|

市场调查报告书

商品编码

1959545

货物扫描设备市场机会、成长要素、产业趋势分析及2026年至2035年预测。Cargo Scanning Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

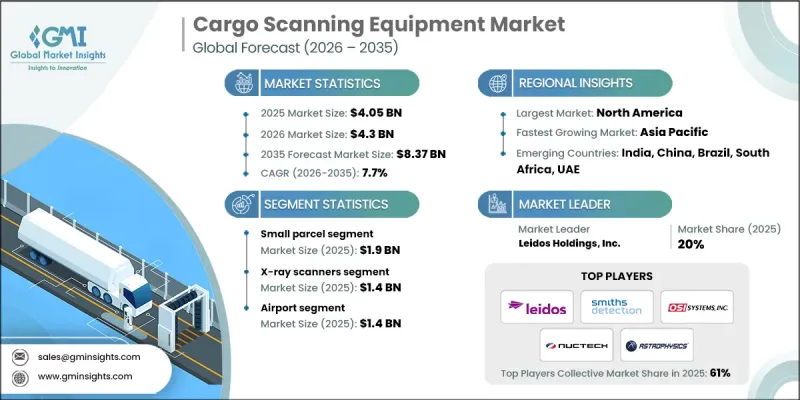

2025 年全球货物扫描设备市场价值为 40.5 亿美元,预计到 2035 年将达到 83.7 亿美元,年复合成长率为 7.7%。

全球贸易的快速扩张、货柜货运量的激增以及日益增长的全球安全隐患,共同推动了这个市场的成长。各国政府和运输管理部门正大力推行更严格的海关、边境管制和港口安全法规,加速了3D X光扫描仪和电脑断层扫描(CT)扫描仪等先进影像技术的应用。人工智慧(AI)和自动化技术在货物检查中的应用,透过提高准确性、减少人为错误和提升处理能力,进一步促进了市场成长。随着安全威胁的不断演变,各国政府正大力投资研发能够侦测复杂隐蔽手段、保护关键基础设施并保障公共的下一代扫描系统。在增强型数据分析和即时监控的支援下,主动风险管理模式的转变,持续推动全球对技术主导高效能货物扫描解决方案的需求。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 40.5亿美元 |

| 预测金额 | 83.7亿美元 |

| 复合年增长率 | 7.7% |

预计到2025年,小小包裹市场规模将达到19亿美元。随着电子商务的快速发展,迫切需要对小包裹进行快速、非侵入性的检查,以确保可靠的交付并符合监管要求。小件包裹中走私货、违禁品和非法物质的风险日益增加,迫使物流和邮政服务提供者部署自动化、高吞吐量的扫描系统。设备製造商正致力于开发紧凑型、高速扫描解决方案,以优化应用于末端配送中心和高容量小包裹分类中心。这些系统必须在不影响营运效率的前提下,提供可靠的检测结果,同时最大限度地减少对供应链营运的影响。

预计到2025年,X光扫描仪市场规模将达14亿美元。机场、港口和海关部门正越来越多地采用先进的X射线扫描仪,对各类货物进行快速、无损的检查。多重视角和3D X射线成像技术的进步提高了侦测精度,减少了误报,并提升了操作人员的工作效率。製造商正在投资研发具备自动威胁侦测功能的高解析度X射线系统,能够在不影响处理能力或安全标准的前提下,对货柜、托盘和散装货物进行无缝检查。

预计到2025年,北美货物扫描设备市场份额将达到33.9%,这主要得益于其庞大的贸易量、先进的港口和边境基础设施以及严格的法规结构。海关和国防安全保障机构正在海港、机场和陆地边境实施全面的筛检程序,从而对具备卓越威胁侦测能力的自动化、高通量扫描设备产生了持续的需求。北美当局正在加速整合人工智慧驱动的影像处理和分析技术,以支援基于风险的货物检查,在保持严格安全标准的同时,加快清关速度。该地区在货物检查操作的创新和效率方面持续引领行业标竿。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 全球贸易量和货柜货运量增加

- 安全威胁和走私活动日益增多

- 更严格的海关、边境管制和港口安全规定

- 引进先进影像技术(CT、3D X射线)

- 将人工智慧和自动化技术应用于货物检验

- 挑战与困难

- 扫描系统高昂的购置成本与维修成本

- 营运复杂性和对熟练劳动力的需求

- 促进因素

- 成长潜力分析

- 监理情势

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 供应链韧性

- 地缘政治分析

- 劳动力分析

- 数位转型

- 併购和策略联盟的趋势

- 风险评估与管理

- 重大合约采购范例(2022-2025 年)

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 市场集中度分析

- 主要企业的竞争标竿分析

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 地理位置比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 产品系列比较

- 2022-2025 年重大发展

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张和投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估算与预测:依设备类型划分,2022-2035年

- 药物微量检测装置

- 非电脑断层扫描器

- X光扫描仪

- 爆炸物微量检测装置(ETD)

- 辐射检测器

- 其他的

第六章 市场估价与预测:依货物尺寸划分,2022-2035年

- 小小包裹

- 散货

- 超大货物

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 主要趋势

- 飞机场

- 火车站

- 边境管制

- 物流/运输

- 工业和製造设施

- 其他的

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第九章:公司简介

- 主要企业

- OSI Systems

- Smiths Detection Group Ltd.

- Leidos Holdings, Inc.

- Nuctech Company Limited

- 按地区分類的主要企业

- 北美洲

- Astrophysics, Inc.

- Autoclear LLC

- TODD Research

- 欧洲

- CEIA

- Gilardoni SpA

- Braun & Co. Limited

- 亚太地区

- LINEV Systems

- 北美洲

- 小众/颠覆者

- Westminster Group Plc

The Global Cargo Scanning Equipment Market was valued at USD 4.05 billion in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 8.37 billion by 2035.

The market is driven by the rapid growth in global trade, surging containerized cargo volumes, and rising security concerns worldwide. Governments and transport authorities are increasingly enforcing stricter customs, border control, and port security regulations, pushing the adoption of advanced imaging technologies such as 3D X-ray and computed tomography (CT) scanners. Integration of artificial intelligence and automation in cargo inspection is further accelerating market growth by enhancing accuracy, reducing human error, and increasing throughput. As security threats evolve, authorities are investing heavily in next-generation scanning systems capable of detecting sophisticated concealment methods, protecting critical infrastructure, and ensuring public safety. The shift toward proactive risk management, supported by enhanced data analytics and real-time monitoring, continues to drive demand for technology-driven, high-performance cargo scanning solutions globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.05 Billion |

| Forecast Value | $8.37 Billion |

| CAGR | 7.7% |

The small parcel segment reached USD 1.9 billion in 2025. Rapid growth in e-commerce has created an urgent need for fast, non-intrusive screening of small packages to ensure timely deliveries while maintaining regulatory compliance. The rising risk of contraband, prohibited items, and illegal substances in small shipments has compelled logistics and postal service providers to adopt automated, high-throughput scanning systems. Equipment manufacturers are focusing on developing compact, high-speed scanning solutions optimized for last-mile distribution hubs and high-volume parcel sorting centers. These systems must provide reliable detection without slowing operational efficiency, while also ensuring minimal disruption to supply chain operations.

The X-ray scanners segment accounted for USD 1.4 billion in 2025. Airports, seaports, and customs authorities are increasingly deploying advanced X-ray scanners to perform rapid, non-intrusive inspections of diverse cargo types. Technological improvements in multi-view and 3D X-ray imaging have enhanced detection accuracy, reduced false positives, and increased operator efficiency. Manufacturers are investing in high-resolution X-ray systems equipped with automated threat detection capabilities, enabling seamless inspection of containers, pallets, and bulk cargo without compromising throughput or security standards.

North America Cargo Scanning Equipment Market held 33.9% share in 2025 due to high trade volumes, advanced port and border infrastructure, and strict regulatory frameworks. Customs and homeland security agencies employ comprehensive screening protocols across maritime ports, airports, and land borders, creating steady demand for automated, high throughput scanning equipment with superior threat detection capabilities. North American authorities are increasingly integrating AI-driven imaging and analytics to support risk-based cargo inspections, allowing faster clearance while maintaining robust security standards. The region continues to set benchmarks for innovation and efficiency in cargo screening operations.

Key players in the Global Cargo Scanning Equipment Market include Autoclear LLC, OSI Systems, Smiths Detection Group Ltd., Astrophysics, Inc., Gilardoni S.p.A., LINEV Systems, TODD Research, Leidos Holdings, Inc., CEIA, Braun & Co. Limited, Nuctech Company Limited, and Westminster Group Plc. Companies in the cargo scanning equipment market are pursuing several strategies to strengthen their market presence. Continuous innovation in imaging technologies, such as 3D and CT scanners with AI-assisted threat detection, is a core focus. Firms are forming strategic partnerships with ports, airports, and logistics providers to expand deployment and service networks. Investment in research and development enhances system reliability, speed, and accuracy to meet evolving regulatory requirements. Manufacturers are also emphasizing modular, scalable systems to accommodate different cargo sizes and inspection environments.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Equipment type trends

- 2.2.2 Cargo size trends

- 2.2.3 End-use trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026 - 2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global trade and containerized cargo volumes

- 3.2.1.2 Increasing security threats and smuggling activities

- 3.2.1.3 Stricter customs, border control, and port security regulations

- 3.2.1.4 Adoption of advanced imaging technologies (CT, 3D x-ray)

- 3.2.1.5 Integration of AI and automation in cargo inspection

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High capital and maintenance costs of scanning systems

- 3.2.2.2 Operational complexity and skilled workforce requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Geopolitical Analysis

- 3.12 Workforce Analysis

- 3.13 Digital Transformation

- 3.14 Mergers, Acquisitions, and Strategic Partnerships Landscape

- 3.15 Risk Assessment and Management

- 3.16 Major Contract Awards (2022 - 2025)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Narcotics Trace Detectors

- 5.3 Non-computed Tomography

- 5.4 X-ray Scanners

- 5.5 Explosive Trace Detectors (ETDs)

- 5.6 Radiation Detectors

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Cargo Size, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Small Parcels

- 6.3 Break Pallet Cargo

- 6.4 Oversized Cargo

Chapter 7 Market Estimates and Forecast, By End-Use, 2022 - 2035 (USD Million)

- 7.1 Key Trends

- 7.2 Airports

- 7.3 Railway Station

- 7.4 Border Control

- 7.5 Logistics and Transportation

- 7.6 Industrial and Manufacturing facilities

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 OSI Systems

- 9.1.2 Smiths Detection Group Ltd.

- 9.1.3 Leidos Holdings, Inc.

- 9.1.4 Nuctech Company Limited

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Astrophysics, Inc.

- 9.2.1.2 Autoclear LLC

- 9.2.1.3 TODD Research

- 9.2.2 Europe

- 9.2.2.1 CEIA

- 9.2.2.2 Gilardoni S.p.A.

- 9.2.2.3 Braun & Co. Limited

- 9.2.3 Asia Pacific

- 9.2.3.1 LINEV Systems

- 9.2.1 North America

- 9.3 Niche / Disruptors

- 9.3.1 Westminster Group Plc