家环境委员会 (CONAMA) 和回收标准

- 墨西哥:环境部(SEMARNAT)指南

- 中东和非洲

- 阿拉伯联合大公国:环境署 - 阿布达比和联邦标准

- 沙乌地阿拉伯:沙乌地阿拉伯标准、计量和品质研究院

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

- 使用案例场景

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估算与预测:依电源类型划分,2022-2035年

- 液压移动式车辆破碎拖车

- 柴油动力移动式车辆破碎拖车

- 电动移动式汽车粉碎拖车

- 其他的

第六章 市场估计与预测:依产能划分,2022-2035年

- 5-10吨

- 5吨或以下

- 超过10吨

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 废品场

- 汽车回收

- 建设与拆除

- 紧急应变

- 军事用途

- 其他的

第八章 市场估算与预测:依最终用途划分,2022-2035年

- 工业的

- 商业的

- 对于地方政府

- 其他的

第九章 市场估价与预测:依通路划分,2022-2035年

- OEM

- 售后市场

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 阿拉伯聯合大公国

- 南非

- 沙乌地阿拉伯

第十一章:公司简介

- Global Player

- Al-jon Manufacturing

- Eagle Crusher Company

- EZ Crusher

- Hammel Recyclingtechnik

- Keestrack

- McCloskey International

- Metso Outotec

- OverBuilt

- Sandvik

- Sierra International Machinery

- Regional Player

- BENLEE

- Big Mac

- Enerpat

- Gensco Equipment

- Granutech-Saturn Systems

- RM Johnson Company

- SAS of Luxemburg

- The Auto Crusher

- VYKIN Crushers

- Youngs Auto Center &Salvage

- 新兴企业

- Baichy Heavy Industrial Machinery

- Fabo Company

- Guangxi Mesda Engineering Machinery

- SBM Mineral Processing

- Senya Crushers

The Global Mobile Car Crusher Trailer Market was valued at USD 1.06 billion in 2025 and is estimated to grow at a CAGR of 8.6% to reach USD 2.35 billion by 2035.

The market continues to gain momentum as rising vehicle retirement rates worldwide increase the need for faster and more efficient recycling processes. Tighter environmental policies and End-of-Life Vehicle compliance requirements are pushing recycling operators to modernize their crushing infrastructure. Scrap yards, vehicle dismantlers, and industrial recycling facilities are increasingly focused on improving productivity, lowering emissions, and meeting safety obligations, which is accelerating demand for advanced mobile crusher trailers. The growing shift toward on-site crushing is also reducing transportation costs and operational delays. Large-scale recycling facilities and multi-site scrap operators are actively investing in mobile, high-capacity, and modular crusher trailers to maintain flexibility and operational control. Market growth is further supported by increasing adoption of hydraulic, electric, and diesel-powered systems designed to handle diverse vehicle types while delivering consistent performance across varied operating environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.06 Billion |

| Forecast Value | $2.35 Billion |

| CAGR | 8.6% |

Ongoing innovation is reshaping mobile car crusher trailer operations through intelligent process controls, digitally enabled performance monitoring, automated safety mechanisms, and advanced power systems. These improvements enhance crushing accuracy, increase throughput, and improve material recovery while ensuring compliance with environmental and workplace standards. The integration of modular trailer structures and predictive maintenance tools is extending equipment lifespan and reducing downtime. Energy-efficient electric and hybrid crusher systems are also helping operators reduce fuel dependency and emissions, allowing them to achieve higher operational efficiency and lower long-term costs while aligning with evolving sustainability targets.

Hydraulic mobile car crusher trailers accounted for roughly 46% of the total market share in 2025 and are projected to grow at a CAGR exceeding 8.4% from 2026 to 2035. This segment continues to lead due to its ability to deliver controlled, high-force crushing with minimal manual handling. Operators favor hydraulic systems for their reliability, adaptability to different vehicle sizes, and enhanced safety performance, particularly in high-volume scrappage environments and operations managing multiple sites.

The OEM segment held 80% share in 2025 and is forecast to grow at a CAGR of 8.8% through 2035. OEM dominance is driven by direct access to fully engineered and certified crusher trailers that offer durability, customization options, and integrated compliance features. End users prioritize OEM solutions for their warranty coverage, technical support, and ability to meet strict operational and regulatory standards, making them the preferred procurement choice across large recycling networks.

United States Mobile Car Crusher Trailer Market held 83% share and reached USD 314.6 million in 2025. The region benefits from a well-established vehicle recycling infrastructure and widespread deployment of advanced mobile crushing technologies. Strong investment in automation, digital monitoring, and high-capacity trailer solutions continues to position North America at the forefront of efficient and technology-driven vehicle recycling.

Key companies active in the Global Mobile Car Crusher Trailer Market include Metso Outotec, Sandvik, Al jon Manufacturing, Sierra International Machinery, Eagle Crusher Company, McCloskey International, OverBuilt, EZ Crusher, Hammel Recyclingtechnik, and Keestrack. Companies operating in the mobile car crusher trailer market are strengthening their market position through continuous product innovation, strategic equipment upgrades, and expanded service offerings. Manufacturers are focusing on developing higher-capacity trailers with improved energy efficiency and advanced control systems to meet evolving customer demands. Many players are investing in modular designs and smart monitoring technologies to enhance flexibility and reduce maintenance costs. Strategic partnerships with recycling operators and regional distributors are helping companies expand their geographic reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Power Source

- 2.2.3 Capacity

- 2.2.4 Application

- 2.2.5 End Use

- 2.2.6 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Vehicle Scrappage & Recycling Needs

- 3.2.1.2 Technological Advancements

- 3.2.1.3 Environmental & Regulatory Compliance

- 3.2.1.4 Expansion of Industrial & Scrap Yard Operations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Investment & Maintenance Costs

- 3.2.2.2 Fragmented Market & Limited Standardization

- 3.2.3 Market opportunities

- 3.2.3.1 Rising Demand for On-Site and Portable Recycling

- 3.2.3.2 Emerging Markets & Untapped Regions

- 3.2.3.3 Electric & Hybrid Crusher Trailers

- 3.2.3.4 Sustainability and Circular Economy Focus

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA, OSHA, and RCRA Compliance Guidelines

- 3.4.1.2 Canada Revenue Agency (CRA) & Environment and Climate Change Canada Guidelines

- 3.4.2 Europe

- 3.4.2.1 Germany: Federal Ministry for the Environment & ELV Regulations

- 3.4.2.2 France: Ministry of Ecological Transition & ELV Guidelines

- 3.4.2.3 UK: Environment Agency & Waste Regulations

- 3.4.2.4 Italy: Ministry of Environment & ELV Compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Ministry of Ecology and Environment Standards

- 3.4.3.2 Japan: Ministry of Economy, Trade and Industry & ELV Recycling Law

- 3.4.3.3 South Korea: Ministry of Environment & ELV Regulations

- 3.4.3.4 India: Ministry of Environment, Forest and Climate Change & Vehicle Scrappage Policy

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Environment Council (CONAMA) & Recycling Standards

- 3.4.4.2 Mexico: SEMARNAT Guidelines

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: Environment Agency - Abu Dhabi & Federal Standards

- 3.4.5.2 Saudi Arabia: Saudi Standards, Metrology and Quality Organization

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Power Source, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hydraulic Mobile Car Crusher Trailers

- 5.3 Diesel-Powered Mobile Car Crusher Trailers

- 5.4 Electric Mobile Car Crusher Trailers

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Capacity, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 5-10 Tons

- 6.3 Up to 5 Tons

- 6.4 Above 10 Tons

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Scrap Yards

- 7.3 Automotive Recycling

- 7.4 Construction & Demolition

- 7.5 Emergency Response

- 7.6 Military

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Industrial

- 8.3 Commercial

- 8.4 Municipal

- 8.5 Other

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 Al-jon Manufacturing

- 11.1.2 Eagle Crusher Company

- 11.1.3 EZ Crusher

- 11.1.4 Hammel Recyclingtechnik

- 11.1.5 Keestrack

- 11.1.6 McCloskey International

- 11.1.7 Metso Outotec

- 11.1.8 OverBuilt

- 11.1.9 Sandvik

- 11.1.10 Sierra International Machinery

- 11.2 Regional Player

- 11.2.1 BENLEE

- 11.2.2 Big Mac

- 11.2.3 Enerpat

- 11.2.4 Gensco Equipment

- 11.2.5 Granutech-Saturn Systems

- 11.2.6 RM Johnson Company

- 11.2.7 SAS of Luxemburg

- 11.2.8 The Auto Crusher

- 11.2.9 VYKIN Crushers

- 11.2.10 Youngs Auto Center & Salvage

- 11.3 Emerging Players

- 11.3.1 Baichy Heavy Industrial Machinery

- 11.3.2 Fabo Company

- 11.3.3 Guangxi Mesda Engineering Machinery

- 11.3.4 SBM Mineral Processing

- 11.3.5 Senya Crushers

半移动式破碎站市场:按破碎机类型、动力来源、应用和终端用户产业划分-全球预测,2026-2032年

半移动式破碎站市场:按破碎机类型、动力来源、应用和终端用户产业划分-全球预测,2026-2032年 全球移动式破碎筛分机市场规模、份额、趋势及成长分析报告(2026-2034年)

全球移动式破碎筛分机市场规模、份额、趋势及成长分析报告(2026-2034年) 2026年全球移动式破碎筛分机市场报告

2026年全球移动式破碎筛分机市场报告 行动破碎分选市场-全球产业规模、份额、趋势、机会与预测:按类型、机械类型、最终用户产业、地区和竞争格局划分,2021-2031年

行动破碎分选市场-全球产业规模、份额、趋势、机会与预测:按类型、机械类型、最终用户产业、地区和竞争格局划分,2021-2031年 移动式破碎筛分机市场规模、份额及成长分析(依产品类型、应用、最终用户及地区划分)-2026-2033年产业预测

移动式破碎筛分机市场规模、份额及成长分析(依产品类型、应用、最终用户及地区划分)-2026-2033年产业预测 北美行动式破碎分类机市场:市场规模、份额、趋势分析(按类型、应用和国家划分)、细分市场预测(2025-2033 年)

北美行动式破碎分类机市场:市场规模、份额、趋势分析(按类型、应用和国家划分)、细分市场预测(2025-2033 年) 2025 年至 2033 年行动破碎筛分机市场报告,依产品类型(移动式破碎机、行动筛分机)、设备用途(新设备、二手设备)、最终用户(采石场、建筑、采矿、材料回收等)和地区划分行动碎纸机和筛选机市场规模、份额和趋势分析报告:按类型、按应用、按地区、细分市场预测,2025-2030 年

2025 年至 2033 年行动破碎筛分机市场报告,依产品类型(移动式破碎机、行动筛分机)、设备用途(新设备、二手设备)、最终用户(采石场、建筑、采矿、材料回收等)和地区划分行动碎纸机和筛选机市场规模、份额和趋势分析报告:按类型、按应用、按地区、细分市场预测,2025-2030 年 日本的移动式碾碎机及筛分机市场评估:类型·终端用户产业·行动类型·各地区的机会及预测 (2018-2032年)美国移动式破碎机和筛分机市场评估:依类型、最终用户产业、移动类型、地区、机会、预测,2017-2031年

日本的移动式碾碎机及筛分机市场评估:类型·终端用户产业·行动类型·各地区的机会及预测 (2018-2032年)美国移动式破碎机和筛分机市场评估:依类型、最终用户产业、移动类型、地区、机会、预测,2017-2031年