|

市场调查报告书

商品编码

1959575

辛酰甘氨酸市场机会、成长要素、产业趋势分析及2026年至2035年预测。Capryloyl Glycine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

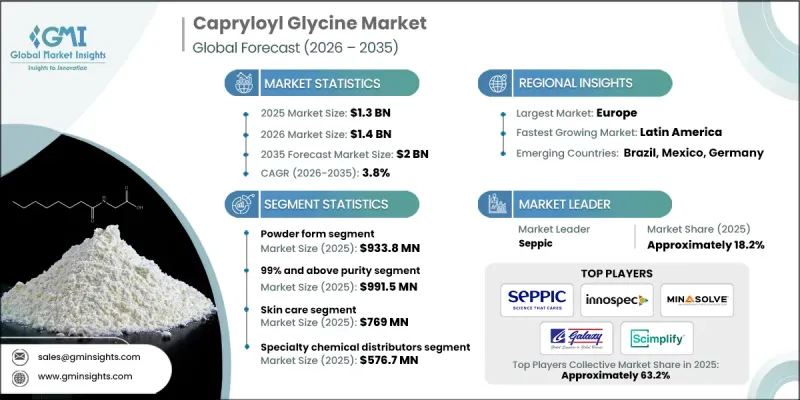

2025 年全球辛基甘胺酸市场价值为 13 亿美元,预计到 2035 年将达到 20 亿美元,年复合成长率为 3.8%。

在清洁美容配方日益普及以及个人保健产品中传统合成防腐剂使用减少的推动下,该市场持续稳定扩张。随着消费者对更温和、更易降解成分的需求不断增长,製造商正在使用辛酰甘氨酸等多功能化合物重新配製产品。这种胺基酸衍生物具有抗菌和皮肤调理功效,使其成为护肤、护髮和个人卫生用品中备受追捧的成分。随着痤疮、脂漏性皮肤炎和皮脂分泌过多等皮肤和头皮问题的日益增多,消费者对能够支持微生物群健康、控制皮脂分泌和保护皮肤屏障功能的配方有着日益增长的长期需求。辛酰甘氨酸正越来越多地被添加到抗痤疮治疗、头皮护理和敏感肌肤产品中,从而有助于在大众市场和高端市场保持稳定的消费。化妆品开发商正在优先考虑那些能够支持皮肤和头皮微生物群健康的成分,以满足消费者对产品功效、安全性和永续性的偏好。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 13亿美元 |

| 预测金额 | 20亿美元 |

| 复合年增长率 | 3.8% |

预计到2025年,粉末状辛酰甘氨酸市场规模将达到9.338亿美元。由于其保质期长、易于储存,且能够在大规模干混配方中实现精确计量,因此深受生产商青睐。粉末状辛酰甘氨酸尤其适用于稳定性和精确配方至关重要的客製化个人保健产品。同时,液体或水溶液形式的辛酰甘氨酸也因其易于添加到配方中、加工速度更快以及生产效率更高而日益普及。这两种形式的供应使生产商能够根据其营运扩充性和配方需求选择最佳形式,从而支援其在各种产品类型中的广泛应用。

预计到2025年,纯度为99%或以上的辛酰甘氨酸市场规模将达到9.915亿美元。高纯度辛酰甘氨酸尤其受到高端化妆品、药用化妆品和外用药物製剂的青睐,因为这些领域对原料的可追溯性和配方的精确性要求极高。更严格的监管标准、国际合规要求以及消费者对经皮肤病学测试的高品质产品日益增长的偏好,正在加速推动这一细分市场的需求成长。製造商正投资于先进的纯化技术,以实现产品差异化,提升产品性能,并确立自身作为能够满足严格品质要求的高端、特定应用解决方案供应商的地位。

预计到2025年,北美辛酰甘氨酸市场规模将达到3.529亿美元。该地区拥有巨大的成长潜力,这得益于其成熟的个人护理行业、较高的人均护肤支出以及日益兴起的「清洁美容」运动,该运动强调成分的透明度和永续性。美国是该地区最大的辛酰甘氨酸市场贡献者,其配方正不断寻求天然来源的多功能成分以满足消费者的需求。消费者对产品安全性的日益关注、对有益于肠道菌群的配方以及环保成分的需求,正在推动辛酰甘氨酸在大众市场和高端个人护理产品领域的广泛应用。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 消费者对清洁美容产品和天然防腐剂替代品的需求不断增长。

- 痤疮、脂漏性皮肤炎和头皮疾病的发生率持续上升。

- 加强对合成防腐剂监管的倡议

- 产业潜在风险与挑战

- 敏感族群可能出现皮肤刺激和过敏反应。

- 与传统的合成防腐剂相比,它的价格更高。

- 市场机会

- 口腔清洁用品和牙齿卫生产品领域尚未开发的潜力

- 拓展至药用级创伤护理及外用药物领域。

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 产品类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计资料(HS编码)(註:贸易统计仅提供主要国家的资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 市场估计与预测:依类型划分,2022-2035年

- 粉状(浓度90%或以上)

- 液体/水溶液

第六章 市场估计与预测:依纯度划分,2022-2035年

- 纯度95%至98%

- 纯度98%至99%

- 纯度超过99%

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 护肤

- 抗痘产品

- 抗皱和抗老化产品

- 控油及油性肌肤护理

- 调节pH平衡并恢復皮肤屏障功能。

- 皮肤保护产品

- 头髮护理和头皮护理

- 去屑产品

- 治疗脂漏性皮肤炎的产品

- 舒缓并缓解头皮刺激

- 护髮产品

- 止汗剂和除臭剂

- 除臭剂

- 止汗产品

- 创伤护理和外用药物

- 伤口敷料和创伤治疗产品

- 皮肤科药物

- 口腔清洁用品

- 牙膏配方

- 漱口水及口腔冲洗产品

第八章 市场估算与预测:依通路划分,2022-2035年

- 直销

- 特用化学品批发商

- 线上B2B平台

- 其他的

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十章:公司简介

- Seppic

- Scimplify

- ATAMAn KIMYA

- Pinpools GMBH

- Euro-Kemical SRL

- Sinerga SpA

- AE Chemie

- DRAVYOM Chemical Company

- DropBio

- Uniproma

- pecial Chem

- Zley Group

- Innospec Inc.

- Minasolve

- Euro-Kemical

- Galaxy Surfactants

The Global Capryloyl Glycine Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 3.8% to reach USD 2 billion by 2035.

The market has been steadily expanding, fueled by the growing adoption of clean beauty formulations and the shift away from conventional synthetic preservatives in personal care products. Consumers are increasingly demanding mild, skin-friendly, and biodegradable ingredients, prompting manufacturers to reformulate products with multifunctional compounds like capryloyl glycine. This amino acid derivative offers antimicrobial properties and skin-conditioning benefits, making it a highly sought-after ingredient across skincare, haircare, and hygiene products. Rising incidences of skin and scalp concerns such as acne, seborrheic dermatitis, and excess sebum production are driving long-term demand for formulations that support microbiome health, oil control, and barrier protection. Capryloyl glycine is increasingly incorporated into anti-acne treatments, scalp care solutions, and products for sensitive skin, helping maintain consistent consumption across both mass-market and premium segments. Cosmetic formulators are prioritizing ingredients that support skin and scalp microbiome health, aligning with consumer preferences for efficacy, safety, and sustainability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $2 Billion |

| CAGR | 3.8% |

The powder form segment reached USD 933.8 million in 2025. This form is widely favored by manufacturers due to its longer shelf life, ease of storage, and ability to be accurately dosed in large-scale and dry-blend formulations. Powder capryloyl glycine is particularly suitable for tailored personal care products where stability and precise incorporation are crucial. Meanwhile, liquid or aqueous solutions are gaining popularity because they integrate easily into formulations, accelerate processing, and enhance production efficiency. This dual availability allows manufacturers to select the most appropriate format based on operational scalability and formulation needs, supporting broader adoption across diverse product categories.

The segment with 99% and above purity generated USD 991.5 million in 2025. High-purity capryloyl glycine is particularly favored in premium cosmetics, cosmeceuticals, and medical topical applications, where ingredient traceability and formulation precision are critical. Rising regulatory standards, international compliance requirements, and consumer preference for dermatologically tested and high-quality products are accelerating demand in this segment. Manufacturers are investing in advanced purification technologies to differentiate their offerings, enhance product performance, and position themselves as suppliers of premium, application-specific solutions that meet stringent quality expectations.

North America Capryloyl Glycine Market accounted for USD 352.9 million in 2025. North America represents a major opportunity, driven by the region's sophisticated personal care industry, high per-capita skincare expenditure, and the growing clean-beauty movement emphasizing ingredient transparency and sustainability. The United States is the largest contributor in the region, with formulators increasingly seeking naturally derived, multifunctional ingredients to meet consumer expectations. Rising awareness of product safety, microbiome-friendly formulations, and the demand for environmentally responsible ingredients are fueling the adoption of capryloyl glycine in both mass-market and premium personal care categories.

Key companies operating in the Global Capryloyl Glycine Market include Sinerga S.p.A., Seppic, Euro-Kemical SRL, Innospec Inc., Zley Group, DropBio, AE Chemie, DRAVYOM Chemical Company, Pinpools GMBH, Special Chem, Minasolve, ATAMAN KIMYA, Galaxy Surfactants, and Uniproma. Companies in the Capryloyl Glycine Market are strengthening their position through multiple strategic initiatives. They are investing in R&D to develop high-purity and multifunctional derivatives to meet the demand for premium skincare and sensitive-skin applications. Manufacturers are optimizing production efficiency by offering both powder and liquid formats to suit different formulation requirements and large-scale industrial processing. Strategic partnerships with cosmetic and personal care brands are helping secure long-term supply agreements and enhance market penetration. Firms are also emphasizing sustainability, clean-label positioning, and compliance with global regulatory standards to attract environmentally conscious consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Form

- 2.2.3 Purity

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for clean beauty & natural preservative alternatives

- 3.2.1.2 Growing prevalence of acne, seborrheic dermatitis & scalp disorders

- 3.2.1.3 Regulatory push against synthetic preservatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Potential skin irritation & allergic reactions in sensitive populations

- 3.2.2.2 Higher cost compared to conventional synthetic preservatives

- 3.2.3 Market opportunities

- 3.2.3.1 Untapped potential in oral care & dental hygiene products

- 3.2.3.2 Expansion into pharmaceutical-grade wound care & medical topicals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Form, 2022 - 2035 (USD million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Powder Form (>90% Concentration)

- 5.3 Liquid/Aqueous Solution

Chapter 6 Market Estimates and Forecast, By Purity, 2022 - 2035 (USD million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Between 95%-98% Purity

- 6.3 Between 98%-99% Purity

- 6.4 99% and Above Purity

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Skin care

- 7.2.1 Anti-acne products

- 7.2.2 Anti-wrinkle & anti-aging products

- 7.2.3 Sebum control & oily skin treatment

- 7.2.4 Ph balancing & skin barrier restoration

- 7.2.5 Dermo-protective products

- 7.3 Hair care & scalp treatment

- 7.3.1 Anti-dandruff products

- 7.3.2 Anti-seborrheic products

- 7.3.3 Scalp soothing & irritation relief

- 7.3.4 Hair conditioning products

- 7.4 Antiperspirant & deodorant

- 7.4.1 Deodorant formulations

- 7.4.2 Antiperspirant products

- 7.5 Wound care & medical topicals

- 7.5.1 Wound dressings & healing products

- 7.5.2 Dermatological treatments

- 7.6 Oral care

- 7.6.1 Toothpaste formulations

- 7.6.2 Mouthwash & oral rinse products

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Specialty chemical distributors

- 8.4 Online b2b platforms

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Seppic

- 10.2 Scimplify

- 10.3 ATAMAn KIMYA

- 10.4 Pinpools GMBH

- 10.5 Euro-Kemical SRL

- 10.6 Sinerga S.p.A.

- 10.7 AE Chemie

- 10.8 DRAVYOM Chemical Company

- 10.9 DropBio

- 10.10 Uniproma

- 10.11 pecial Chem

- 10.12 Zley Group

- 10.13 Innospec Inc.

- 10.14 Minasolve

- 10.15 Euro-Kemical

- 10.16 Galaxy Surfactants

全球辛酰甘氨酸市场规模、份额、趋势和成长分析报告(2026-2034年)

全球辛酰甘氨酸市场规模、份额、趋势和成长分析报告(2026-2034年) 辛酰甘氨酸的全球市场全球马来西亚甘胺酸市场规模(依等级、最终用户、区域范围、预测)全球甘胺酸市场规模:按等级、最终用户和地区分類的范围和预测

辛酰甘氨酸的全球市场全球马来西亚甘胺酸市场规模(依等级、最终用户、区域范围、预测)全球甘胺酸市场规模:按等级、最终用户和地区分類的范围和预测