|

市场调查报告书

商品编码

1959578

单板计算机市场机会、成长要素、产业趋势分析及2026年至2035年预测。Single Board Computer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025 年全球单板计算机市场价值为 43 亿美元,预计到 2035 年将达到 73 亿美元,年复合成长率为 5.7%。

由于物联网设备在工业领域的应用日益广泛,市场正经历快速成长。随着企业将物联网融入运营,对紧凑、高效且功能多样的运算解决方案(例如单板电脑)的需求也在加速成长。教育机构和DIY计划也在推动这一成长,教育机构利用单板电脑教导学生程式设计、电子学和其他技术技能。单板计算机在培养新一代技术人才的同时,也创造了长期的市场机会。此外,人工智慧、机器视觉和边缘运算领域的应用也推动了市场需求,因为这些应用需要低延迟、高效能的即时数据处理能力。随着机器人、自主系统、安防和工业自动化的扩展,单板电脑正成为现代技术基础设施的关键基础。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 43亿美元 |

| 预测金额 | 73亿美元 |

| 复合年增长率 | 5.7% |

预计2035年,有线单板计算机(SBC)市场规模将达53亿美元。有线SBC因其高速、稳定的连接性能,以及在关键任务应用中确保不间断资料传输的能力,在工业和企业环境中日益受到青睐。这些闆卡在製造自动化、即时监控系统和工业IoT)网路中至关重要,因为即使是轻微的停机也会中断运作并危及安全。有线SBC在持续使用下的可靠性、抗干扰能力以及与现有有线网路的兼容性,使其成为在复杂系统中需要高精度、低延迟和稳定性能的领域的基础技术。

预计到2025年,基于ARM架构的单板电脑(SBC)市场份额将达到52.3%,其发展势头强劲,这得益于其高效的节能架构以及对人工智慧、嵌入式电脑和边缘运算的良好适应性。这些闆卡因其无风扇设计和紧凑的尺寸而备受青睐,使其能够在空间受限的环境中部署,同时又不牺牲性能。它们兼具低功耗和高运算效率,支援长时间运作,降低能源成本,是机器人、行动设备和自动化工业设备的理想选择。

预计到2025年,北美单板计算机(SBC)市占率将达到36.7%。该地区积极采用工业自动化、物联网整合和边缘运算解决方案,推动了对SBC的需求。企业和政府机构正依靠这些紧凑型运算系统进行即时数据采集、製程监控,并与现有工业网路无缝整合。先进的技术基础设施、强大的供应链以及对智慧製造和互联繫统的持续投资,正在巩固北美在SBC市场的领先地位,并使其成为创新和大规模部署的中心。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 物联网和边缘运算应用的快速普及

- 单板计算机 (SBC) 在教育和 DIY计划中的广泛应用

- 在人工智慧和机器视觉系统中的应用日益广泛

- 增加对国防和航太计画的投资

- 拓展教育与创客社区

- 产业潜在风险与挑战

- 供应链中断和零件短缺

- 与替代计算技术的竞争

- 市场机会

- 自动驾驶汽车和无人机领域的新兴应用

- 能源管理和智慧电网领域的机会

- 促进因素

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 专利和智慧财产权分析

- 地缘政治和贸易趋势

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 区域分布比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 2022-2025 年重大发展

- 併购

- 合作伙伴关係和合资企业

- 技术进步

- 扩张和投资策略

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估算与预测:依处理器架构划分,2022-2035年

- 基于ARM的单板计算机(SBC)

- 基于 x86/x64 的单板计算机

- 基于 RISC-V 的单板计算机

- 其他的

第六章 市场估算与预测:依记忆体配置划分,2022-2035年

- 2 GB RAM

- 2 GB~8 GB RAM

- 8 GB~16 GB RAM

- 16 GB~32 GB RAM

第七章 市场估算与预测:依连接介面划分,2022-2035年

- 有线SBC

- 工业现场汇流排通讯协定

- 标准乙太网路

- USB/串口

- 其他的

- 无线单板计算机

- Wi-Fi

- 细胞

- 其他的

第八章 市场估算与预测:依最终用途划分,2022-2035年

- 车

- 车载资讯娱乐和远端资讯处理

- 进阶驾驶辅助系统与自动驾驶系统

- 其他的

- 食品/饮料

- 流程自动化和控制

- 品质监控和安全系统

- 其他的

- 医疗保健

- 医疗设备及诊断设备

- 远端医疗和远距健康监测

- 其他的

- 国防、航太和公共

- 能源与公共产业

- 化学和製药製造

- 通讯与网路

- 其他的

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 主要企业

- Advantech Co., Ltd.

- Kontron AG

- Digi International Inc.

- Texas Instruments Incorporated

- 按地区分類的主要企业

- 北美洲

- Abaco Systems, Inc.

- Radisys Corporation

- IEI Integration Corp.

- 欧洲

- Congatec AG

- Eurotech SpA

- DFI Inc.(Diamond Flower Inc.)

- 亚太地区

- AAEON Technology Inc.

- ADLINK Technology Inc.

- ASUSTeK Computer Inc.

- 北美洲

- 特殊玩家/干扰者

- Raspberry Pi Foundation

- Axiomtek Co., Ltd.

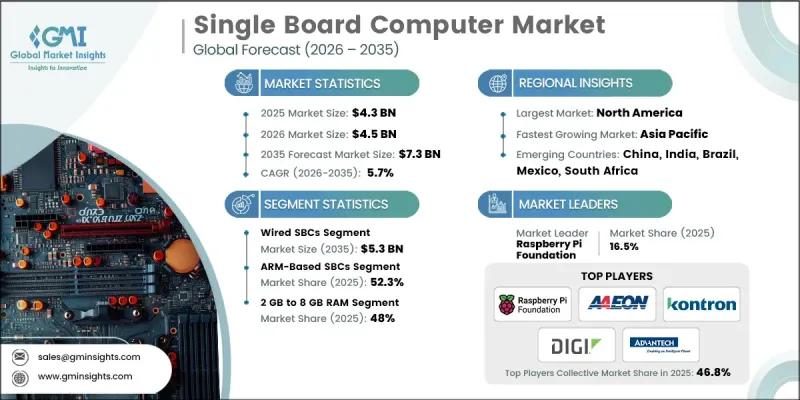

The Global Single Board Computer Market was valued at USD 4.3 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 7.3 billion by 2035.

The market is witnessing rapid expansion due to the rising adoption of IoT devices across industries. As businesses increasingly integrate IoT into operations, the demand for compact, efficient, and versatile computing solutions such as SBCs is accelerating. Educational and DIY projects are further supporting growth, with institutions using SBCs to train students in programming, electronics, and other tech skills. SBCs are shaping a new generation of tech-savvy individuals while creating long-term market opportunities. Additionally, the use of SBCs in AI, machine vision, and edge computing is fueling demand, as these applications require low-latency, high-performance computing capable of real-time data processing. As robotics, autonomous systems, security, and industrial automation expand, SBCs are becoming a critical backbone of modern technological infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.3 Billion |

| Forecast Value | $7.3 Billion |

| CAGR | 5.7% |

The wired SBC segment is projected to reach USD 5.3 billion by 2035. Wired SBCs are increasingly preferred in industrial and enterprise environments because they deliver high-speed, stable connectivity and ensure uninterrupted data transmission for mission-critical applications. These boards are essential for manufacturing automation, real-time monitoring systems, and industrial IoT networks, where even minimal downtime can disrupt operations or compromise safety. Their reliability under continuous use, resistance to interference, and compatibility with existing wired networks make them a cornerstone for sectors that demand precision, low latency, and consistent performance across complex systems.

The ARM-based SBC segment held a 52.3% share in 2025, gaining traction due to its power-efficient architecture and adaptability for AI, embedded computing, and edge processing. These boards are especially valued for fanless designs and compact footprints, allowing deployment in space-constrained environments without sacrificing performance. Their low power consumption, combined with high computational efficiency, supports long-term operation and reduces energy costs, making them ideal for robotics, mobile devices, and automated industrial equipment.

North America Single Board Computer Market contributed 36.7% share in 2025. The region's strong adoption of industrial automation, IoT integration, and edge computing solutions has propelled SBC demand. Enterprises and government agencies rely on these compact computing systems for real-time data acquisition, process monitoring, and seamless integration with existing industrial networks. Advanced technology infrastructure, robust supply chains, and ongoing investments in smart manufacturing and connected systems have reinforced North America's leadership in the Single Board Computer Market, positioning it as a hub for innovation and large-scale deployment.

Prominent players in the Global Single Board Computer Market include Advantech Co., Ltd., DFI Inc. (Diamond Flower Inc.), AAEON Technology Inc., Abaco Systems, Inc., ADLINK Technology Inc., ASUSTeK Computer Inc., Axiomtek Co., Ltd., Congatec AG, Digi International Inc., IEI Integration Corp., Eurotech S.p.A., Kontron AG, Radisys Corporation, Raspberry Pi Foundation, and Texas Instruments Incorporated. Key strategies adopted by companies in the Single Board Computer Market include expanding product portfolios to cover diverse applications from AI and industrial automation to education and embedded systems. Firms focus on enhancing processing power while maintaining energy efficiency and compact form factors. Companies invest heavily in R&D to develop specialized SBCs for edge computing, robotics, and AI workloads. Strategic partnerships, collaborations, and acquisitions are used to enter new markets and access innovative technologies. Manufacturers also emphasize reliability, high-speed connectivity, and long-term technical support to strengthen customer loyalty.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Processor architecture trends

- 2.2.2 Memory configuration trends

- 2.2.3 Connectivity interface trends

- 2.2.4 End-use application trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid adoption of IoT and edge computing applications

- 3.2.1.2 Widespread use of SBCs in educational and DIY projects

- 3.2.1.3 Rising utilization in AI and machine vision systems

- 3.2.1.4 Increasing investments in defense and aerospace programs

- 3.2.1.5 Expansion of educational and maker communities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain disruptions and component shortages

- 3.2.2.2 Competition from alternative computing technologies

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging applications in autonomous vehicles and drones

- 3.2.3.2 Opportunities in energy management and smart grids

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Processor Architecture, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 ARM-Based SBCs

- 5.3 x86 / x64-Based SBCs

- 5.4 RISC-V-Based SBCs

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Memory Configuration, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 2 GB RAM

- 6.3 2 GB to 8 GB RAM

- 6.4 8 GB to 16 GB RAM

- 6.5 16 GB to 32 GB RAM

Chapter 7 Market Estimates and Forecast, By Connectivity Interface, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Wired SBCs

- 7.2.1 Industrial fieldbus protocols

- 7.2.2 Standard ethernet

- 7.2.3 Usb / Serial

- 7.2.4 Others

- 7.3 Wireless SBCs

- 7.3.1 Wi-Fi

- 7.3.2 Cellular

- 7.3.3 Others

Chapter 8 Market Estimates and Forecast, By End-use Application, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Automotive

- 8.2.1 In-vehicle infotainment & telematics

- 8.2.2 ADAS & autonomous driving systems

- 8.2.3 Others

- 8.3 Food & beverage

- 8.3.1 Process automation & control

- 8.3.2 Quality monitoring & safety systems

- 8.3.3 Others

- 8.4 Medical & healthcare

- 8.4.1 Medical devices & diagnostics

- 8.4.2 Telemedicine & remote health monitoring

- 8.4.3 Others

- 8.5 Defense, aerospace & public safety

- 8.6 Energy & utilities

- 8.7 Chemical & pharmaceutical manufacturing

- 8.8 Telecommunications & networking

- 8.9 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Advantech Co., Ltd.

- 10.1.2 Kontron AG

- 10.1.3 Digi International Inc.

- 10.1.4 Texas Instruments Incorporated

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 Abaco Systems, Inc.

- 10.2.1.2 Radisys Corporation

- 10.2.1.3 IEI Integration Corp.

- 10.2.2 Europe

- 10.2.2.1 Congatec AG

- 10.2.2.2 Eurotech S.p.A.

- 10.2.2.3 DFI Inc. (Diamond Flower Inc.)

- 10.2.3 APAC

- 10.2.3.1 AAEON Technology Inc.

- 10.2.3.2 ADLINK Technology Inc.

- 10.2.3.3 ASUSTeK Computer Inc.

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Raspberry Pi Foundation

- 10.3.2 Axiomtek Co., Ltd.