|

市场调查报告书

商品编码

1959551

施工机械租赁市场机会、成长要素、产业趋势分析及2026年至2035年预测Construction Equipment Rental Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

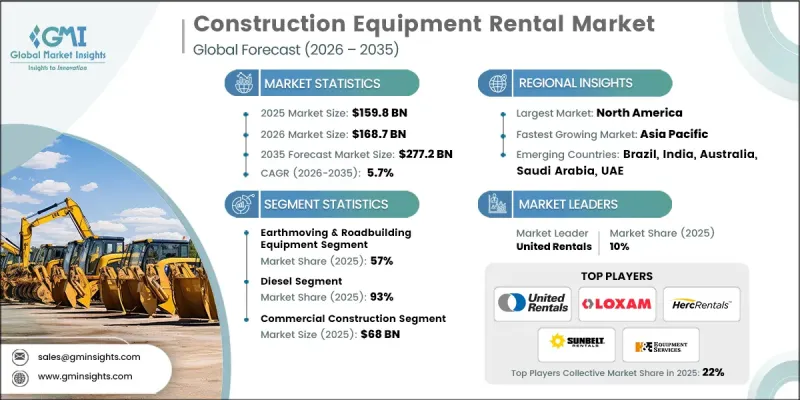

2025年全球施工机械租赁市场价值1,598亿美元,预计2035年将达2,772亿美元,年复合成长率为5.7%。

在住宅、商业和大型基础设施计划中,对土木工程施工机械、物料输送设备和高空作业平台的需求日益增长。中小型承包商是租赁解决方案最积极的采用者,而大型承包商也在扩大租赁设备的使用,以满足尖峰时段需求,并在无需长期投资的情况下获得专用设备。租赁公司正在转型经营模式,专注于客户维繫、服务商品搭售和可预测的定价。透过扩大设备规模,瞄准可再生能源、隧道建设和大型基础设施等高价值行业,供应商可以提供客製化设计的设备,计划专属合同,并建立忠实的基本客群。这种方式使租赁公司能够在满足不断变化的建筑需求的同时,提高营运效率和盈利。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 1598亿美元 |

| 预测金额 | 2772亿美元 |

| 复合年增长率 | 5.7% |

预计到 2025 年,土木工程和道路施工设备领域将占据 57% 的市场份额,并从 2026 年到 2035 年以 4.9% 的复合年增长率增长。各公司正在整合其车队并收购互补业务,以提供更广泛的机械选择,扩大其区域影响力,并服务大规模的现有基本客群。

柴油动力设备市占率高达93%,预计2026年至2035年将以5.2%的复合年增长率成长。凭藉其可靠性、动力性和高效性,柴油机械仍然是土木工程、铺路和混凝土施工等重型作业的首选。 Rental Fleet将继续专注于柴油动力设备,以满足承包商在无法采用传统动力解决方案的计划中的需求。

预计到2025年,美国施工机械租赁市场规模将达756亿美元。美国市场的成长主要得益于强劲的基础建设支出、成熟的商业建筑市场以及完善的租赁行业。承包商越来越依赖租赁设备来扩大营运规模、降低资本支出,并为短期或高需求计划取得专用机械。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 成本结构

- 利润率

- 每个阶段增加的价值

- 垂直整合趋势

- 颠覆者

- 影响因素

- 促进因素

- 联网汽车和软体定义汽车的日益普及。

- 消费者对个人化和免持操作的需求日益增长。

- 电动车 (EV) 和自动驾驶汽车领域的扩张

- 售后市场和软体升级机会增加

- 产业潜在风险与挑战

- 联网汽车和软体定义汽车的日益普及。

- 消费者对个人化和免持操作的需求日益增长。

- 市场机会

- AI驱动的预测和生成助手

- 多模态人机介面实施现状

- 云端连线和OTA更新

- 智慧驾驶座区域部署状况

- 促进因素

- 技术趋势与创新生态系统

- 目前技术

- 新兴技术

- 成长潜力分析

- 监理情势

- 北美洲

- 职业安全与健康管理局(OSHA)

- 美国环保署(EPA)排放标准

- 加拿大运输部职场安全与设备法规

- 欧洲

- 欧盟机械指令 (MD) 和 CE 认证

- 欧盟第五阶段排放气体法规

- ISO 20474(土木工程施工机械安全标准)

- 亚太地区

- 日本产业安全卫生法

- 中国国家施工机械标准(GB标准)

- 印度AIS/排放气体和安全指南

- 拉丁美洲

- 巴西INMETRO认证

- 哥伦比亚劳动部安全法规

- 阿根廷施工机械安全指南

- 中东和非洲

- 阿联酋联邦人力资源及资源机构及ESMA标准

- 阿曼劳动部设备安全规章

- 南非SABS施工机械标准

- 北美洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- OEM定价模式

- 售后市场价格趋势

- 订阅购买模式

- 区域价格波动

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

- 资产利用率和车队生产力基准测试

- 电气化准备与转型蓝图

- 租赁渗透率与所有权模式转换分析

- 数位化和远端资讯处理的影响分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 竞争定位矩阵

- 战略展望矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估价与预测:依产品划分,2022-2035年

- 土木工程及道路施工机械

- 后铲

- 挖土机

- 装载机

- 压实设备

- 其他的

- 物料输送和起重机

- 储存和运输设备

- 工程系统

- 工业车辆

- 散装物料输送设备

- 混凝土设备

- 混凝土泵

- 破碎机

- 运输搅拌车

- 沥青铺筑机

- 混凝土搅拌站

第六章 市场估计与预测:依驱动因素划分,2022-2035年

- 柴油引擎

- CNG/LNG

- 电的

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 住宅

- 商业建筑

- 工业建筑

- 采矿和采石

第八章 市场估算与预测:依最终用途划分,2022-2035年

- 建设公司

- 矿业营运商

- 租赁公司

- 政府/市政当局

- 工业用户

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 世界公司

- Ashtead Technology(Sunbelt Rentals)

- Capital Equipment Rental

- Elliott Equipment Company

- Herc Rentals

- Hertz Equipment Rentals

- JLG

- John Deere Rental

- Loxam

- Ritchie Bros. Auctioneers

- United Rentals

- 当地公司

- Allmand Brothers

- Atlas Rents

- Bakersfield Rental

- Maxim Crane Works

- NESCO Rentals

- Riwal

- Stephenson's Rental Services

- Sunstate Equipment

- Toromont CAT

- WesternOne

- 新兴企业

- Allmand Brothers

- Capital Equipment Rental

- Bakersfield Rental

- Sunstate Equipment

The Global Construction Equipment Rental Market was valued at USD 159.8 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 277.2 billion by 2035.

The industry is witnessing high demand for earthmoving, materials handling, and aerial lift equipment across residential, commercial, and large infrastructure projects. Small and mid-sized contractors are among the fastest adopters of rental solutions, while large contractors are increasingly using rented machinery to meet peak demands and access specialized equipment without long-term investment. Rental companies are shifting their business models, focusing on customer retention, service bundling, and predictable pricing. Expansion of fleets targeted to high-value sectors, such as renewable energy, tunneling, and major infrastructure, allows providers to offer purpose-built equipment, secure project-specific contracts, and develop loyal customer bases. This approach ensures rental companies can cater to evolving construction demands while improving operational efficiency and profitability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $159.8 Billion |

| Forecast Value | $277.2 Billion |

| CAGR | 5.7% |

The earthmoving and roadbuilding equipment segment held a 57% share in 2025 and is projected to grow at a CAGR of 4.9% from 2026 to 2035. Companies are consolidating fleets and acquiring complementary businesses to provide diversified machinery options, expand regional presence, and serve larger established customer bases.

The diesel-powered equipment segment held a 93% share and is expected to grow at a CAGR of 5.2% between 2026 and 2035. Diesel machinery remains the preferred choice for heavy-duty operations due to its reliability, power, and efficiency in earthmoving, paving, and concrete applications. Rental fleets continue to focus on diesel-powered units to meet contractor needs in projects where electricity-based solutions are not feasible.

U.S. Construction Equipment Rental Market reached USD 75.6 billion in 2025. Growth in the U.S. is driven by robust infrastructure spending, mature commercial construction, and the established rental industry. Contractors increasingly rely on rental equipment to scale operations, reduce capital expenditure, and access specialized machinery for short-term or high-demand projects.

Key players operating in the Global Construction Equipment Rental Market include Allmand Brothers, Ashtead Technology (Sunbelt Rentals), Atlas Rents, Bakersfield Rental, Herc Rentals, JLG, John Deere Rental, Loxam, Ritchie Bros. Auctioneers, and United Rentals. Companies in the Construction Equipment Rental Market are strengthening their position by expanding regional and sector-specific fleets, acquiring complementary rental businesses, and offering bundled services with predictable pricing. Firms are investing in purpose-built equipment for high-value projects, forming strategic alliances with contractors, and leveraging digital platforms for equipment tracking and maintenance. Focus on customer loyalty programs, flexible rental terms, and specialized training services enhances client retention while improving operational efficiency. Emphasis on renewable energy, tunneling, and infrastructure sectors ensures access to premium contracts and market growth opportunities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Propulsion

- 2.2.4 Application

- 2.2.5 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of connected and software-defined vehicles.

- 3.2.1.2 Rising consumer demand for personalization and hands-free operation

- 3.2.1.3 Expansion of EV and autonomous vehicle segments

- 3.2.1.4 Increasing aftermarket and software upgrade opportunities

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Growing adoption of connected and software-defined vehicles.

- 3.2.2.2 Rising consumer demand for personalization and hands-free operation

- 3.2.3 Market opportunities

- 3.2.3.1 AI-driven predictive and generative assistants

- 3.2.3.2 Multimodal HMI adoption

- 3.2.3.3 Cloud connectivity and OTA updates

- 3.2.3.4 Regional adoption of intelligent cockpits

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 Occupational Safety and Health Administration (OSHA)

- 3.5.1.2 Environmental Protection Agency (EPA) Emission Standards

- 3.5.1.3 Transport Canada Workplace Safety & Equipment Regulations

- 3.5.2 Europe

- 3.5.2.1 EU Machinery Directive (MD) & CE Certification

- 3.5.2.2 EU Stage V Emission Standards

- 3.5.2.3 ISO 20474 (Earth-moving Machinery Safety Standards)

- 3.5.3 Asia-Pacific

- 3.5.3.1 Japan Industrial Safety & Health Act

- 3.5.3.2 China GB Standards for Construction Machinery

- 3.5.3.3 India AIS/Emission & Safety Guidelines

- 3.5.4 Latin America

- 3.5.4.1 Brazil INMETRO Certification

- 3.5.4.2 Colombia Ministry of Labor Safety Regulations

- 3.5.4.3 Argentina Construction Equipment Safety Guidelines

- 3.5.5 Middle East & Africa

- 3.5.5.1 UAE Federal Authority for Human Resources & ESMA Standards

- 3.5.5.2 Oman Ministry of Labor Equipment Safety Regulations

- 3.5.5.3 South Africa SABS Construction Equipment Standards

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Price trends

- 3.8.1 OEM Pricing models

- 3.8.2 Aftermarket pricing trends

- 3.8.3 Subscription purchase models

- 3.8.4 Regional price variations

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Asset Utilization & Fleet Productivity Benchmarking

- 3.12 Electrification Readiness & Transition Roadmap

- 3.13 Rental Penetration & Ownership Shift Analysis

- 3.14 Digitalization & Telematics Impact Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Earthmoving & roadbuilding equipment

- 5.2.1 Backhoe

- 5.2.2 Excavator

- 5.2.3 Loader

- 5.2.4 Compaction equipment

- 5.2.5 Others

- 5.3 Material handling and cranes

- 5.3.1 Storage and handling equipment

- 5.3.2 Engineered systems

- 5.3.3 Industrial trucks

- 5.3.4 Bulk material handling equipment

- 5.4 Concrete equipment

- 5.4.1 Concrete pumps

- 5.4.2 Crusher

- 5.4.3 Transit mixers

- 5.4.4 Asphalt pavers

- 5.4.5 Batching plants

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 CNG/LNG

- 6.4 Electric

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Residential Construction

- 7.3 Commercial Construction

- 7.4 Industrial Construction

- 7.5 Mining & Quarrying

Chapter 8 Market Estimates & Forecast, By End use, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Construction Companies

- 8.3 Mining Operators

- 8.4 Rental Companies

- 8.5 Government & Municipalities

- 8.6 Industrial Users

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 North America

- 9.1.1 US

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Belgium

- 9.2.7 Netherlands

- 9.2.8 Sweden

- 9.2.9 Russia

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 Singapore

- 9.3.6 South Korea

- 9.3.7 Vietnam

- 9.3.8 Indonesia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 South Africa

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Companies

- 10.1.1 Ashtead Technology (Sunbelt Rentals)

- 10.1.2 Capital Equipment Rental

- 10.1.3 Elliott Equipment Company

- 10.1.4 Herc Rentals

- 10.1.5 Hertz Equipment Rentals

- 10.1.6 JLG

- 10.1.7 John Deere Rental

- 10.1.8 Loxam

- 10.1.9 Ritchie Bros. Auctioneers

- 10.1.10 United Rentals

- 10.2 Regional Companies

- 10.2.1 Allmand Brothers

- 10.2.2 Atlas Rents

- 10.2.3 Bakersfield Rental

- 10.2.4 Maxim Crane Works

- 10.2.5 NESCO Rentals

- 10.2.6 Riwal

- 10.2.7 Stephenson's Rental Services

- 10.2.8 Sunstate Equipment

- 10.2.9 Toromont CAT

- 10.2.10 WesternOne

- 10.3 Emerging Companies

- 10.3.1 Allmand Brothers

- 10.3.2 Capital Equipment Rental

- 10.3.3 Bakersfield Rental

- 10.3.4 Sunstate Equipment

2026年全球施工机械租赁市场报告2026年全球重型建筑设备租赁市场报告

2026年全球施工机械租赁市场报告2026年全球重型建筑设备租赁市场报告 施工机械及工具租赁平台市场预测至2034年-全球分析(依设备类型、租赁模式、定价模式、客户类型、最终用户及地区划分)

施工机械及工具租赁平台市场预测至2034年-全球分析(依设备类型、租赁模式、定价模式、客户类型、最终用户及地区划分) 重型施工机械租赁市场-全球产业规模、份额、趋势、机会与预测:按设备类型、应用、地区和竞争格局划分,2021-2031年

重型施工机械租赁市场-全球产业规模、份额、趋势、机会与预测:按设备类型、应用、地区和竞争格局划分,2021-2031年 日本施工机械租赁市场报告:按解决方案、设备、类型、应用、产业和地区划分(2026-2034年)

日本施工机械租赁市场报告:按解决方案、设备、类型、应用、产业和地区划分(2026-2034年) 施工机械租赁市场规模、份额及成长分析(依产品类型、动力系统、应用及地区划分)-2026-2033年产业预测

施工机械租赁市场规模、份额及成长分析(依产品类型、动力系统、应用及地区划分)-2026-2033年产业预测 施工机械租赁市场规模、份额及趋势分析报告:按产品、驱动系统、地区和细分市场预测(2026-2033 年)

施工机械租赁市场规模、份额及趋势分析报告:按产品、驱动系统、地区和细分市场预测(2026-2033 年) 施工机械租赁市场:2025-2030 年全球预测(按设备类型、租赁期间、动力来源、营运、租赁模式和应用)

施工机械租赁市场:2025-2030 年全球预测(按设备类型、租赁期间、动力来源、营运、租赁模式和应用) 施工机械租赁:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

施工机械租赁:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 全球施工机械租赁软体市场:市场规模(按产品、应用和地区划分)、未来预测

全球施工机械租赁软体市场:市场规模(按产品、应用和地区划分)、未来预测