|

市场调查报告书

商品编码

1959600

指纹认证门禁系统市场机会、成长要素、产业趋势分析及2026年至2035年预测Fingerprint Access Control System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025年全球指纹认证门禁系统市值为30.4亿美元,预计2035年将以10.6%的复合年增长率成长至73.5亿美元。

市场扩张的驱动力来自住宅、商业和工业设施日益增长的安全需求,以及从传统门禁方式转变为先进的生物识别解决方案。此外,政府对关键区域安全存取的强制性要求、物联网和智慧建筑技术的进步,以及新兴国家商业基础设施的快速发展,都在推动市场成长。各组织和机构越来越意识到,传统的钥匙、识别卡和基于PIN码的系统容易被复製和滥用,而生物识别则能提供可靠的个人身份验证。这种转变的驱动力源于防止未经授权存取、加强课责以及保护公共和私营部门的关键基础设施、职场资产和敏感业务区域的需求。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 30.4亿美元 |

| 预测金额 | 73.5亿美元 |

| 复合年增长率 | 10.6% |

预计到2025年,硬体市场规模将达到13亿美元。在日益增长的安全需求推动下,指纹扫描器、控制器和读取器的部署正在工业、商业和政府机构中不断扩大。政府为安全基础设施现代化所做的努力,正在加速公共设施和关键资产采用高性能硬体。製造商正致力于研发高精度、高可靠性的指纹认证设备,以满足政府和行业严格的安全标准,从而能够在监管严格的工业环境、交通枢纽和公共基础设施计划中实现长期部署。

预计到2025年,光学指纹感测器市场规模将达到7.76亿美元,在部署方面领先市场。由于其成本效益高、可靠性强且易于集成,这些感测器被广泛应用于商业办公大楼、住宅小区和政府计划中。光学感测器因其耐用性和久经考验的性能,尤其适用于大规模部署。企业正在优化这些设备的性价比和稳定性,以满足公共和私人设施的标准化安全要求。

预计2025年,美国指纹认证门禁系统市场规模将达8.265亿美元。随着联邦政府优先事项的推进,包括边境管制、关键基础设施建设以及政府设施安全基础设施身份验证的现代化和升级,美国指纹认证系统的部署正在不断扩大。指纹认证系统在联邦安全战略中扮演着日益重要的角色,例如移民执法和设施门禁控制。製造商正优先考虑符合美国国防安全保障部的标准,并建立战略伙伴关係关係,以支援在联邦政府和关键基础设施计划中的部署。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 住宅、商业和工业领域的安全问题日益严重。

- 与传统门禁系统相比,生物识别解决方案的采用率正在不断提高。

- 政府关于安全存取机密区域的法规和义务

- 与物联网和智慧建筑技术的集成

- 新兴市场商业基础设施的扩张

- 挑战与困难

- 较高的初始投资和安装成本

- 隐私问题和资料保护条例

- 促进因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 对永续性的承诺

- 供应链韧性

- 地缘政治分析

- 数位转型

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 区域扩张比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 产品系列比较

- 2022-2025 年重大发展

- 併购

- 合作伙伴关係和合资企业

- 技术进步

- 扩张和投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估计与预测:依组件划分,2022-2035年

- 硬体

- 阅读器/扫描仪

- 指纹认证设备

- 门锁和控制器

- 软体

- 演算法引擎

- 存取管理软体

- 考勤管理

- 服务

- 安装

- 一体化

- 维护和支援

第六章 市场估算与预测:依感测器类型划分,2022-2035年

- 光学的

- 电容式

- 超音波

- 热感的

- 频谱

- 其他的

第七章 市场估算与预测:依部署类型划分,2022-2035年

- 本地部署系统

- 云端管理系统

- 混合系统

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 主要趋势

- 门禁管制

- 受限设施访问

- 员工考勤管理

- 访客管理

第九章 市场估计与预测:依最终用途产业划分,2022-2035年

- 商业的

- 住宅

- 工业和製造业

- 政府/国防

- 卫生保健

- 教育

- 饭店和零售业

- 其他的

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第十一章:公司简介

- 主要企业

- HID Global Corporation

- IDEMIA(Morpho)

- Thales Group

- NEC Corporation

- Suprema Inc.

- 按地区分類的主要企业

- 北美洲

- 3M Cogent, Inc.

- Aware, Inc.

- Integrated Biometrics

- Secugen Corporation

- M2SYS Technology

- 欧洲

- Fingerprint Cards AB

- Precise Biometrics AB

- 亚太地区

- Anviz Global Inc.

- Aratek Biometrics

- BioEnable Technologies Pvt. Ltd.

- Mantra Softech(India)Pvt. Ltd.

- 北美洲

- 小众/颠覆者

- Nitgen Co., Ltd.

- ZKTeco Co., Ltd.

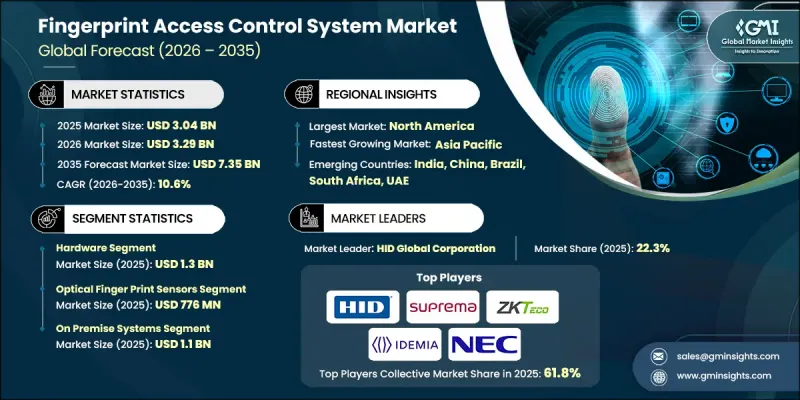

The Global Fingerprint Access Control System Market was valued at USD 3.04 billion in 2025 and is estimated to grow at a CAGR of 10.6% to reach USD 7.35 billion by 2035.

Market expansion is driven by the rising emphasis on security across residential, commercial, and industrial facilities, coupled with the shift from conventional access methods to advanced biometric solutions. Government mandates for secure access in sensitive zones, growing integration of IoT and smart building technologies, and the surge in commercial infrastructure development in emerging economies are further propelling growth. Organizations and authorities are increasingly recognizing that traditional keys, ID badges, or PIN-based systems are prone to duplication and misuse, whereas biometric authentication provides reliable, individualized verification. This transition is fueled by the need to prevent unauthorized entry, enhance accountability, and safeguard critical infrastructure, workplace assets, and sensitive operational areas across both public and private sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.04 Billion |

| Forecast Value | $7.35 Billion |

| CAGR | 10.6% |

The hardware segment reached USD 1.3 billion in 2025. Deployment of fingerprint scanners, controllers, and readers is expanding across industrial, commercial, and government facilities due to growing security requirements. Government initiatives to modernize security infrastructure are accelerating the adoption of robust hardware for public facilities and critical assets. Manufacturers are focusing on high-accuracy, ruggedized fingerprint devices that meet stringent government and industry security standards, enabling long-term adoption in regulated industrial environments, transportation hubs, and public infrastructure projects.

The optical fingerprint sensors segment accounted for USD 776 million in 2025 and led the market in terms of adoption. These sensors are widely preferred for their cost-effectiveness, reliability, and ease of integration across commercial offices, residential complexes, and government projects. Optical sensors are particularly popular in high-volume deployments due to their durability and proven performance. Companies are optimizing these devices for affordability and robustness to meet standardized security requirements in public and private facilities.

U.S. Fingerprint Access Control System Market was valued at USD 826.5 million in 2025. Adoption in the U.S. is expanding in line with broader federal priorities to modernize security infrastructure and enhance identity verification across border control, critical infrastructure, and government facilities. Fingerprint access systems are increasingly central to federal security strategies, including immigration enforcement and facility access management. Manufacturers are prioritizing compliance with U.S. Department of Homeland Security standards and establishing strategic partnerships to support deployments across federal and critical infrastructure projects.

Prominent players in the Global Fingerprint Access Control System Market include 3M Cogent, Inc., Anviz Global Inc., Aratek Biometrics, Aware, Inc., BioEnable Technologies Pvt. Ltd., Fingerprint Cards AB (Fingerprints), HID Global Corporation, IDEMIA (Morpho), Integrated Biometrics, M2SYS Technology, Mantra Softech (India) Pvt. Ltd., NEC Corporation, Nitgen Co., Ltd., Precise Biometrics AB, Secugen Corporation, Suprema Inc., Thales Group, and ZKTeco Co., Ltd. Companies operating in the Global Fingerprint Access Control System Market are employing several key strategies to strengthen their market position. These include investing in research and development to improve sensor accuracy, speed, and durability; expanding product portfolios with integrated IoT and cloud-based solutions; and forming strategic alliances with government agencies and commercial integrators to secure large-scale contracts. Companies are also focusing on geographic expansion into emerging markets, enhancing after-sales support and maintenance services, and developing customized solutions for specific industries. Strategic mergers and acquisitions are being leveraged to enhance technological capabilities, broaden global reach, and secure long-term supply agreements, reinforcing competitive advantage in a rapidly evolving market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Component trends

- 2.2.2 Sensor type trends

- 2.2.3 Deployment type trends

- 2.2.4 Application trends

- 2.2.5 End users trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising security concerns in residential, commercial, and industrial sectors

- 3.2.1.2 Increasing adoption of biometric solutions over traditional access systems

- 3.2.1.3 Government regulations and mandates for secure access in sensitive areas

- 3.2.1.4 Integration with IoT and smart building technologies

- 3.2.1.5 Expansion of commercial infrastructure in emerging markets

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High initial investment and installation costs

- 3.2.2.2 Privacy concerns and data protection regulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Initiatives

- 3.11 Supply Chain Resilience

- 3.12 Geopolitical Analysis

- 3.13 Digital Transformation

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Readers/scanners

- 5.2.2 Fingerprint terminals

- 5.2.3 Door locks & controllers

- 5.3 Software

- 5.3.1 Algorithm engine

- 5.3.2 Access control management software

- 5.3.3 Time & attendance

- 5.4 Services

- 5.4.1 Installation

- 5.4.2 Integration

- 5.4.3 Maintenance/support

Chapter 6 Market Estimates and Forecast, By Sensor Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Optical

- 6.3 Capacitive

- 6.4 Ultrasonic

- 6.5 Thermal

- 6.6 Multispectral

- 6.7 Other

Chapter 7 Market Estimates and Forecast, By Deployment Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 On-premise systems

- 7.3 Cloud-managed systems

- 7.4 Hybrid systems

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key Trends

- 8.2 Door access control

- 8.3 Restricted facility access

- 8.4 Workforce attendance tracking

- 8.5 Visitor management

Chapter 9 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Commercial

- 9.3 Residential

- 9.4 Industrial/manufacturing

- 9.5 Government & defense

- 9.6 Healthcare

- 9.7 Education

- 9.8 Hospitality & retail

- 9.9 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 HID Global Corporation

- 11.1.2 IDEMIA (Morpho)

- 11.1.3 Thales Group

- 11.1.4 NEC Corporation

- 11.1.5 Suprema Inc.

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 3M Cogent, Inc.

- 11.2.1.2 Aware, Inc.

- 11.2.1.3 Integrated Biometrics

- 11.2.1.4 Secugen Corporation

- 11.2.1.5 M2SYS Technology

- 11.2.2 Europe

- 11.2.2.1 Fingerprint Cards AB

- 11.2.2.2 Precise Biometrics AB

- 11.2.3 Asia Pacific

- 11.2.3.1 Anviz Global Inc.

- 11.2.3.2 Aratek Biometrics

- 11.2.3.3 BioEnable Technologies Pvt. Ltd.

- 11.2.3.4 Mantra Softech (India) Pvt. Ltd.

- 11.2.1 North America

- 11.3 Niche / Disruptors

- 11.3.1 Nitgen Co., Ltd.

- 11.3.2 ZKTeco Co., Ltd.