|

市场调查报告书

商品编码

1959619

血液采集市场成长机会、成长要素、产业趋势分析及2026年至2035年预测。Blood Collection Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

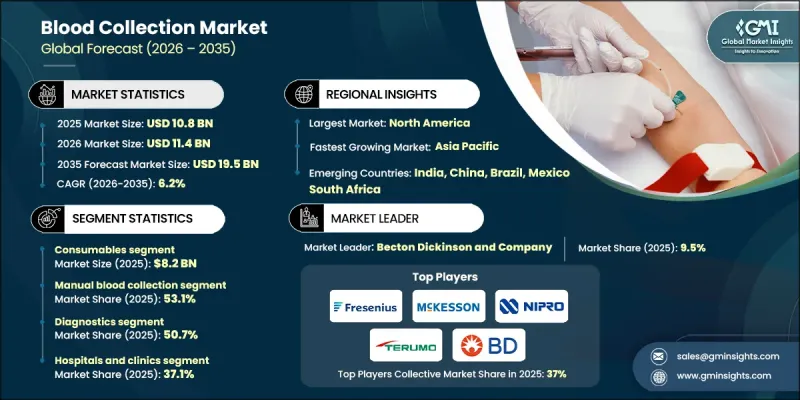

2025 年全球血液采集市场价值 108 亿美元,预计到 2035 年将达到 195 亿美元,年复合成长率为 6.2%。

全球疾病负担日益加重、血液采集技术不断进步以及全球医疗程序数量不断增加,共同推动了血液采集市场的成长。随着医疗系统越来越重视早期检测、定期监测和精准医疗,对准确高效血液采集的需求持续上升。血液采集是诊断流程中的关键步骤,可支援疾病检测、疗效评估以及在多种医疗环境中对病患监测。临床介入措施的增加进一步刺激了这项需求,需要在患者评估和復原过程中进行血液检测。采集方法的进步、以安全为中心的设计以及简化的工作流程也促进了血液采集技术的广泛应用。这些因素共同推动了市场成长,同时也凸显了可靠的血液采集解决方案在医院、检查室和照护现场场所的重要性。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 108亿美元 |

| 预测金额 | 195亿美元 |

| 复合年增长率 | 6.2% |

预计到2025年,耗材市场规模将达82亿美元。此细分市场包括用于血液样本采集、处理和运输的必需一次性产品。由于其一次性使用的特性,每次抽血后都需要这些产品,因此在整个医疗机构中都不可或缺。耗材在维持样本完整性、防止污染和确保诊断结果准确性方面发挥着至关重要的作用。其广泛且重复的使用持续推动临床和检查室对耗材的稳定需求。

预计到2025年,诊断业务将占市场份额的50.7%。该业务涵盖用于采集和分析血液样本以进行疾病识别、监测和管理的设备和耗材。随着常规体检和慢性病管理需求的不断增长,以及对高效先进的血液采集系统的日益依赖,该业务板块正持续增长。

预计到2025年,北美血液采集市占率将达到35.4%。该地区的成长主要得益于高诊断检测量、完善的医疗基础设施以及人口快速老化。老年人医疗保健需求的增加推高了对血液诊断工具的需求,进一步扩大了全部区域的市场规模。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 慢性疾病和感染疾病的发生率增加

- 血液采样技术的进步

- 手术数量增加

- 人口老化加剧

- 产业潜在风险与挑战

- 输血相关风险

- 熟练医疗专业人员短缺

- 市场机会

- 政府主导的促进捐血和疾病筛检的宣传活动增加。

- 促进因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 科技趋势

- 当前技术趋势

- 新兴技术

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略仪錶板

- 主要进展

- 併购

- 合作伙伴关係和合资企业

- 新产品发布

- 扩张计划

第五章 市场估算与预测:依产品类型划分,2021-2034年

- 系统

- 自动化系统

- 手动系统

- 消耗品

- 静脉注射用

- 针头和注射器

- 双头针

- 带翅膀的采血套装

- 标准皮下注射针

- 其他采血针

- 采血管

- 用于血清分离

- EDTA

- 肝素

- 用于等离子体分离

- 血袋

- 其他静脉产品

- 针头和注射器

- 毛细管

- 《采血针》

- 微型容器管

- 微量血球容积比管

- 保温装置

- 其他毛细血管产品

- 静脉注射用

第六章 市场估计与预测:依方法划分,2021-2034年

- 人工采血

- 自动化采血

第七章 市场估计与预测:依应用领域划分,2021-2034年

- 诊断

- 治疗

- 研究

第八章 市场估算与预测:依最终用途划分,2021-2034年

- 医院和诊所

- 诊断中心

- 血库

- 学术研究机构

第九章 市场估计与预测:依地区划分,2021-2034年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- Abbott Laboratories

- Becton, Dickinson, and Company

- Cardinal Health

- F. Hoffmann-La Roche

- FL MEDICAL

- Fresenius SE &Co

- Greiner

- Haemonetics Corporation

- McKesson Corporation

- Nipro Corporation

- QIAGEN

- Sarstedt AG &Co

- Siemens Healthineers

- Streck

- Terumo Corporation

- Thermo Fisher Scientific

The Global Blood Collection Market was valued at USD 10.8 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 19.5 billion by 2035.

Growth is supported by the rising global disease burden, continuous progress in blood collection technologies, and the increasing volume of medical procedures performed worldwide. As healthcare systems place greater emphasis on early detection, routine monitoring, and precision-based treatment, the demand for accurate and efficient blood sampling continues to rise. Blood collection remains a foundational step in diagnostic workflows, supporting disease detection, therapy evaluation, and long-term patient monitoring across multiple care settings. The growing number of clinical interventions further reinforces demand, as blood-based assessments are required throughout patient evaluation and recovery processes. Advancements in collection methods, safety-focused designs, and workflow efficiency are also contributing to broader adoption. Together, these factors are strengthening market growth while reinforcing the importance of reliable blood collection solutions across hospitals, laboratories, and point-of-care environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.8 Billion |

| Forecast Value | $19.5 Billion |

| CAGR | 6.2% |

The consumables category generated USD 8.2 billion in 2025. This segment includes single-use products essential for collecting, handling, and transporting blood samples. Due to their disposable nature, these items are required for every blood draw, making them indispensable across healthcare facilities. Consumables play a critical role in maintaining sample integrity, preventing contamination, and ensuring accurate diagnostic outcomes. Their widespread and repetitive use continues to drive consistent demand across clinical and laboratory settings.

The diagnostics segment held 50.7% share in 2025. This segment encompasses devices and consumables used to collect and analyze blood samples for disease identification, monitoring, and management. Rising demand for routine testing and long-term condition management has increased reliance on efficient and advanced blood collection systems, supporting sustained growth in this segment.

North America Blood Collection Market accounted for 35.4% share in 2025. Regional growth is driven by high diagnostic testing volumes, well-established healthcare infrastructure, and a rapidly aging population. Increasing healthcare utilization among older individuals has led to higher demand for blood-based diagnostic tools, reinforcing market expansion across the region.

Key companies operating in the Global Blood Collection Market include Thermo Fisher Scientific, Becton, Dickinson, and Company, Abbott Laboratories, Siemens Healthineers, Cardinal Health, McKesson Corporation, Terumo Corporation, Greiner, Sarstedt AG & Co, Nipro Corporation, QIAGEN, Streck, Haemonetics Corporation, F. Hoffmann-La Roche, Fresenius SE & Co, and FL MEDICAL. Companies in the blood collection market are strengthening their market position through product innovation, safety enhancements, and expanded distribution networks. Manufacturers are investing in user-friendly, safety-engineered designs to reduce contamination risks and improve clinical efficiency. Emphasis on automation and compatibility with advanced diagnostic platforms helps streamline laboratory workflows. Strategic partnerships with healthcare providers and distributors support broader market reach. Firms are also expanding manufacturing capacity to meet rising global demand while ensuring regulatory compliance. Continuous focus on quality assurance, cost optimization, and sustainability initiatives further enhances competitiveness, allowing companies to maintain strong relationships with healthcare systems and reinforce long-term market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Method trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.2.5 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chronic and infectious diseases

- 3.2.1.2 Advancements in blood collection technologies

- 3.2.1.3 Increasing number of surgical procedures

- 3.2.1.4 Rising geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risks associated with blood transfusions

- 3.2.2.2 Lack of skilled healthcare professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Rising government-led campaigns for promoting blood donation and disease screening

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 System

- 5.2.1 Automated systems

- 5.2.2 Manual systems

- 5.3 Consumables

- 5.3.1 Venous

- 5.3.1.1 Needles and syringes

- 5.3.1.1.1 Double-ended needles

- 5.3.1.1.2 Winged blood collection sets

- 5.3.1.1.3 Standard hypodermic needles

- 5.3.1.1.4 Other blood collection needles

- 5.3.1.2 Blood collection tubes

- 5.3.1.2.1 Serum-separating

- 5.3.1.2.2 EDTA

- 5.3.1.2.3 Heparin

- 5.3.1.2.4 Plasma-separating

- 5.3.1.3 Blood bags

- 5.3.1.4 Other venous products

- 5.3.1.1 Needles and syringes

- 5.3.2 Capillary

- 5.3.2.1 Lancets

- 5.3.2.2 Micro-container tubes

- 5.3.2.3 Micro-hematocrit tubes

- 5.3.2.4 Warming devices

- 5.3.2.5 Other capillary products

- 5.3.1 Venous

Chapter 6 Market Estimates and Forecast, By Method, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Manual blood collection

- 6.3 Automated blood collection

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Diagnostics

- 7.3 Treatment

- 7.4 Research

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and clinics

- 8.3 Diagnostic centers

- 8.4 Blood banks

- 8.5 Academic and research institutes

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 Becton, Dickinson, and Company

- 10.3 Cardinal Health

- 10.4 F. Hoffmann-La Roche

- 10.5 FL MEDICAL

- 10.6 Fresenius SE & Co

- 10.7 Greiner

- 10.8 Haemonetics Corporation

- 10.9 McKesson Corporation

- 10.10 Nipro Corporation

- 10.11 QIAGEN

- 10.12 Sarstedt AG & Co

- 10.13 Siemens Healthineers

- 10.14 Streck

- 10.15 Terumo Corporation

- 10.16 Thermo Fisher Scientific

血液采集管塞市场按材料、最终用户、管型和密封机制划分-全球预测,2026-2032年

血液采集管塞市场按材料、最终用户、管型和密封机制划分-全球预测,2026-2032年 2026年全球毛细血管采血设备市场报告2026年全球自体血液采集与储存设备市场报告2026年全球自动化血液采集市场报告2026年全球血液采集、处理与管理设备市场报告2026年全球血液采集设备市场报告

2026年全球毛细血管采血设备市场报告2026年全球自体血液采集与储存设备市场报告2026年全球自动化血液采集市场报告2026年全球血液采集、处理与管理设备市场报告2026年全球血液采集设备市场报告 全球干血斑采集卡市场规模、份额、趋势及成长分析报告(2026-2034年)

全球干血斑采集卡市场规模、份额、趋势及成长分析报告(2026-2034年) 毛细血管采血装置市场 - 全球产业规模、份额、趋势、机会及预测(按产品、材料、最终用途、应用、地区和竞争格局划分),2021-2031年真空采血市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、最终用途、地区和竞争格局划分,2021-2031年)一次性无菌采血管市场按类型、材质、应用和最终用户划分-2026-2032年全球预测

毛细血管采血装置市场 - 全球产业规模、份额、趋势、机会及预测(按产品、材料、最终用途、应用、地区和竞争格局划分),2021-2031年真空采血市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、最终用途、地区和竞争格局划分,2021-2031年)一次性无菌采血管市场按类型、材质、应用和最终用户划分-2026-2032年全球预测