|

市场调查报告书

商品编码

1959621

水产养殖疫苗市场机会、成长要素、产业趋势分析及2026年至2035年预测。Aquaculture Vaccines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

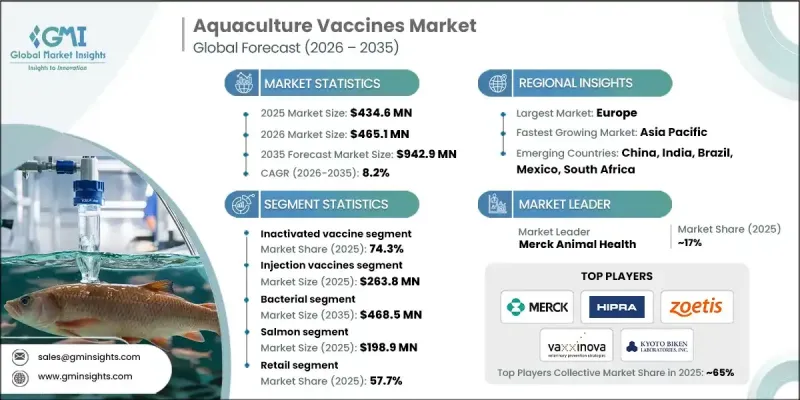

2025 年全球水产养殖疫苗市场价值为 4.346 亿美元,预计到 2035 年将达到 9.429 亿美元,年复合成长率为 8.2%。

全球水产养殖生产的扩张和鱼类需求的成长推动了市场成长。细菌和病毒感染疾病弧菌、气单胞菌和其他病原体引起的感染)的日益频繁,使得降低死亡率和提高生产力的感染疾病需求不断增长。水产养殖疫苗是一种能够刺激鱼类和甲壳类动物等水生动物免疫系统的生物製药,使其对特定病原体产生抵抗力。这些疫苗可透过注射、浸泡或口服给药,有助于最大限度地减少疾病爆发、减少抗生素的使用并促进永续水产养殖。新兴市场,特别是亚太地区和拉丁美洲的市场,以及对口服和浸泡疫苗给药技术研发投入的增加,都在推动市场成长。製造商和水产养殖公司之间的合作,正在促进创新解决方案的快速商业化和广泛推广。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 4.346亿美元 |

| 预测金额 | 9.429亿美元 |

| 复合年增长率 | 8.2% |

灭活疫苗市场占有率占74.3%,预计到2035年将以8.1%的复合年增长率成长。其安全性高、保护范围广、稳定性佳,深受养殖者青睐。这类疫苗广泛应用于各种水产养殖物种,能够提供稳定的免疫反应,且无復发风险。多种给药方式,例如注射和浸泡,为养殖户提供了操作柔软性。监管标准推荐使用非活病毒疫苗製剂、消费者对无抗生素水产品的需求不断增长,以及集约化水产养殖系统对生物安全的日益重视,都进一步推动了灭活疫苗的普及应用。

预计到2025年,注射疫苗市场规模将达到2.638亿美元,并将以8.1%的复合年增长率持续成长至2035年。注射疫苗透过直接向鱼类注射精确剂量,提供卓越的疗效和持久的免疫力,确保对细菌和病毒病原体的最佳保护。自动化疫苗接种系统和符合人体工学设计的设备的创新,简化了接种流程,减轻了动物的压力反应,并提高了孵化场和养殖场的运作效率。

预计到2025年,欧洲水产养殖疫苗市场份额将达到43%,这主要得益于先进的水产养殖产业、对疾病预防法规的高度重视以及疫苗接种计划的早期实施。对预防性抗生素使用的监管限制正在加速向疫苗的转变,而完善的低温运输分销网络、专业的兽医支持以及领先疫苗生产商的存在,都为市场的可持续增长做出了贡献。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 细菌和性行为感染正在增加。

- 全球水产养殖产量增加

- 研发并推出一种用于水产养殖的新疫苗

- 扩大水产养殖疫苗的使用,以取代抗生素

- 产业潜在风险与挑战

- 小规模水产养殖户意识薄弱

- 复杂的疫苗研发流程

- 市场机会

- 口服疫苗和浸泡疫苗的出现

- 新兴市场对水产养殖的投资正在增加。

- 促进因素

- 成长潜力分析

- 科技趋势

- 当前技术趋势

- 新兴技术

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 管道分析

- 未来市场趋势

- 波特的分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 市场估计与预测:依疫苗类型划分,2022-2035年

- 灭活疫苗

- 减毒活病毒疫苗

- 次单位疫苗

- 其他疫苗类型

第六章 市场估计与预测:依给药途径划分,2022-2035年

- 注射疫苗

- 口服疫苗

- 浸没和喷淋

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 细菌

- 病毒性的

- 寄生虫

- 合成的

第八章 市场估算与预测:依类型划分,2022-2035年

- 鲑鱼

- 鳟鱼

- 吴郭鱼

- 铃木

- 海鲷

- 比目鱼

- 鲤鱼

- 其他鱼类

第九章 市场估价与预测:依通路划分,2022-2035年

- 零售

- 电子商务

- 兽医医院/兽医诊所附设药房

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 挪威

- 爱尔兰

- 土耳其

- 丹麦

- 亚太地区

- 中国

- 印度

- 印尼

- 菲律宾

- 越南

- 澳洲

- 纽西兰

- 拉丁美洲

- 巴西

- 墨西哥

- 智利

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章:公司简介

- Cavac

- CIBA

- HIPRA

- Kemin Industries

- Kyoritsu Seiyaku

- Kyoto Biken Laboratories

- Merck Animal Health

- Nisseiken

- Phibro Animal Health

- Tecnovax

- Vaxxinova International

- Veterquimica

- Virbac

- Zoetis

The Global Aquaculture Vaccines Market was valued at USD 434.6 million in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 942.9 million by 2035.

Market growth is driven by the expansion of global aquaculture production and the rising demand for fish. Frequent bacterial and viral outbreaks, including infections caused by Vibrio, Aeromonas, and other pathogens, have increased the need for vaccines that reduce mortality and improve productivity. Aquaculture vaccines are biological preparations that stimulate the immune system of aquatic animals, such as fish and crustaceans, providing resistance to specific pathogens. Administered via injection, immersion, or oral routes, these vaccines help minimize disease outbreaks, reduce antibiotic use, and promote sustainable fish farming. Emerging markets, particularly in Asia-Pacific and Latin America, are contributing to growth, alongside rising investments in R&D for oral and immersion vaccine delivery. Collaborations between manufacturers and aquaculture companies are enabling faster commercialization and broader access to innovative solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $434.6 Million |

| Forecast Value | $942.9 Million |

| CAGR | 8.2% |

The inactivated vaccines segment held a 74.3% share and is expected to grow at a CAGR of 8.1% through 2035. Their safety profile, broad-spectrum protection, and stability make them highly preferred among producers. These vaccines are widely used across various aquaculture species and provide consistent immune responses without the risk of reverting to virulence. They are available in multiple delivery formats, including injectable and immersion, offering operational flexibility. Regulatory standards favoring non-live formulations, increasing consumer demand for antibiotic-free seafood, and a focus on biosecurity in intensive farming systems further support their adoption.

The injection vaccines segment accounted for USD 263.8 million in 2025 and is projected to grow at a CAGR of 8.1% through 2035. Injectable vaccines offer superior efficacy and long-lasting immunity by delivering precise doses directly to fish, ensuring optimal protection against bacterial and viral pathogens. Innovations in automated vaccination systems and ergonomic devices have simplified administration, reduced stress on animals, and increased operational efficiency across hatcheries and grow-out farms.

Europe Aquaculture Vaccines Market held a 43% share in 2025, driven by its advanced aquaculture industry, strong regulatory emphasis on disease prevention, and early adoption of vaccination programs. Regulatory restrictions on prophylactic antibiotic use have accelerated the shift toward vaccines, while a well-established cold-chain distribution network, skilled veterinary support, and the presence of leading vaccine manufacturers contribute to sustained growth.

Key players in the Global Aquaculture Vaccines Market include Cavac, CIBA, HIPRA, Kemin Industries, Kyoritsu Seiyaku, Kyoto Biken Laboratories, Merck Animal Health, Nisseiken, Phibro Animal Health, Tecnovax, Vaxxinova International, Veterquimica, Virbac, Zoetis. Companies in the Global Aquaculture Vaccines Market are strengthening their positions by investing in research and development of oral and immersion-based delivery systems, expanding manufacturing capacity, and forming strategic alliances with aquaculture operators for faster commercialization. They are also focusing on emerging markets, enhancing cold-chain logistics, offering value-added services such as technical support and training, and ensuring regulatory compliance to build trust and maintain market leadership.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Vaccine type trends

- 2.2.3 Route of administration trends

- 2.2.4 Application trends

- 2.2.5 Species trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surging prevalence of bacterial and viral infections

- 3.2.1.2 Increasing aquaculture production across the globe

- 3.2.1.3 Development and launch of new aquaculture vaccines

- 3.2.1.4 Rising adoption of aquaculture vaccines over antibiotics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited awareness among small-scale farmers

- 3.2.2.2 Complex vaccine development procedures

- 3.2.3 Market opportunities

- 3.2.3.1 Emergence of oral and immersion-based vaccines

- 3.2.3.2 Expansion into emerging markets with rising aquaculture investments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Vaccine Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Inactivated vaccine

- 5.3 Live attenuated vaccine

- 5.4 Subunit vaccine

- 5.5 Other vaccine types

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Injection vaccines

- 6.3 Oral vaccines

- 6.4 Immersion and spray

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Bacterial

- 7.3 Viral

- 7.4 Parasitic

- 7.5 Combined

Chapter 8 Market Estimates and Forecast, By Species, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Salmon

- 8.3 Trout

- 8.4 Tilapia

- 8.5 Seabass

- 8.6 Seabream

- 8.7 Turbot

- 8.8 Carp

- 8.9 Other species

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Retail

- 9.3 E-commerce

- 9.4 Veterinary hospital/clinic pharmacy

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Norway

- 10.3.7 Ireland

- 10.3.8 Turkey

- 10.3.9 Denmark

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Indonesia

- 10.4.4 Philippines

- 10.4.5 Vietnam

- 10.4.6 Australia

- 10.4.7 New Zealand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Chile

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Cavac

- 11.2 CIBA

- 11.3 HIPRA

- 11.4 Kemin Industries

- 11.5 Kyoritsu Seiyaku

- 11.6 Kyoto Biken Laboratories

- 11.7 Merck Animal Health

- 11.8 Nisseiken

- 11.9 Phibro Animal Health

- 11.10 Tecnovax

- 11.11 Vaxxinova International

- 11.12 Veterquimica

- 11.13 Virbac

- 11.14 Zoetis