|

市场调查报告书

商品编码

1959581

光学感测器市场机会、成长要素、产业趋势分析及2026年至2035年预测Optical Sensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

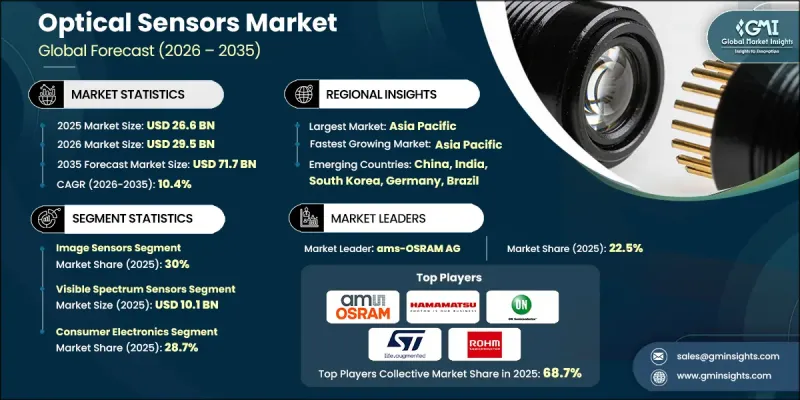

2025 年全球光学感测器市场价值为 266 亿美元,预计到 2035 年将达到 717 亿美元,年复合成长率为 10.4%。

穿戴式健康监测设备中光学感测器的日益普及,以及其在医学成像和诊断领域应用的不断增长,推动了市场扩张。此外,工业和商业设施对精确环境和气体监测的需求,以及基于光电感测技术实现自动化、品质检测和安全合规的智慧工厂的发展,也支撑了市场需求。光纤感测技术凭藉其远距离和高灵敏度的测量能力,在能源和基础设施监测领域也备受关注。预计从2020年起,在电网现代化和可再生能源扩张的推动下,这一趋势将加速发展,并持续到2030年。这是因为电力公司正致力于即时故障检测、结构健康监测以及减少停机时间和维护风险。在受监管行业,标准化和安全标准的合规性正日益影响部署策略,从而提升互通性、加快核准流程,并增强人们对光学感测技术的信心。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 266亿美元 |

| 预测金额 | 717亿美元 |

| 复合年增长率 | 10.4% |

预计到2025年,影像感测器市场份额将达到30%,在包括家用电子电器、汽车摄影机系统、工业机器视觉和医学成像在内的众多应用领域中保持主导地位。影像感测器对于需要高精度和即时视觉智慧的应用至关重要,因为它们能够提供高解析度视觉数据,支援人工智慧驱动的分析,并能与数位处理平台无缝整合。

预计到 2025 年,可见频谱感测器市场规模将达到 101 亿美元。由于这些感测器与标准成像系统相容、生产效率高且成本效益好,并且能够适应家用电子电器、工业检测和机器视觉系统等大规模应用,因此它们的需求仍然强劲。

预计到2025年,北美光学感测器市场份额将达到27%。这一区域成长主要得益于高阶驾驶辅助系统(ADAS)、医疗诊断和工业製造自动化等技术的日益普及。汽车、半导体和医疗设备产业的需求最为强劲,加速了高精度影像感测器、光达(LiDAR)和光电感测器的应用。政府和私人公司对智慧运输、数位医疗和工业4.0等倡议的投资也推动了市场成长,因为这些计划需要依赖光学感测器进行精确的即时数据采集和製程控制。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 扩大ADAS和LiDAR在乘用车中的集成

- 在穿戴式健康监测设备的应用范围扩大

- 光学感测技术在医学诊断与影像学的应用

- 对精确的环境和气体监测系统的需求

- 利用光电感测技术的智慧工厂发展

- 产业潜在风险与挑战

- 高精度应用的高成本校准和调整。

- 与低成本MEMS和电容式感测器的竞争

- 市场机会

- 用于非侵入性疾病诊断的光学生物感测器

- 工业安全法规促进了机器视觉感测器的发展。

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 定价策略

- 新兴经营模式

- 合规要求

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线广度

- 科技

- 创新

- 地理位置比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 主要进展

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张和投资策略

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 分离式检测器

- 光电接近感测器

- 光纤感测器

- 影像感测器

- 主动测距感测器模组

- 其他的

第六章 市场估算与预测:依输出讯号类型划分,2022-2035年

- 类比输出感测器

- 数位输出感测器

- 混合型和可配置输出感测器

第七章 市场估计与预测:依频谱范围划分,2022-2035年

- 紫外线 (UV) 感测器

- 可见频谱感测器

- 红外线(IR)感测器

- 宽频多频谱感测器

第八章 市场估算与预测:依最终用途产业划分,2022-2035年

- 车

- 工业的

- 家用电子电器

- 电讯

- 医疗保健系统

- 航太/国防

- 其他的

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 主要企业

- ams-OSRAM AG

- STMicroelectronics NV

- Sony Group Corporation

- Texas Instruments Incorporated

- Honeywell International Inc.

- Panasonic Corporation

- 按地区分類的主要企业

- 北美洲

- ON Semiconductor Corp.

- Broadcom Inc.

- Vishay Intertechnology, Inc.

- TE Connectivity Ltd.

- 亚太地区

- Hamamatsu Photonics KK

- Keyence Corporation

- ROHM Co., Ltd.

- 欧洲

- SICK AG

- Jenoptik AG

- 北美洲

- 特殊玩家/干扰者

- SiLC Technologies, Inc.

- Rockley Photonics Holdings Ltd.

The Global Optical Sensors Market was valued at USD 26.6 billion in 2025 and is estimated to grow at a CAGR of 10.4% to reach USD 71.7 billion by 2035.

The market expansion is driven by the rising adoption of optical sensors in wearable health monitoring devices, coupled with their increasing use in imaging and medical diagnostic applications. Demand is further supported by the need for precise environmental and gas monitoring in industrial and commercial operations, along with the growth of smart factories that rely on photoelectric sensing for automation, quality inspection, and safety compliance. Fiber-optic sensing is also gaining traction in energy and infrastructure monitoring, offering long-distance, high-sensitivity measurement capabilities. This trend accelerated after 2020 with grid modernization and the expansion of renewable energy, and it is expected to continue through 2030, as utilities focus on real-time fault detection, structural health monitoring, and reducing downtime and maintenance risks. Standardization and safety compliance are increasingly shaping adoption strategies in regulated sectors, driving interoperability, faster approvals, and trust in optical sensing technologies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $26.6 Billion |

| Forecast Value | $71.7 Billion |

| CAGR | 10.4% |

The image sensors segment held 30% share in 2025, leading due to its wide application in consumer electronics, automotive camera systems, industrial machine vision, and medical imaging. Image sensors provide high-resolution visual data, support AI-driven analytics, and integrate seamlessly with digital processing platforms, making them essential for applications requiring precision and real-time visual intelligence.

The visible spectrum sensors segment reached USD 10.1 billion in 2025. These sensors remain in strong demand due to compatibility with standard imaging systems, cost-effective production, and suitability for large-scale applications across consumer electronics, industrial inspection, and machine vision systems.

North America Optical Sensors Market accounted for 27% share in 2025. Growth in this region is fueled by rising adoption of advanced driver assistance systems, healthcare diagnostics, and automation in industrial manufacturing. Demand is strongest in the automotive, semiconductor, and medical device sectors, driving deployment of high-precision image sensors, LiDAR, and photoelectric sensors. Investments by governments and private companies in smart mobility, digital healthcare, and Industry 4.0 initiatives are also boosting market growth, as these projects depend on optical sensors for accurate, real-time data acquisition and process control.

Prominent players in the Global Optical Sensors Market include Keyence Corporation, Panasonic Corporation, Broadcom Inc., ams-OSRAM AG, Texas Instruments Incorporated, SICK AG, Honeywell International Inc., ROHM Co., Ltd., Sony Group Corporation, Jenoptik AG, ON Semiconductor Corp., Rockley Photonics Holdings Ltd., TE Connectivity Ltd., SiLC Technologies, Inc., Hamamatsu Photonics K.K., and STMicroelectronics N.V. Key strategies adopted by optical sensor companies include expanding product portfolios to cover diverse applications, from automotive and industrial to medical devices. Firms focus on high-precision and energy-efficient solutions while emphasizing interoperability with existing systems. Companies invest in R&D to develop next-generation sensors with higher sensitivity, smaller form factors, and AI integration. Strategic partnerships, collaborations, and mergers help access new markets and technologies. Market leaders optimize manufacturing capabilities to meet high-volume demand and reduce costs. Emphasis on regulatory compliance, certifications, and standardization improves adoption in critical sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Output signal type trends

- 2.2.3 Spectral range trends

- 2.2.4 End-use Industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising ADAS and LiDAR integration in passenger vehicles

- 3.2.1.2 Expanding use in wearable health monitoring devices

- 3.2.1.3 Optical sensing adoption in medical diagnostics and imaging

- 3.2.1.4 Demand for precise environmental and gas monitoring systems

- 3.2.1.5 Growth of smart factories using photoelectric sensing

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High calibration and alignment costs for precision applications

- 3.2.2.2 Competition from low-cost MEMS and capacitive sensors

- 3.2.3 Market opportunities

- 3.2.3.1 Optical biosensors for non-invasive disease diagnostics

- 3.2.3.2 Industrial safety compliance driving machine-vision sensors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Discrete photodetectors

- 5.3 Photoelectric proximity sensors

- 5.4 Fiber optic sensors

- 5.5 Image sensors

- 5.6 Active ranging sensor modules

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Output Signal Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Analog output sensors

- 6.3 Digital output sensors

- 6.4 Hybrid & configurable output sensors

Chapter 7 Market Estimates and Forecast, By Spectral Range, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Ultraviolet (UV) sensors

- 7.3 Visible spectrum sensors

- 7.4 Infrared (IR) sensors

- 7.5 Broadband & multi-spectral sensors

Chapter 8 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Industrial

- 8.4 Consumer Electronics

- 8.5 Telecommunications

- 8.6 Healthcare Systems

- 8.7 Aerospace & Defense

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 ams-OSRAM AG

- 10.1.2 STMicroelectronics N.V.

- 10.1.3 Sony Group Corporation

- 10.1.4 Texas Instruments Incorporated

- 10.1.5 Honeywell International Inc.

- 10.1.6 Panasonic Corporation

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 ON Semiconductor Corp.

- 10.2.1.2 Broadcom Inc.

- 10.2.1.3 Vishay Intertechnology, Inc.

- 10.2.1.4 TE Connectivity Ltd.

- 10.2.2 Asia Pacific

- 10.2.2.1 Hamamatsu Photonics K.K.

- 10.2.2.2 Keyence Corporation

- 10.2.2.3 ROHM Co., Ltd.

- 10.2.3 Europe

- 10.2.3.1 SICK AG

- 10.2.3.2 Jenoptik AG

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 SiLC Technologies, Inc.

- 10.3.2 Rockley Photonics Holdings Ltd.

2026年全球光学感测器市场报告

2026年全球光学感测器市场报告 3D彩色共聚焦感测器市场:按产品、应用和最终用户划分-2026-2032年全球预测奈米级共聚焦色差感测器市场:按产品类型、销售管道、终端用户产业和应用划分-2026-2032年全球预测线型色散共焦感测器市场:按产品类型、雷射波长、测量范围、应用和最终用户产业划分-2026-2032年全球预测

3D彩色共聚焦感测器市场:按产品、应用和最终用户划分-2026-2032年全球预测奈米级共聚焦色差感测器市场:按产品类型、销售管道、终端用户产业和应用划分-2026-2032年全球预测线型色散共焦感测器市场:按产品类型、雷射波长、测量范围、应用和最终用户产业划分-2026-2032年全球预测 光学感测器市场分析及预测(至2035年):按类型、产品类型、技术、组件、应用、材料类型、装置及最终用户划分

光学感测器市场分析及预测(至2035年):按类型、产品类型、技术、组件、应用、材料类型、装置及最终用户划分 全球光学感测器市场:按类型、感测器类别、应用和地区划分-市场规模、产业趋势、机会分析和未来预测(2026-2035 年)

全球光学感测器市场:按类型、感测器类别、应用和地区划分-市场规模、产业趋势、机会分析和未来预测(2026-2035 年) 光学感测市场-全球产业规模、份额、趋势、机会及预测(按类型、方法、操作、技术、最终用途、地区和竞争格局划分,2021-2031年)

光学感测市场-全球产业规模、份额、趋势、机会及预测(按类型、方法、操作、技术、最终用途、地区和竞争格局划分,2021-2031年) 全球光学感测器市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析、未来预测(2026-2034)按产品类型、解析度、技术、安装位置、价格范围、连接方式、性别、最终用户和分销管道分類的角落摄影机市场—2026-2032年全球预测液态聚焦镜头市场:依技术、应用、最终用户和通路划分,全球预测(2026-2032年)

全球光学感测器市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析、未来预测(2026-2034)按产品类型、解析度、技术、安装位置、价格范围、连接方式、性别、最终用户和分销管道分類的角落摄影机市场—2026-2032年全球预测液态聚焦镜头市场:依技术、应用、最终用户和通路划分,全球预测(2026-2032年)