|

市场调查报告书

商品编码

1959544

整合系统市场机会、成长要素、产业趋势分析及2026年至2035年预测Integrated Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025年全球整合系统市场价值为423亿美元,预计2035年将以15.1%的复合年增长率成长至1,718亿美元。

市场成长的驱动力在于各产业加速采用整合解决方案,旨在实现营运现代化、自动化复杂工作流程,并在全球系统间实现互通性。企业越来越依赖整合系统来支援大规模转型计划,并利用这些解决方案将分散的营运结构整合到统一的环境中。透过将IT基础设施、操作技术和资料平台连接到单一的整合框架中,企业可以提高生产力、减少流程低效,并快速获得可执行的洞察。整合系统减少了对人工流程的依赖,提供跨职能的即时可视性,并支援更明智、更及时的决策。人工智慧驱动的自动化技术的日益普及进一步放大了市场需求,因为企业可以利用智慧系统来提高预测准确性、预测性维护和营运精度。随着企业管理大量资料和日益复杂的环境,整合系统在提升製造、服务和企业营运的反应速度、扩充性和整体业务敏捷性方面发挥着至关重要的作用。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 423亿美元 |

| 预测金额 | 1718亿美元 |

| 复合年增长率 | 15.1% |

预计到2025年,整合平台和工作负载系统细分市场将占据41.4%的市场。该细分市场正引领市场普及,因为企业更倾向于采用将运算、储存和网路功能整合于单一架构中的统一平台。这些系统简化了编配,提高了效能一致性,实现了即时处理,并降低了基础架构的复杂性。企业正越来越多地采用这些平台来简化IT运维,同时支援各行各业的高阶分析和数位转型计画。

预计到2025年,本地部署市场规模将达到181亿美元,并持续保持主导地位。企业持续优先考虑本地整合系统,因为它们能够提供更高的控制力、资料安全性和可自订性。这些解决方案对管理敏感资料和关键业务营运的组织极具吸引力,因为它们支援合规性、可预测的效能和客製化的基础设施设计。

美国整合系统市场预计2025年将达到107亿美元。主导地位得益于对先进IT基础设施的持续投资、对云端和本地部署解决方案的强劲需求,以及各行业广泛的数位转型措施。持续的技术创新和领先解决方案供应商的存在进一步巩固了美国的优势。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 跨产业数位转型措施的增加

- 自动化、人工智慧和数据分析应用范围的扩大

- 云端运算和混合IT环境的兴起

- 对即时数据整合和可视化的需求日益增长

- 人们越来越关注营运效率和成本优化

- 产业潜在风险与挑战

- 实施和整合的初期成本很高。

- 整合旧有系统的复杂性

- 市场机会

- 物联网和连接基础设施的扩展

- 智慧製造和工业4.0应用的成长

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 历史价格分析(2022-2024)

- 影响价格趋势的因素

- 区域价格差异

- 价格预测(2026-2035)

- 定价策略

- 新兴经营模式

- 合规要求

- 专利分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 地理位置比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 2022-2025 年重大发展

- 併购

- 合作伙伴关係和合资企业

- 技术进步

- 扩张和投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章:整合系统市场估算与预测:依产品划分,2022-2035年

- ,

- 整合平台/工作负载系统

- 综合基础设施系统

- 其他整合系统

第六章 市场估计与预测:依服务业划分,2022-2035年

- 整合和安装

- 咨询

- 维护和支援

- 训练

第七章:整合系统市场估算与预测:依部署模式划分,2022-2035年

- 现场

- 基于云端的

- 杂交种

第八章:整合系统市场估算与预测:依应用领域划分,2022-2035年

- 车

- 航太和国防部门

- 资讯科技和通讯

- BFSI

- 卫生保健

- 石油和天然气

- 活力

- 製造业

- 零售

- 其他的

第九章:整合系统市场估算与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 荷兰

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十章:公司简介

- Accenture

- IBM Corporation

- Tata Consultancy Services Limited

- Oracle Corporation

- BAE Systems

- Wipro Limited

- Cognizant

- Deloitte Touche Tohmatsu Limited

- Infosys Limited

- MDS Systems Integration(MDS SI)

- HCL Technologies

- Capgemini

- Atos SE

- Fujitsu Limited

- Cisco Systems, Inc.

- Hewlett Packard Enterprise(HPE)

- SAP SE

- NEC Corporation

- Siemens AG

- CGI Inc.

- DXC Technology

- Tech Mahindra

- Hitachi, Ltd.(Vantara)

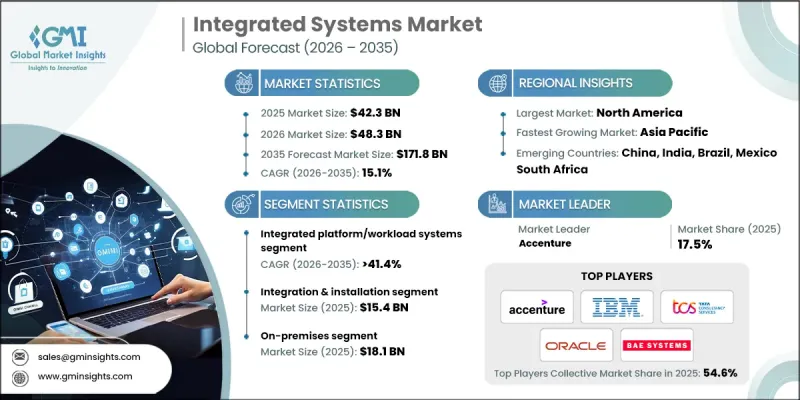

The Global Integrated Systems Market was valued at USD 42.3 billion in 2025 and is estimated to grow at a CAGR of 15.1% to reach USD 171.8 billion by 2035.

Market growth is fueled by the accelerating adoption of integrated solutions across industries seeking to modernize operations, automate complex workflows, and enable seamless interoperability between global systems. Organizations increasingly rely on integrated systems to support large-scale digital transformation initiatives, as these solutions help consolidate fragmented operational structures into unified environments. By connecting IT infrastructure, operational technologies, and data platforms into a single cohesive framework, enterprises improve productivity, reduce process inefficiencies, and gain faster access to actionable insights. Integrated systems reduce reliance on manual processes, enable real-time visibility across departments, and support more informed and timely decision-making. The rising use of AI-driven automation further amplifies demand, as organizations leverage intelligent systems to improve forecasting, predictive maintenance, and operational precision. As enterprises manage growing data volumes and increasingly complex environments, integrated systems play a critical role in enhancing responsiveness, scalability, and overall business agility across manufacturing, services, and enterprise operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $42.3 Billion |

| Forecast Value | $171.8 Billion |

| CAGR | 15.1% |

The integrated platform and workload systems segment accounted for a 41.4% share in 2025. This segment leads adoption as organizations favor unified platforms that combine compute, storage, and networking capabilities within a single architecture. These systems simplify workload orchestration, enhance performance consistency, enable real-time processing, and reduce infrastructure complexity. Enterprises increasingly adopt these platforms to streamline IT operations while supporting advanced analytics and digital transformation initiatives across diverse industries.

The on-premises segment generated USD 18.1 billion in 2025 and remained the dominant deployment model. Enterprises continue to prioritize on-premises integrated systems due to their ability to deliver higher levels of control, data security, and customization. These solutions support regulatory compliance, predictable performance, and tailored infrastructure design, making them highly attractive for organizations managing sensitive data and mission-critical operations.

U.S. Integrated Systems Market reached USD 10.7 billion in 2025. Market leadership is supported by sustained investments in advanced IT infrastructure, strong demand for both cloud-based and on-premises solutions, and widespread digital transformation initiatives across sectors. Continuous technological innovation and the presence of major solution providers further reinforce the country's dominant position.

Key companies operating in the Global Integrated Systems Market include IBM Corporation, Accenture, Oracle Corporation, Tata Consultancy Services Limited, Cisco Systems Inc., Hewlett Packard Enterprise, SAP SE, Siemens AG, Fujitsu Limited, Capgemini, Wipro Limited, Infosys Limited, Cognizant, Deloitte Touche Tohmatsu Limited, HCL Technologies, Atos SE, DXC Technology, CGI Inc., Tech Mahindra, NEC Corporation, BAE Systems, Hitachi Ltd. through Vantara, and MDS Systems Integration. Companies in the Integrated Systems Market strengthen their market position through continuous innovation, strategic partnerships, and expansion of end-to-end solution portfolios. Leading players invest heavily in AI-enabled automation, hybrid deployment models, and scalable architectures to address evolving enterprise requirements. Firms focus on industry-specific integrated solutions to meet regulatory, security, and performance needs. Mergers, acquisitions, and collaborations help expand geographic reach and technical expertise.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Service trends

- 2.2.3 Deployment Model trends

- 2.2.4 End-Use trends

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in digital transformation initiatives across industries

- 3.2.1.2 Growing adoption of automation, AI, and data analytics

- 3.2.1.3 Increase in cloud computing and hybrid IT environments

- 3.2.1.4 Rising demand for real-time data integration and visibility

- 3.2.1.5 Growing focus on operational efficiency and cost optimization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial implementation and integration costs

- 3.2.2.2 Complexity of integrating legacy systems

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of IoT and connected infrastructure

- 3.2.3.2 Growth in smart manufacturing and Industry 4.0 adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2022-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2026-2035)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Integrated systems Market Estimates & Forecast, By Product, 2022 - 2035 (USD Billion)

- 5.1 Key trends,

- 5.2 Integrated Platform/Workload Systems

- 5.3 Integrated Infrastructure Systems

- 5.4 Other Integrated Systems

Chapter 6 Market Estimates and Forecast, By Service, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Integration & Installation

- 6.3 Consulting

- 6.4 Maintenance & Support

- 6.5 Training

Chapter 7 Integrated systems Market Estimates & Forecast, By Deployment Model, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 On-premises

- 7.3 Cloud-based

- 7.4 Hybrid

Chapter 8 Integrated systems Market Estimates & Forecast, By End-Use, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Aerospace and Defense

- 8.4 IT and Telecom

- 8.5 BFSI

- 8.6 Healthcare

- 8.7 Oil and Gas

- 8.8 Energy

- 8.9 Manufacturing

- 8.10 Retail

- 8.11 Others

Chapter 9 Integrated systems Market Estimates & Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia-Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia-Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Accenture

- 10.2 IBM Corporation

- 10.3 Tata Consultancy Services Limited

- 10.4 Oracle Corporation

- 10.5 BAE Systems

- 10.6 Wipro Limited

- 10.7 Cognizant

- 10.8 Deloitte Touche Tohmatsu Limited

- 10.9 Infosys Limited

- 10.10 MDS Systems Integration (MDS SI)

- 10.11 HCL Technologies

- 10.12 Capgemini

- 10.13 Atos SE

- 10.14 Fujitsu Limited

- 10.15 Cisco Systems, Inc.

- 10.16 Hewlett Packard Enterprise (HPE)

- 10.17 SAP SE

- 10.18 NEC Corporation

- 10.19 Siemens AG

- 10.20 CGI Inc.

- 10.21 DXC Technology

- 10.22 Tech Mahindra

- 10.23 Hitachi, Ltd.(Vantara)

全球系统整合市场规模、份额、趋势和成长分析报告(2026-2034年)

全球系统整合市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球整合系统市场报告

2026年全球整合系统市场报告 系统整合市场报告(按服务、最终用户产业和地区划分),2026-2034年全球系统整合市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

系统整合市场报告(按服务、最终用户产业和地区划分),2026-2034年全球系统整合市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 整合系统市场-全球产业规模、份额、趋势、机会、预测:按产品、服务、最终用户、地区和竞争对手划分,2021-2031年

整合系统市场-全球产业规模、份额、趋势、机会、预测:按产品、服务、最终用户、地区和竞争对手划分,2021-2031年 联觉与运算整合解决方案市场(按解决方案类型、组件、部署类型和应用划分)-2026-2032年全球预测日本系统整合市场报告(按服务、最终用户产业和地区划分,2026-2034 年)

联觉与运算整合解决方案市场(按解决方案类型、组件、部署类型和应用划分)-2026-2032年全球预测日本系统整合市场报告(按服务、最终用户产业和地区划分,2026-2034 年) 系统整合市场规模、份额和成长分析(按服务类型、公司规模、最终用途和地区划分)-2026-2033年产业预测

系统整合市场规模、份额和成长分析(按服务类型、公司规模、最终用途和地区划分)-2026-2033年产业预测 系统整合的全球市场(~2035年):各服务形式,各类型企业,各产业类型,各地区,产业趋势,预测整合系统市场 - 预测 2025-2030

系统整合的全球市场(~2035年):各服务形式,各类型企业,各产业类型,各地区,产业趋势,预测整合系统市场 - 预测 2025-2030