|

市场调查报告书

商品编码

1959601

同步电容器市场机会、成长要素、产业趋势分析及2026年至2035年预测Synchronous Condenser Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

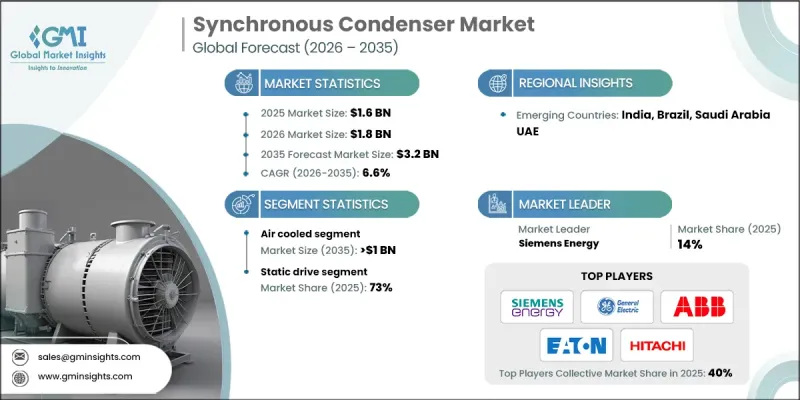

2025年全球同步电容器市场价值为16亿美元,预计2035年将达32亿美元,年复合成长率为6.6%。

这一增长主要源于石化燃料发电厂的退役,这些电厂传统上为电网提供惯性和无功功率,由此造成了巨大的功率缺口,而同步电容器可以有效弥补这一缺口。电网现代化倡议,包括智慧电网建设和高压直流计划,正在加速对这些设备的需求。各国政府和电力公司正大力投资老旧基础设施的升级改造、提高可靠性标准以及整合分散式能源。风能和太阳能的快速部署带来了不稳定的输出,导致电压和频率不稳定。同步电容器能够提供快速可靠的无功功率支持,从而稳定电网并提高电能品质。不断增长的电力需求和对可再生能源计划的大规模投资进一步推动了这些系统的部署,因为现代电网需要复杂的解决方案来高效管理间歇性能源来源。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 16亿美元 |

| 预测金额 | 32亿美元 |

| 复合年增长率 | 6.6% |

预计2035年,空冷式同步冷凝器市场规模将达10亿美元。与水冷式和氢冷式系统相比,空冷式同步冷凝器因其成本效益高、安装简单而更受欢迎。其设计降低了基础设施需求、初始资本支出和运作复杂性,使其特别适用于水资源有限或安全法规严格的地区。技术进步正在进一步提高效率和可靠性,从而推动空冷式系统在全球工业和公共产业领域的应用日益广泛。

预计到2025年,静电驱动市占率将达到73%,并在2026年至2035年间以6%的复合年增长率成长。静电驱动采用闸流体和IGBT等电力电子元件,与传统启动方式相比,效率更高。它们能够精确控制启动电流和转矩,最大限度地减少机械应力,降低设备磨损,并确保大型电网更可靠地运作。

预计2035年,美国同步电容器市场规模将达1.88亿美元。旨在确保电网可靠性和整合可再生能源的严格法规,正在增加对同步电容器等先进无功功率补偿装置的需求。包括石油和天然气行业在内的工业成长,进一步推动了同步电容器的应用。美国在全球贸易中扮演着至关重要的角色,对电力基础设施的投资将对国内和国际能源市场产生影响。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 原物料供应情况

- 影响价值链的因素

- 中断

- 监管环境

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 成长潜力分析

- 波特五力分析

- PESTEL 分析

- 新机会与趋势

- 投资分析及未来展望

第四章 竞争情势

- 介绍

- 我们按地区分類的市场份额

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 策略倡议

- 竞争标竿分析图

- 战略仪錶板

- 创新与科技趋势

第五章 市场规模及预测:依冷却方式划分,2022-2035年

- 氢冷

- 空冷式

- 水冷

第六章 市场规模与预测:依创业模式划分,2022-2035年

- 静态驱动系统

- 辅助马达

- 其他的

第七章 市场规模与预测:依最终用户划分,2022-2035年

- 公共产业

- 工业的

第八章 市场规模及预测:依无功功率等级划分,2022-2035年

- ≤100 MVAr

- 超过 100 MVAr 至低于 200 MVAr

- 超过200兆瓦

第九章 市场规模及预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 义大利

- 法国

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第十章:公司简介

- ABB

- Alstom SA

- ANDRITZ

- Ansaldo Energia

- Baker Hughes

- Bharat Heavy Electricals Limited

- BRUSH

- Doosan

- Eaton

- General Electric

- Hitachi Energy Ltd.

- Ingeteam

- Mitsubishi Electric Power Products, Inc.

- NIDEC Corporation

- Power Systems &Controls, Inc.

- Shanghai Electric

- Siemens Energy

- Toshiba Energy Systems &Solutions Corporation

- Voith GmbH &Co.

- WEG

The Global Synchronous Condenser Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 3.2 billion by 2035.

The growth is driven by the retirement of fossil-fuel-based power plants, which traditionally supplied grid inertia and reactive power, leaving a critical gap that synchronous condensers effectively address. Grid modernization initiatives, including smart grid development and high-voltage direct current (HVDC) transmission projects, are accelerating the demand for these devices. Governments and utilities are investing heavily to upgrade aging infrastructure, meet stricter reliability standards, and integrate distributed energy resources. The rapid deployment of wind and solar power introduces variable outputs that can destabilize voltage and frequency. Synchronous condensers provide fast and reliable reactive power support, stabilizing the grid and enhancing power quality. Rising electricity demand, coupled with large-scale investments in renewable energy projects, is further driving the adoption of these systems, as modern grids require advanced solutions to manage intermittent energy sources efficiently.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 6.6% |

The air-cooled segment is expected to reach USD 1 billion by 2035. Air-cooled synchronous condensers are favored for their cost-effectiveness and simpler installation process compared to water- or hydrogen-cooled systems. Their design reduces infrastructure requirements, lowering upfront capital expenditure and operational complexity. This makes them particularly suitable for regions with limited water resources or strict safety regulations. Technological advancements have further improved efficiency and reliability, increasing the adoption of air-cooled systems across industrial and utility applications worldwide.

The static drive segment accounted for 73% share in 2025 and is projected to grow at a CAGR of 6% from 2026 to 2035. Static drives, which leverage power electronic components like thyristors and IGBTs, provide superior efficiency over traditional starting methods. They allow precise control of starting current and torque, minimizing mechanical stress, reducing equipment wear, and ensuring more reliable operation in large-scale electrical networks.

U.S. Synchronous Condenser Market is expected to reach USD 188 million by 2035. Stringent regulations focused on grid reliability and the integration of renewable energy necessitate advanced reactive power compensation devices like synchronous condensers. Industrial growth, including demand from sectors such as oil and gas, further drives adoption. The U.S. also plays a significant role in global trade, where electricity infrastructure investments impact both domestic and international energy markets.

Leading players in the Global Synchronous Condenser Market include ABB, Hitachi Energy Ltd., Toshiba Energy Systems & Solutions Corporation, Mitsubishi Electric Power Products, Inc., Alstom SA, Eaton, Siemens Energy, Doosan, NIDEC Corporation, Bharat Heavy Electricals Limited, Ansaldo Energia, Power Systems & Controls, Inc., BRUSH, Voith GmbH & Co., ANDRITZ, Shanghai Electric, Baker Hughes, and Ingeteam. Companies in the synchronous condenser market are adopting multiple strategies to strengthen their market position. Investment in research and development focuses on enhancing efficiency, reliability, and integration with renewable energy grids. Strategic partnerships with utilities and independent power producers help expand deployment and service networks globally. Firms are developing modular, scalable solutions tailored to industrial, renewable, and grid stabilization applications. Focusing on digital monitoring, predictive maintenance, and remote control capabilities improves operational performance and customer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability landscape

- 3.1.2 Factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Emerging opportunities & trends

- 3.8 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Cooling, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hydrogen Cooled

- 5.3 Air Cooled

- 5.4 Water Cooled

Chapter 6 Market Size and Forecast, By Starting Method, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Static Drive

- 6.3 Pony motors

- 6.4 Others

Chapter 7 Market Size and Forecast, By End User, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Utility

- 7.3 Industrial

Chapter 8 Market Size and Forecast, By Reactive Power Rating, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 ≤ 100 MVAr

- 8.3 > 100 MVAr to ≤ 200 MVAr

- 8.4 > 200 MVAr

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 Italy

- 9.3.3 France

- 9.3.4 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Alstom SA

- 10.3 ANDRITZ

- 10.4 Ansaldo Energia

- 10.5 Baker Hughes

- 10.6 Bharat Heavy Electricals Limited

- 10.7 BRUSH

- 10.8 Doosan

- 10.9 Eaton

- 10.10 General Electric

- 10.11 Hitachi Energy Ltd.

- 10.12 Ingeteam

- 10.13 Mitsubishi Electric Power Products, Inc.

- 10.14 NIDEC Corporation

- 10.15 Power Systems & Controls, Inc.

- 10.16 Shanghai Electric

- 10.17 Siemens Energy

- 10.18 Toshiba Energy Systems & Solutions Corporation

- 10.19 Voith GmbH & Co.

- 10.20 WEG

2026年全球同步电容器市场报告

2026年全球同步电容器市场报告 全球同步调相机市场(依冷却类型、类型、启动方式、最终用户、额定无功功率和地区划分)-预测(至2030年)

全球同步调相机市场(依冷却类型、类型、启动方式、最终用户、额定无功功率和地区划分)-预测(至2030年) 全球同步冷凝器市场规模、份额、趋势及成长分析报告(2026-2034)

全球同步冷凝器市场规模、份额、趋势及成长分析报告(2026-2034) 同步冷凝器市场-全球产业规模、份额、趋势、机会与预测:按类型、冷却方式、启动方式、最终用户、无功功率容量、地区和竞争格局划分,2021-2031年

同步冷凝器市场-全球产业规模、份额、趋势、机会与预测:按类型、冷却方式、启动方式、最终用户、无功功率容量、地区和竞争格局划分,2021-2031年 并联同步冷凝器市场依励磁方式、安装方式、冷却方式及最终用途划分-全球预测,2026-2032年同步冷凝器市场-2026-2031年预测

并联同步冷凝器市场依励磁方式、安装方式、冷却方式及最终用途划分-全球预测,2026-2032年同步冷凝器市场-2026-2031年预测 同步冷凝器市场规模、份额和成长分析:按冷却技术、启动方式、无功功率额定值、最终用户、类型和地区划分 - 2026-2033 年行业预测

同步冷凝器市场规模、份额和成长分析:按冷却技术、启动方式、无功功率额定值、最终用户、类型和地区划分 - 2026-2033 年行业预测 同步调相机市场,按产品类型、冷却方式、按无功功率额定值、按启动方式、按最终用户、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测

同步调相机市场,按产品类型、冷却方式、按无功功率额定值、按启动方式、按最终用户、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测 同步电容器市场规模、份额、趋势分析报告:按产品类型、最终用途、地区和细分市场预测,2025 年至 2030 年

同步电容器市场规模、份额、趋势分析报告:按产品类型、最终用途、地区和细分市场预测,2025 年至 2030 年 公用事业规模风冷同步冷凝器市场、机会、成长动力、产业趋势分析与预测,2024-2032

公用事业规模风冷同步冷凝器市场、机会、成长动力、产业趋势分析与预测,2024-2032