|

市场调查报告书

商品编码

1959573

工业标籤印表机市场机会、成长要素、产业趋势分析及2026年至2035年预测Industrial Label Printer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

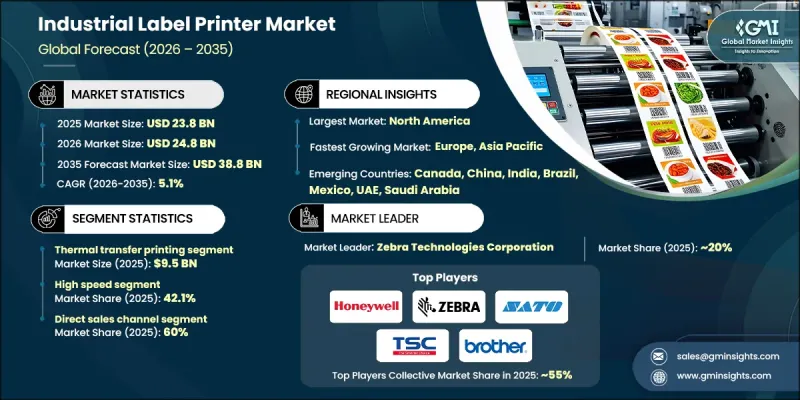

2025 年全球工业标籤印表机市场价值为 238 亿美元,预计到 2035 年将达到 388 亿美元,年复合成长率为 5.1%。

市场成长与整个生产环境中工业自动化和数位化製造方法的加速普及密切相关。随着製造商扩大营运规模并实现设施现代化,对能够提供稳定品质、运作可靠性和长期耐用性的标籤系统的需求日益增长。工业标籤印表机正逐渐被视为自动化生产生态系统中不可或缺的基础设施,有助于提高识别准确性、资产可视性和简化工作流程管理。向互联製造环境的转变进一步增加了对能够与数据驱动系统和即时监控平台整合的智慧标籤解决方案的需求。随着产量的增加和品质要求的日益严格,製造商不得不投资先进的列印技术,以提高整个工业运营的效率、准确性和可追溯性。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 238亿美元 |

| 预测金额 | 388亿美元 |

| 复合年增长率 | 5.1% |

热转印列印市场预计在2025年达到95亿美元,并在2026年至2035年间以5%的复合年增长率成长。这种列印方法之所以被广泛采用,是因为它能够製作高清标籤,即使在恶劣的环境条件下也能保持效能。其耐用性满足长期识别和合规性要求,持续推动受监管行业和高性能工业应用的需求。

预计到2025年,高速工业标籤印表机市场占有率将达到42.1%,并在2035年之前以5.7%的复合年增长率成长。对更快生产速度和更短交货週期的需求推动了高功率印表机的普及,这类印表机能够在保持精度的同时最大限度地减少停机时间。物流密集型业务订单量的成长进一步巩固了该细分市场的主导地位。

美国工业标籤印表机市场预计到 2025 年将达到 76 亿美元,并从 2026 年到 2035 年以 4.9% 的复合年增长率成长。这一市场扩张的驱动力是先进的製造能力、强大的物流基础设施以及越来越多依赖工业级标籤解决方案的整合自动化系统。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 製造业和工业自动化的扩张

- 物流、仓储业和电子商务的快速成长

- 人们越来越关注产品可追溯性和序列化

- 产业潜在风险与挑战

- 对消耗品和价格波动的依赖

- 激烈的竞争和利润率压力

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 透过印刷技术

- 监理情势

- 标准和合规要求

- 区域法规结构

- 认证标准

- 贸易统计

- 主要进口国

- 主要出口国

- 波特的分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 市场估价与预测:依印刷技术划分,2022-2035年

- 热转印

- 直接热感列印

- 雷射列印

- 喷墨列印

- 特殊印刷技术

第六章 市场估算与预测:依自动化程度划分,2022-2035年

- 手动的

- 半自动

- 全自动

第七章 市场估计与预测:依速度划分,2022-2035年

- 慢速

- 高速

- 中速

第八章 市场估算与预测:以连结方式划分,2022-2035年

- 有线连接

- USB

- 乙太网路

- 序号

- 无线的

- Wi-Fi

- Bluetooth

- NFC

第九章 市场估计与预测:依最终用途划分,2022-2035年

- 消费品/家居用品

- 医疗和製药领域

- 化学品和危险材料

- 食品/饮料

- 对于汽车和航太行业

- 电子设备

- 纺织服装

- 其他的

第十章 市场估价与预测:依通路划分,2022-2035年

- 直销

- 间接销售

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 印尼

- 马来西亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

第十二章:公司简介

- Avery Dennison Corporation

- Brady Corporation

- Brother Industries, Ltd.

- Datalogic SpA

- Godex International Co., Ltd.

- Honeywell International Inc.

- Oki Electric Industry Co., Ltd.

- Primera Technology, Inc.

- Printronix, LLC

- SATO Holdings Corporation

- Seiko Epson Corporation

- Toshiba Tec Corporation

- TSC Auto ID Technology Co., Ltd.

- Wasp Barcode Technologies

- Zebra Technologies Corporation

The Global Industrial Label Printer Market was valued at USD 23.8 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 38.8 billion by 2035.

Market growth is linked to the accelerating adoption of industrial automation and digital manufacturing practices across production environments. As manufacturers scale operations and modernize facilities, demand is rising for labeling systems that deliver consistent quality, operational reliability, and long-term durability. Industrial label printers are increasingly viewed as essential infrastructure within automated production ecosystems, supporting identification accuracy, asset visibility, and streamlined workflow management. The shift toward connected manufacturing environments has further increased the need for intelligent labeling solutions that integrate with data-driven systems and real-time monitoring platforms. Growing production volumes and stricter quality expectations are pushing manufacturers to invest in advanced printing technologies that enhance efficiency, precision, and traceability across industrial operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $23.8 Billion |

| Forecast Value | $38.8 Billion |

| CAGR | 5.1% |

The thermal transfer printing segment generated USD 9.5 billion in 2025 and is expected to grow at a CAGR of 5% from 2026 to 2035. This printing method is widely adopted due to its ability to produce high-clarity labels that maintain performance under demanding environmental conditions. Its durability supports long-term identification and compliance requirements, which continue to drive demand across regulated and high-performance industrial applications.

The high-speed industrial label printers segment accounted for 42.1% share in 2025 and is forecast to grow at a CAGR of 5.7% through 2035. Increasing production speeds and shorter fulfillment cycles are encouraging the adoption of high-output printers capable of maintaining accuracy while minimizing downtime. Rising order volumes across logistics-intensive operations further reinforce this segment's leadership.

U.S. Industrial Label Printer Market reached USD 7.6 billion in 2025 and is projected to grow at a CAGR of 4.9% from 2026 to 2035. Market expansion is supported by advanced manufacturing capabilities, strong logistics infrastructure, and increasing use of integrated automation systems that rely on industrial-grade labeling solutions.

Key companies operating in the Global Industrial Label Printer Market include Zebra Technologies Corporation, Honeywell International Inc., SATO Holdings Corporation, Avery Dennison Corporation, Brady Corporation, Toshiba Tec Corporation, Seiko Epson Corporation, Brother Industries, Ltd., Printronix, LLC, TSC Auto ID Technology Co., Ltd., Datalogic S.p.A., Oki Electric Industry Co., Ltd., Godex International Co., Ltd., Wasp Barcode Technologies, and Primera Technology, Inc. Companies in the industrial label printer market are strengthening their market positions through continuous technology enhancement and portfolio diversification. Many players are focusing on high-speed, high-resolution printing capabilities that support automated and data-driven production environments. Integration with enterprise software platforms and smart factory systems is a key strategic priority. Manufacturers are also investing in ruggedized designs and energy-efficient technologies to improve lifecycle value. Strategic partnerships with logistics providers and industrial solution integrators are expanding market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Print technology

- 2.2.3 Automation level

- 2.2.4 Speed

- 2.2.5 Connectivity

- 2.2.6 End use

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of manufacturing and industrial automation

- 3.2.1.2 Rapid growth in logistics, warehousing, and e-commerce

- 3.2.1.3 Increasing focus on product traceability and serialization

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Dependence on consumables and price volatility

- 3.2.2.2 Intense price competition and margin pressure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By print technology

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Print Technology, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Thermal transfer printing

- 5.3 Direct thermal printing

- 5.4 Laser printing

- 5.5 Inkjet printing

- 5.6 Specialty printing technologies

Chapter 6 Market Estimates & Forecast, By Automation Level, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automated

- 6.4 Fully automated

Chapter 7 Market Estimates & Forecast, By Speed, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Low speed

- 7.3 High speed

- 7.4 Mid speed

Chapter 8 Market Estimates & Forecast, By Connectivity, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Wired

- 8.2.1 USB

- 8.2.2 Ethernet

- 8.2.3 Serial

- 8.3 Wireless

- 8.3.1 Wi-Fi

- 8.3.2 Bluetooth

- 8.3.3 NFC

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Consumer good & home care

- 9.3 Healthcare and pharmaceuticals

- 9.4 Chemical and hazardous materials

- 9.5 Food and beverage

- 9.6 Automotive and aerospace

- 9.7 Electronics

- 9.8 Textile and apparel

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Avery Dennison Corporation

- 12.2 Brady Corporation

- 12.3 Brother Industries, Ltd.

- 12.4 Datalogic S.p.A.

- 12.5 Godex International Co., Ltd.

- 12.6 Honeywell International Inc.

- 12.7 Oki Electric Industry Co., Ltd.

- 12.8 Primera Technology, Inc.

- 12.9 Printronix, LLC

- 12.10 SATO Holdings Corporation

- 12.11 Seiko Epson Corporation

- 12.12 Toshiba Tec Corporation

- 12.13 TSC Auto ID Technology Co., Ltd.

- 12.14 Wasp Barcode Technologies

- 12.15 Zebra Technologies Corporation

标籤印刷市场:2026-2032年全球市场预测,依材料、印刷技术、应用及最终用途产业划分护理标籤印表机市场:按印表机类型、技术类型、应用程式和最终用户划分 - 全球预测,2026-2032 年双色标籤印表机市场(按最终用户产业、应用、产品类型、列印技术、连接方式和销售管道),全球预测,2026-2032年

标籤印刷市场:2026-2032年全球市场预测,依材料、印刷技术、应用及最终用途产业划分护理标籤印表机市场:按印表机类型、技术类型、应用程式和最终用户划分 - 全球预测,2026-2032 年双色标籤印表机市场(按最终用户产业、应用、产品类型、列印技术、连接方式和销售管道),全球预测,2026-2032年 全球工业标籤印表机市场规模、份额、趋势和成长分析报告(2026-2034年)

全球工业标籤印表机市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球标籤印刷市场报告2026年全球彩色标籤印刷市场报告专业彩色标籤印表机市场(按技术、墨水类型、媒体类型、最终用户产业、分销管道和最终用户划分),全球预测,2026-2032年

2026年全球标籤印刷市场报告2026年全球彩色标籤印刷市场报告专业彩色标籤印表机市场(按技术、墨水类型、媒体类型、最终用户产业、分销管道和最终用户划分),全球预测,2026-2032年 全球工业标籤印表机市场标籤彩色印刷市场规模(按类型、应用、区域范围、预测)

全球工业标籤印表机市场标籤彩色印刷市场规模(按类型、应用、区域范围、预测) 全球喷墨桌面彩色标籤印表机市场:截至 2031 年

全球喷墨桌面彩色标籤印表机市场:截至 2031 年