|

市场调查报告书

商品编码

1959585

瓦楞纸箱市场机会、成长要素、产业趋势分析及2026年至2035年预测。Corrugated Boxes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

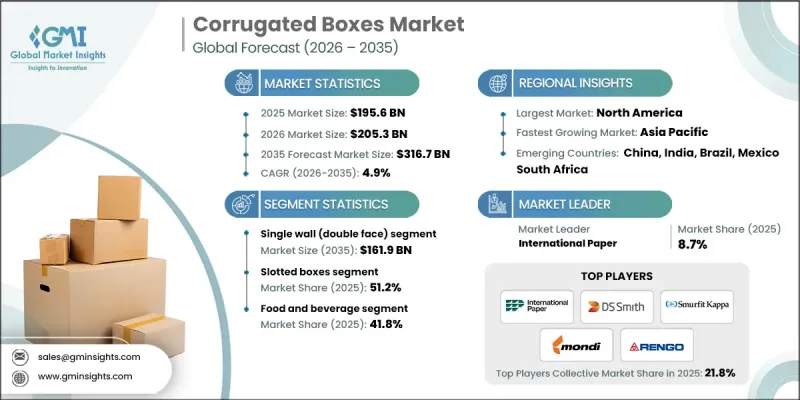

2025年全球瓦楞纸箱市值为1,956亿美元,预计2035年将达到3,167亿美元,年复合成长率为4.9%。

该市场的快速扩张主要得益于电子商务和线上零售的蓬勃发展,从而催生了对可靠、耐用且经济高效的包装解决方案的需求。快速消费品(FMCG)消费量的成长,包括个人护理产品、家居用品以及食品饮料,进一步推动了对瓦楞纸箱的需求。企业日益意识到包装是一种策略行销工具,它不仅能够保护产品、优化存储,还能帮助品牌推广。QR码、NFC标籤和扩增实境(AR)等数位创新技术有助于提升消费者参与度和品牌知名度。轻盈而坚固的瓦楞纸板材料需求旺盛,因为它们既能降低运输成本和环境影响,又不影响产品保护。新兴地区的都市化和人均收入的成长正在推动快速消费品需求,进而促进全球瓦楞纸板包装产业的成长。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 1956亿美元 |

| 预测金额 | 3167亿美元 |

| 复合年增长率 | 4.9% |

预计2035年,单层(双面)单层双面瓦楞纸板箱兼具价格优势、强度和可回收性,市场需求不断增长。这类纸箱适用于轻量至中型产品,适合大规模生产,并可与自动化包装线相容。永续性和成本效益使其成为希望在保持营运效率的同时减少环境影响的製造商的理想选择。

预计2026年至2035年间,自动化组合式瓦楞纸箱市场将以5.2%的复合年增长率成长。企业正越来越多地采用自动化组合式瓦楞纸箱,以提高营运效率、减少对劳动力的依赖并加快包装流程。这些纸箱性能稳定、组装快捷,是电履约中心、餐饮服务业和自动化仓库的理想选择。自动化程度的不断提高以及对扩充性包装解决方案的需求是推动该市场成长的主要因素。

预计2025年,北美瓦楞纸箱市占率将达到28.5%。该地区拥有成熟的製造业基础、完善的基础设施和先进的物流网络。瓦楞纸箱因其耐用性、可回收性和产品保护能力而备受青睐。美国在该市场占据主导地位,这主要得益于零售、工业运输和消费品行业的需求。大规模生产系统、完善的供应链以及电子商务的日益普及,都推动了瓦楞纸包装解决方案在该地区广泛应用。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 电子商务和线上零售通路的成长

- 快速消费品(FMCG)产业的扩张

- 食品和饮料包装需求不断成长

- 从塑胶包装向纸质包装解决方案过渡

- 新兴市场的都市化与零售基础建设发展

- 产业潜在风险与挑战

- 原物料价格快速波动

- 大宗瓦楞纸箱运输和仓储成本高昂

- 市场机会

- 对永续和可生物降解包装解决方案的需求日益增长

- 智慧包装技术的应用日益广泛

- 促进因素

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 永续性措施

- 永续材料评价

- 碳足迹分析

- 引入循环经济

- 永续性认证和标准

- 永续性投资报酬率分析

- 全球消费者态度分析

- 专利分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 区域扩张比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年重大发展

- 併购

- 合作伙伴关係和合资企业

- 技术进步

- 扩张和投资策略

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估价与预测:依板材类型划分,2022-2035年

- 一边

- 单层(双面)

- 双层壁

- 三层壁

第六章 市场估价与预测:依包装盒样式划分,2022-2035年

- 狭缝盒

- 伸缩盒

- 文件夹盒

- 硬盒

- 自动组合式箱

- 内框架

第七章 市场估计与预测:依材料类型划分,2022-2035年

- 衬板

- 瓦楞芯纸

- 其他的

第八章 市场估算与预测:依印刷技术划分,2022-2035年

- 柔版印刷

- 数位印刷

- 胶印标籤/胶版印刷

- 其他的

第九章 市场估价与预测:依通路划分,2022-2035年

- 离线

- 在线的

第十章 市场估价与预测:依最终用途划分,2022-2035年

- 食品/饮料

- 电子商务和直接面向消费者的销售

- 电子设备和电气产品

- 製药和医疗保健

- 工业/製造产品

- 汽车及车辆零件

- 其他的

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- 主要企业

- International Paper

- DS Smith

- Smurfit Kappa

- Mondi

- 按地区分類的主要企业

- 北美洲

- Packaging Corporation of America

- Cascades Inc.

- Visy

- 欧洲

- Rengo Co., Ltd.

- GB Pack

- Lee &Man Paper Manufacturing Ltd

- 亚太地区

- Nine Dragons Worldwide(China)Investment Group Co., Ltd.

- TGI Packaging Pvt. Ltd

- Natraj Industries

- 北美洲

- 特殊玩家/干扰者

- Dongguang Ruichang Carton Machinery

- Shanghai PrintYoung International Industry

- Shengli Carton Equipment Manufacturing

- NBM Pack

- Pretoria Box Manufacturers(Pty)Ltd

- XINTIAN CARTON MACHINERY MANUFACTURING

- Zemat Technology Group

The Global Corrugated Boxes Market was valued at USD 195.6 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 316.7 billion by 2035.

The market is expanding rapidly, driven primarily by the surge in e-commerce and online retail, which demands reliable, durable, and cost-efficient packaging solutions. Rising consumption of FMCG products, including personal care, household goods, and food & beverages, is further fueling the need for corrugated boxes. Businesses increasingly recognize packaging as a strategic marketing tool that protects products, optimizes storage, and enables branding. Digital innovations, including QR codes, NFC tags, and augmented reality features, are enhancing consumer engagement and brand visibility. Lightweight yet strong corrugated materials are gaining preference, as they reduce shipping costs and environmental impact without compromising product protection. Urbanization and rising per capita income in emerging regions are driving FMCG demand, which in turn strengthens the global corrugated packaging sector.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $195.6 Billion |

| Forecast Value | $316.7 Billion |

| CAGR | 4.9% |

The single wall (double face) segment is projected to reach USD 161.9 billion by 2035. Demand for single wall double face corrugated boxes is rising due to their optimal balance of affordability, strength, and recyclability. These boxes are ideal for lightweight to medium-weight products, support high-volume production, and are compatible with automated packaging lines. Their sustainability and cost-effectiveness make them the preferred choice for manufacturers aiming to reduce environmental impact while maintaining operational efficiency.

The self-erecting boxes segment is expected to grow at a CAGR of 5.2% between 2026 and 2035. Companies are increasingly adopting self-erecting boxes to enhance operational efficiency, reduce labor dependency, and accelerate packing processes. These boxes allow consistent performance and faster assembly, making them highly suitable for e-commerce fulfillment centers, foodservice operations, and automated warehouses. The increasing adoption of automation and demand for scalable packaging solutions are major factors driving growth in this segment.

North America Corrugated Boxes Market held a 28.5% share in 2025. The region benefits from a mature manufacturing base, robust infrastructure, and advanced logistics networks. Corrugated boxes are preferred for their durability, recyclability, and product protection capabilities. The United States dominates this market, driven by demand from retail, industrial shipping, and consumer goods sectors. High-volume production, sophisticated supply chains, and growing e-commerce penetration contribute to the strong adoption of corrugated packaging solutions in the region.

Key players operating in the Global Corrugated Boxes Market include DS Smith, Smurfit Westrock, Mondi, Acme Machinery, Fosber Group, Packaging Corporation of America, Bohui Group, DING SHUNG MACHINERY, Dongguang Ruichang Carton Machinery, International Paper, Lee & Man Paper Manufacturing Ltd, Natraj Industries, NBM Pack, GB Pack, Nine Dragons Worldwide (China) Investment Group Co., Ltd., Packsize International, National Carton Factory (NCF), Pretoria Box Manufacturers (Pty) Ltd, Rengo Co. Ltd, Shanghai PrintYoung International Industry, and Shengli Carton Equipment Manufacturing. Companies in the corrugated boxes market are pursuing multiple strategies to strengthen their presence and market share. They are investing in R&D to develop lightweight, high-strength, and sustainable corrugated materials. Collaboration with e-commerce, FMCG, and industrial players allows for customized packaging solutions that meet specific operational and branding needs. Many are integrating smart packaging technologies such as QR codes, AR, and NFC to enhance consumer engagement and drive brand differentiation. Expansion of production facilities and global distribution networks ensures faster delivery and wider market reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Board type trends

- 2.2.2 Box style trends

- 2.2.3 Material type trends

- 2.2.4 Printing technology trends

- 2.2.5 Distribution channel trends

- 2.2.6 End use application trends

- 2.2.7 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in E-commerce and online retail channels

- 3.2.1.2 Expansion of fast moving consumer goods (FMCG) sector

- 3.2.1.3 Growth in food and beverage packaging requirements

- 3.2.1.4 Shift from plastic to paper-based packaging solutions

- 3.2.1.5 Emerging market urbanization and retail infrastructure development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High raw material price volatility

- 3.2.2.2 High transportation and storage costs for bulk corrugated boxes

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for sustainable and biodegradable packaging solutions

- 3.2.3.2 Increasing adoption of smart and intelligent packaging technologies

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging Business Models

- 3.8 Compliance Requirements

- 3.9 Sustainability Measures

- 3.9.1 Sustainable Materials Assessment

- 3.9.2 Carbon Footprint Analysis

- 3.9.3 Circular Economy Implementation

- 3.9.4 Sustainability Certifications and Standards

- 3.9.5 Sustainability ROI Analysis

- 3.10 Global Consumer Sentiment Analysis

- 3.11 Patent Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Board Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Single face

- 5.3 Single wall (double face)

- 5.4 Double wall

- 5.5 Triple wall

Chapter 6 Market Estimates and Forecast, By Box Style, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Slotted boxes

- 6.3 Telescope boxes

- 6.4 Folder boxes

- 6.5 Rigid boxes

- 6.6 Self-erecting boxes

- 6.7 Interior forms

Chapter 7 Market Estimates and Forecast, By Material Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Linerboard

- 7.3 Medium

- 7.4 Others

Chapter 8 Market Estimates and Forecast, By Printing Technology, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Flexographic printing

- 8.3 Digital printing

- 8.4 Litho-label / offset printing

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Offline

- 9.3 Online

Chapter 10 Market Estimates and Forecast, By End-Use Application, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Food & beverage

- 10.3 E-commerce & direct-to-consumer

- 10.4 Electronics & electrical goods

- 10.5 Pharmaceuticals & healthcare

- 10.6 Industrial & manufacturing goods

- 10.7 Automotive & vehicle parts

- 10.8 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 International Paper

- 12.1.2 DS Smith

- 12.1.3 Smurfit Kappa

- 12.1.4 Mondi

- 12.2 Regional Key Players

- 12.2.1 North America

- 12.2.1.1 Packaging Corporation of America

- 12.2.1.2 Cascades Inc.

- 12.2.1.3 Visy

- 12.2.2 Europe

- 12.2.2.1 Rengo Co., Ltd.

- 12.2.2.2 GB Pack

- 12.2.2.3 Lee & Man Paper Manufacturing Ltd

- 12.2.3 APAC

- 12.2.3.1 Nine Dragons Worldwide (China) Investment Group Co., Ltd.

- 12.2.3.2 TGI Packaging Pvt. Ltd

- 12.2.3.3 Natraj Industries

- 12.2.1 North America

- 12.3 Niche Players / Disruptors

- 12.3.1 Dongguang Ruichang Carton Machinery

- 12.3.2 Shanghai PrintYoung International Industry

- 12.3.3 Shengli Carton Equipment Manufacturing

- 12.3.4 NBM Pack

- 12.3.5 Pretoria Box Manufacturers (Pty) Ltd

- 12.3.6 XINTIAN CARTON MACHINERY MANUFACTURING

- 12.3.7 Zemat Technology Group

瓦楞纸箱市场分析及预测(至2035年):类型、产品类型、应用、材质类型、技术、最终用户、功能、製造流程、组件

瓦楞纸箱市场分析及预测(至2035年):类型、产品类型、应用、材质类型、技术、最终用户、功能、製造流程、组件 全球可重复使用瓦楞塑胶盒市场规模、份额、趋势和成长分析报告(2026-2034年)

全球可重复使用瓦楞塑胶盒市场规模、份额、趋势和成长分析报告(2026-2034年) 瓦楞纸箱市场规模、份额、趋势及预测(按材料、最终用途和地区划分),2026-2034年

瓦楞纸箱市场规模、份额、趋势及预测(按材料、最终用途和地区划分),2026-2034年 2026年全球带瓦楞纸箱市场报告

2026年全球带瓦楞纸箱市场报告 瓦楞纸箱市场 - 全球产业规模、份额、趋势、机会及预测(按类型、材料、印刷油墨、地区和竞争格局划分,2021-2031年)

瓦楞纸箱市场 - 全球产业规模、份额、趋势、机会及预测(按类型、材料、印刷油墨、地区和竞争格局划分,2021-2031年) 模切折迭盒市场按类型、材料类型、印刷技术、最终用途产业和分销管道划分,全球预测(2026-2032年)

模切折迭盒市场按类型、材料类型、印刷技术、最终用途产业和分销管道划分,全球预测(2026-2032年) 瓦楞纸箱市场规模、份额和成长分析(按材料、印刷油墨、印刷技术、类型、最终用户产业和地区划分)—产业预测(2026-2033 年)

瓦楞纸箱市场规模、份额和成长分析(按材料、印刷油墨、印刷技术、类型、最终用户产业和地区划分)—产业预测(2026-2033 年) 瓦楞纸箱市场预测至2032年:全球分析(按纸箱类型、壁厚类型、瓦楞类型、材料类型、印刷技术、最终用户和地区划分)瓦楞纸箱市场按类型、材料来源、瓦楞类型、设计类型、印刷技术和最终用户划分-2025-2032 年全球预测

瓦楞纸箱市场预测至2032年:全球分析(按纸箱类型、壁厚类型、瓦楞类型、材料类型、印刷技术、最终用户和地区划分)瓦楞纸箱市场按类型、材料来源、瓦楞类型、设计类型、印刷技术和最终用户划分-2025-2032 年全球预测 全球可重复使用塑胶瓦楞纸箱市场

全球可重复使用塑胶瓦楞纸箱市场