|

市场调查报告书

商品编码

1959580

玻璃纤维增强塑胶管道市场机会、成长要素、产业趋势分析及预测(2026-2035年)Glass Reinforced Plastic (GRP) Piping Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

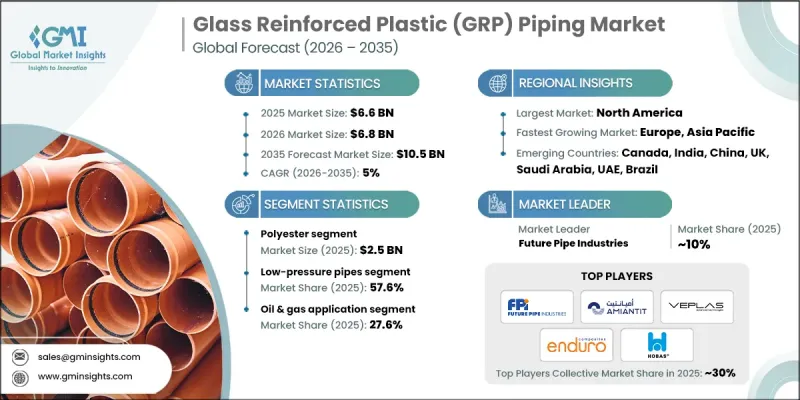

2025 年全球玻璃纤维增强塑胶 (GRP) 管道市场价值为 66 亿美元,预计到 2035 年将达到 105 亿美元,年复合成长率为 5%。

市场成长主要得益于玻璃钢(GRP)管道在需要高耐腐蚀性、耐久性和低维护成本的行业中日益普及。在石油天然气、化学和水资源管理等行业,由于玻璃钢管道相比传统的钢管和混凝土管道系统具有更长的使用寿命、更强的耐化学腐蚀性和更低的运营成本,其应用范围正在不断扩大。玻璃钢管道即使在恶劣的环境条件下也能保持高耐久性,并最大限度地降低生命週期成本,使其成为寻求永续和耐用基础设施解决方案的行业的理想选择。快速的都市化和市政基础设施的扩张,尤其是在发展中地区,正在推动供水、污水处理和灌溉网路对玻璃钢管道的需求。该材料长期性能稳定和永续性优势,以及政府和私人企业为寻求长期可靠性而采用玻璃钢解决方案,共同推动了这一趋势。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 66亿美元 |

| 预测金额 | 105亿美元 |

| 复合年增长率 | 5% |

预计到2025年,聚酯玻璃钢管道市场规模将达到25亿美元,并在2035年之前以5.2%的复合年增长率成长。这些管道因其卓越的耐腐蚀性而备受青睐,是供水、污水处理、灌溉和工业化学品应用的理想选择。与环氧树脂和乙烯基酯类管道相比,聚酯管道具有成本效益,因此在对成本高度敏感且兼顾可靠性和效率的市场中,聚酯管道被广泛应用于大规模计划和计划中。

预计到2025年,石油和天然气产业将占据27.6%的市场份额,并在2026年至2035年间以4.8%的复合年增长率成长。玻璃纤维(GRP)管道具有使用寿命长、耐腐蚀、维护成本低等优点,因此适用于输油管线、注水系统、生产水处理和炼油厂作业。随着企业扩大探勘、升级老旧基础设施并追求营运效率,对能够减少停机时间和降低生命週期成本的玻璃钢解决方案的需求持续增长。

预计到2025年,北美玻璃纤维增强塑胶(GRP)管道市场规模将达到12亿美元。美国大量老化的管道需要更换,而GRP管道因其使用寿命长、耐腐蚀、维护成本低等优点,成为理想的解决方案。石油天然气、化学和可再生能源产业的投资不断增长,推动了对能够支持永续营运并能承受严苛环境的管道技术的需求。监管机构对环境法规和效率的日益重视,也进一步加速了环保GRP材料的应用。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 对耐腐蚀和低维护材料的需求不断增长

- 都市化以及对水和污水处理日益增长的需求

- 基础建设和老旧系统的更换

- 产业潜在风险与挑战

- 全球贸易不确定性和关税波动的影响

- 高昂的初始资本成本和安装成本

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依产品类型

- 监理情势

- 标准和合规要求

- 区域法规结构

- 认证标准

- 贸易统计

- 主要进口国

- 主要出口国

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 环氧树脂

- 聚酯纤维

- 乙烯基酯类

- 其他的

第六章 市场估价与预测:依製造流程划分,2022-2035年

- 缠绕成型

- 树脂注射成型(RTM)

- 离心铸造

第七章 市场估计与预测:依压力等级划分,2022-2035年

- 低压管道

- 高压管道

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 石油和天然气

- 化学品

- 污水处理

- 灌溉

- 供水

- 其他行业(造纸和纸浆製造、发电、采矿等)

第九章 市场估价与预测:依通路划分,2022-2035年

- 直接地

- 间接

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 印尼

- 马来西亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

第十一章:公司简介

- Composite Pipes Industry

- Dubai Pipes Factory

- Enduro Composites

- Fibrex

- Future Pipe Industries

- Graphite India Limited

- Hanwei Energy Services Corp.

- Harwal Group

- HOBAS

- Industrial Plastic Systems

- Plasticon Composites

- Sarplast

- Saudi Arabian Amiantit Company

- Smithline Reinforced Composites

- Veplas dd

The Global Glass Reinforced Plastic Piping Market was valued at USD 6.6 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 10.5 billion by 2035.

Market growth is driven by the rising adoption of GRP piping across industries that demand highly corrosion-resistant, durable, and low-maintenance materials. Sectors such as oil and gas, chemicals, and water management are increasingly using GRP due to its longer service life, chemical resistance, and lower operational costs compared to traditional steel or concrete systems. GRP piping also offers resilience under extreme environmental conditions while minimizing lifecycle costs, making it an attractive choice for industries seeking sustainable and durable infrastructure solutions. Rapid urbanization and expanding municipal infrastructure, particularly in developing regions, are fueling demand for GRP pipes in water distribution, sewage management, and irrigation networks. The material's performance stability over time, combined with its sustainability benefits, is encouraging governments and private enterprises to adopt GRP solutions for long-term reliability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.6 Billion |

| Forecast Value | $10.5 Billion |

| CAGR | 5% |

The polyester-based GRP pipes segment accounted for USD 2.5 billion in 2025 and is expected to grow at a CAGR of 5.2% through 2035. These pipes are favored for their excellent corrosion resistance, making them ideal for water, sewage, irrigation, and industrial chemical applications. Polyester variants are cost-effective compared to epoxy and vinyl ester alternatives, driving their adoption in large-scale municipal and infrastructure projects, particularly in cost-sensitive markets seeking both reliability and efficiency.

The oil & gas segment held a 27.6% share in 2025 and is projected to grow at a CAGR of 4.8% during 2026-2035. GRP pipes provide long service life, corrosion resistance, and low maintenance requirements, making them suitable for flowlines, water injection systems, produced water handling, and refinery operations. As companies expand exploration, replace aging infrastructure, and seek operational efficiency, the demand for GRP solutions that reduce downtime and total lifecycle costs continues to rise.

North America Glass Reinforced Plastic (GRP) Piping Market was valued at USD 1.2 billion in 2025. Widespread aging pipelines in the U.S. require replacement with materials that provide longevity, corrosion resistance, and lower maintenance costs, positioning GRP pipes as a preferred solution. Increased investments across oil and gas, chemical processing, and renewable energy sectors are boosting demand for piping technologies that withstand harsh conditions while supporting sustainable operations. Regulatory focus on environmental compliance and efficiency further accelerates the adoption of eco-friendly GRP materials.

Key players in the Global Glass Reinforced Plastic Piping Market include Enduro Composites, Future Pipe Industries, Smithline Reinforced Composites, Veplas d.d., Industrial Plastic Systems, Plasticon Composites, Composite Pipes Industry, Dubai Pipes Factory, Graphite India Limited, Sarplast, HOBAS, Hanwei Energy Services Corp., Saudi Arabian Amiantit Company, and Fibrex. Companies in the Glass Reinforced Plastic Piping Market are pursuing multiple strategies to strengthen their foothold. They are investing in R&D to develop high-performance, corrosion-resistant, and lightweight pipes suitable for extreme conditions and specialized applications. Strategic partnerships with municipal authorities, industrial clients, and engineering firms allow for early adoption and integration of advanced piping systems. Expanding manufacturing capabilities and localizing production help reduce lead times and logistical costs while meeting regional demand. Firms are also emphasizing sustainable and eco-friendly materials to align with regulatory standards and environmental goals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Manufacturing process

- 2.2.4 Application

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for corrosion-resistant & low-maintenance materials

- 3.2.1.2 Urbanization and growing water & wastewater needs

- 3.2.1.3 Infrastructure development & replacement of aging systems

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Impact of global trade uncertainties & tariff fluctuations

- 3.2.2.2 High initial capital costs & installation expenses

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Epoxy

- 5.3 Polyester

- 5.4 Vinyl ester

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Manufacturing Process, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Filament winding

- 6.3 Resin transfer molding (RTM)

- 6.4 Centrifugal casting

Chapter 7 Market Estimates & Forecast, By Pressure Rating, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low-pressure pipes

- 7.3 High-pressure pipes

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Oil & gas

- 8.3 Chemicals

- 8.4 Wastewater treatment

- 8.5 Irrigation

- 8.6 Water supply

- 8.7 Others (pulp & paper, power generation, mining, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Composite Pipes Industry

- 11.2 Dubai Pipes Factory

- 11.3 Enduro Composites

- 11.4 Fibrex

- 11.5 Future Pipe Industries

- 11.6 Graphite India Limited

- 11.7 Hanwei Energy Services Corp.

- 11.8 Harwal Group

- 11.9 HOBAS

- 11.10 Industrial Plastic Systems

- 11.11 Plasticon Composites

- 11.12 Sarplast

- 11.13 Saudi Arabian Amiantit Company

- 11.14 Smithline Reinforced Composites

- 11.15 Veplas d.d.

纤维增强塑胶市场:依纤维类型、树脂类型和终端用户产业划分-2026-2032年全球预测

纤维增强塑胶市场:依纤维类型、树脂类型和终端用户产业划分-2026-2032年全球预测 FRP管材市场报告:按类型、製造流程、应用和地区划分(2026-2034年)FRP货柜市场:按货柜类型、製造流程和应用划分-2026-2032年全球市场预测FRP储槽市场:按类型、容量、製造流程、材质等级、应用和最终用户划分-2026-2032年全球市场预测FRP桥樑市场:按桥樑类型、纤维类型、树脂类型、组件和应用划分-2026-2032年全球市场预测FRP格栅市场:2026-2032年全球市场预测(依成型製程、树脂类型、应用及终端用户产业划分)

FRP管材市场报告:按类型、製造流程、应用和地区划分(2026-2034年)FRP货柜市场:按货柜类型、製造流程和应用划分-2026-2032年全球市场预测FRP储槽市场:按类型、容量、製造流程、材质等级、应用和最终用户划分-2026-2032年全球市场预测FRP桥樑市场:按桥樑类型、纤维类型、树脂类型、组件和应用划分-2026-2032年全球市场预测FRP格栅市场:2026-2032年全球市场预测(依成型製程、树脂类型、应用及终端用户产业划分) 2026年全球FRP储槽市场报告2026年全球FRP容器市场报告2026年全球玻璃纤维增强塑胶(GRP)管道市场报告2026年全球纤维增强塑胶容器市场报告

2026年全球FRP储槽市场报告2026年全球FRP容器市场报告2026年全球玻璃纤维增强塑胶(GRP)管道市场报告2026年全球纤维增强塑胶容器市场报告